Expected shortfall

VAR replacement may be too volatile, banks warn

Criticism of expected shortfall has been muted, but concerns are growing

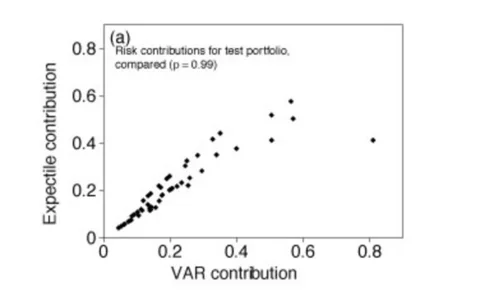

Expectiles behave as expected

Expectiles' results are analogous to those of value-at-risk and expected shortfall

Replacing VAR: smaller banks fear expected shortfall workload

Some banks worry they may not have enough data to implement expected shortfall safely

Baskets will suffer in trading book regime, warns HSBC exec

Capital charges will be ‘very difficult to explain’, conference hears

Models could lose appeal under new trading book rules

Rise of standardised approach would be 'a loss for the banking industry'

Basel Committee drops fixed correlations in new trading book proposals

Banks relieved as revised trading book proposals drop plans for capital to be based on regulator-set correlations

Applied risk management series: Integrating stress tests with risk management

Stress testing is a vital part of successful risk management, but risk managers at energy trading firms frequently face obstacles in designing and implementing successful stress testing programmes. In this article, Carlos Blanco provides some advice on…

Mooted VAR substitute cannot be back-tested, says top quant

Basel Committee should stick with VAR, argues Paul Embrechts of ETH Zürich

The false promise of expected shortfall

The false promise of expected shortfall

ETF tracking error conundrum

Tracking error conundrum

Risk.net poll: Industry divided over plan to scrap VAR

Poll on Basel Committee proposal to ditch VAR attracts close to 1,000 votes - with a narrow victory for critics of the metric

JP Morgan’s ‘London whale’ losses spark VAR debate

In-house probe will look at role of internal model change, among other factors

Basel Committee proposes scrapping VAR

Review recommends switch to expected shortfall, postpones CVA charge overhaul, and retains split between banking and trading books

Quants weigh up VAR's flawed alternatives

VAR at risk

Beyond Basel 2.5: regulators prepare trading book review

Beyond Basel 2.5

Goodbye VAR? Basel to consider other risk metrics

Trading book review will look at replacing value-at-risk, but quants say the obvious alternative - expected shortfall - is not much better

Delayed Basel trading book review will be broad, say supervisors

Basel Committee is expected to consider wide range of topics, including VAR, liquidity, CVA and the line between banking and trading books - but overall capital requirements are not likely to change

An analytical framework for credit portfolio risk measures

An analytical framework for credit portfolio risk measures