Risk magazine - Volume18/No1

Articles in this issue

The importance of ALM

Accounting standards

The top stories from RiskNews

Feature

Fitch buys Algorithmics

New angles

Structured products linked to hedge fund returns

Class notes

Job moves

People

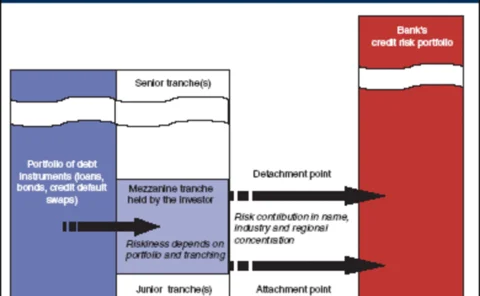

A bank as a manufacturer

The risk architect

Counterparty risk – the next generation

Risk analysis

HSH takes a long-term view

Company profile

A wrong-way bet

Trading losses

German banks get to grips with a new lending reality

Loan pricing systems

Forex appeal

Foreign exchange

Credit risk

Introduction

Reducing long-term forex transaction risk under volume uncertainty

Coporate hedging

From Basel II to Basel III

Portfolio risk

Estimating default correlations using a reduced-form model

Credit risk : Cuttingedge

Market models for CDS

In August 2004, Risk published an article on the pricing of credit default swap (CDS) options entitled A measure of survival by Phillip Schönbucher. Here, Damiano Brigo provides an alternative derivation of the CDS option pricing formula based on Cox