Risk magazine - Volume16/No1

Articles in this issue

The legacy of Dupire

Comments

Real problems

The Risk Awards 2003

The forex toolbox

Review - Books

Pension funds diversify

New angles

Natexis loses in equity derivatives

New angles

The role of correlation

Risk analysis

Software survey 2003

Survey

RiskNews review

The leading stories from RiskNews

An operational risk scorecard approach

Operational risk

Defining forex option value

Options pricing

Technology briefs

Systems

what's new on the web

@risk

What lies beneath?

Credit derivatives

Job moves

People

Quant of the year – Peter Carr

The Risk Awards 2003

Equity derivatives research house of the year – Deutsche Bank

The Risk Awards 2003

Risk manager of the year – Mark Ritter, UBS Warburg

The Risk Awards 2003

Derivatives exchange of the year – Eurex

The Risk Awards 2003

Not all bad news

Comment

Buy-side risk manager of the year - Barclays Global Investors

The Risk Awards 2003

Pounding the pavement

Profile

Lifetime achievement award – Robert Merton

The Risk Awards 2003

Equity derivatives house of the year – UBS Warburg

The Risk Awards 2003

Technology development of the year – CLS Bank

The Risk Awards 2003

Currency derivatives house of the year - ABN Amro

The Risk Awards 2003

Corporate risk manager of the year – Scottish Power

The Risk Awards 2003

Software product of the year – Almonde 4

The Risk Awards 2003

The Risk Awards 2003

The Risk Awards 2003

Mixed signals

Introduction

Testing rating accuracy

Cutting edge: Ratings validation

Canada’s shifting credit scene

Canadian banks

New dawn for loan portfolio management

Credit risk survey

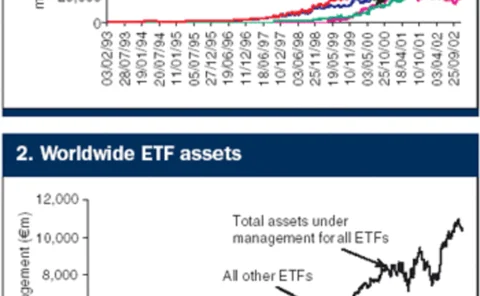

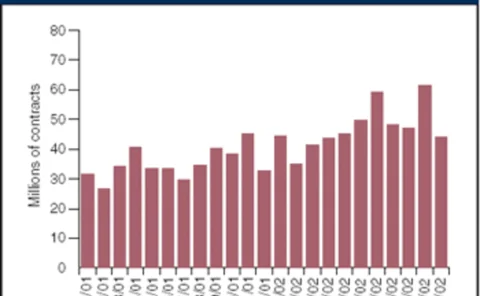

Exchanges in vogue?

Introduction

Pitching to the public

Retail investors

Winds of change blow for the CME

Chicago Mercantile Exchange

Box enters the ring

Boston Options Exchange

At a crossroads

Sydney Futures Exchange

Dealing with discrete dividends

Over the past year, we have published several papers on the issue of options on stocks with discrete dividends. At least three distinct models are used by practitioners, involving trade-offs between accuracy and tractability. Here, Remco Bos, Alexander…

Coarse-grained CDOs

While analytical models of credit portfolio risk using conditional independence have been one of the most promising areas of recent research, they often involve granularity assumptions that are violated in CDO reference portfolios. Here, Michael Pykhtin…

Why be backward?

Originally developed as a tool for calibrating smile models, so-called forward methods can also be used to price options and derive Greeks. Here, Peter Carr and Ali Hirsa apply the technique to the pricing of continuously exercisable American-style put…