Swaps data: CCPs – a systemically important market infrastructure

Disclosures show heavy concentration of initial margin in the top three clearing services, writes Amir Khwaja

With more than $1 trillion of financial resources backing cleared trades, and billions of dollars of cash flowing daily between members and clients, clearing houses today are systemically important market infrastructures.

The latest set of quantitative disclosures show $740 billion held as initial margin (IM) – the largest weapon used by central counterparties to protect against risk. Almost half of this is held as cash. Default resources account for another $210 billion.

We aggregate data for more than 50 clearing houses or services, ranging from global firms such as CME, Eurex, Ice and LCH to small regional firms such as AthexClear, KDPW and Keler. A clearing house can operate one or more clearing services and while the distinction is clear, to coin a pun, some disclosures are provided for a clearing house, while others are for a clearing service. So the 50 figure is an understatement if we refer to clearing services and an overstatement if we discuss clearing houses.

Futures and options together account for the largest IM amount by product type, but LCH SwapClear emerges as the largest single clearing service with $159 billion of IM. Clearing can be a lumpy business – the top three services together account for 43% of IM.

Crucially, estimated stress losses as a peak day amount for the default of two participants stood at $56 billion at the mid-point of the year – significantly lower than the $98 billion of prefunded default resources. Capital provided by clearing house owners, so-called ‘skin in the game’, totalled $16 billion – 7.6% of all default resources.

Initial margin

Let’s start with the largest financial resource, initial margin. We aggregate it for all the clearing services we have and separate into house, meaning member firms, and client, meaning firms that do not mutualise losses by contributing to the default fund (DF).

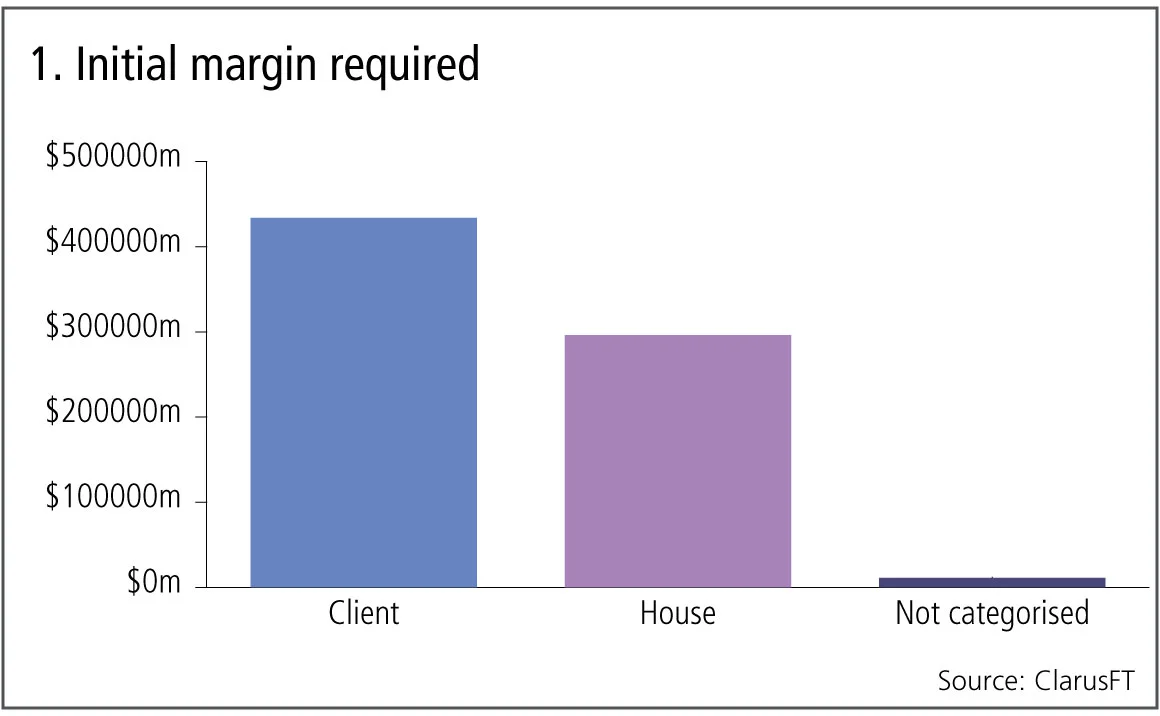

Figure 1 shows:

- Aggregate IM required from client firms is $434 billion, while that required from house (member firms) is $296 billion.

- A split of 59% to 40% with 1% not categorised.

- A grand total of $740 billion as of June 28, 2019.

Next, let’s try to segment this IM by product type. We use product type in a loose sense, so we assign each clearing service to one product type. Often that is obvious from the name of the clearing service but other times we have to plumb for one as there is no split available.

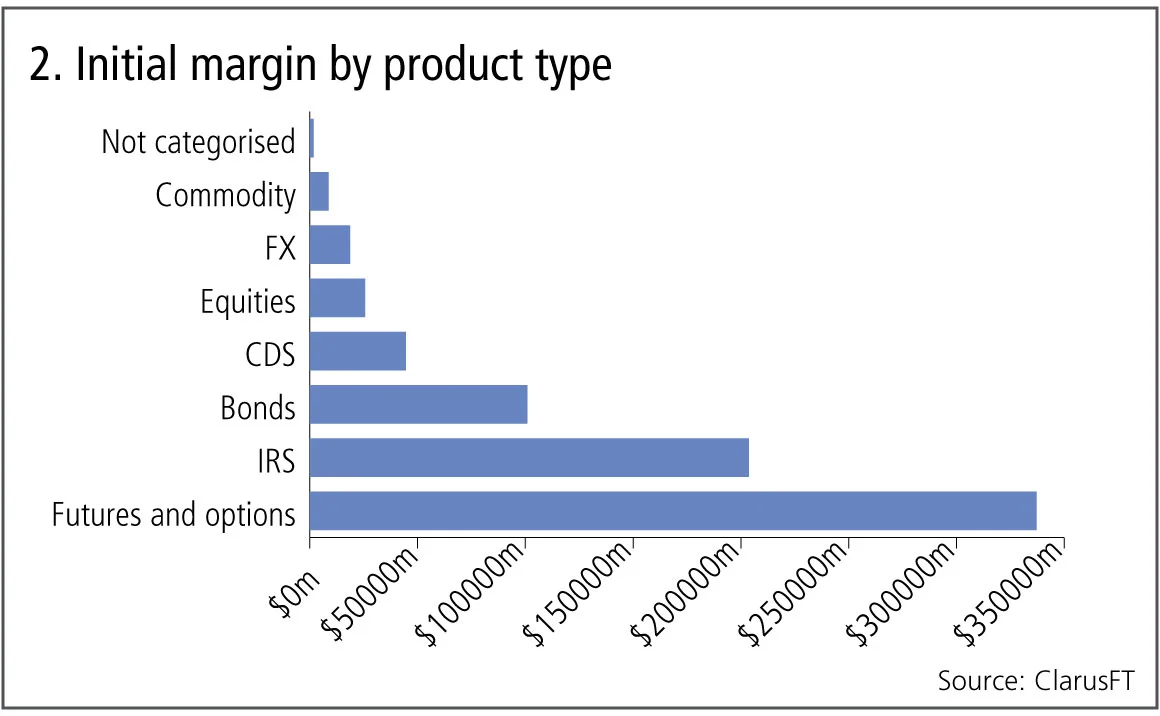

Figure 2 shows:

- Futures and options is by far the largest product type with $337 billion.

- Interest rate swaps with $204 billion.

- Bonds and repos with $101 billion.

- Credit default swaps with $44 billion.

- Equities, meaning cash equities, which as they settle on T+1 or T+2, attract low margins, with $26 billion.

- Foreign exchange and commodity are those clearing services with one of these in the name, and consequently look small as they do not include forex or commodity futures and options that are cleared at the global clearing houses such as CME or Ice.

The three largest clearing services by initial margin required as of June 28, 2019, were LCH SwapClear with $159 billion, CME Base with $97 billion and B3 (Bovespa) with $59 billion. These three represent 43% of the overall initial margin, a chunky share indeed.

Default resources

Next let’s look at the second-largest financial resource, the default fund resources that clearing houses require from members and their owners to mutualise losses. We aggregate all 50 services and show by type of default resource.

Figure 3 shows:

- Member contributions that are prefunded, so the cash or securities have been provided to the clearing service, are by far the largest at $92 billion.

- Next are member contributions that are committed to address the default of one or more members at $62 billion.

- Then member contributions required to replenish a default fund, which has been drawn down in a default, with $37 billion.

- Own capital – capital provided by the owners of the clearing service, which are either private companies or member-owned companies – is $11 billion to address a default and $3 billion and $2 billion pre-funded before and after member contributions.

- Total default resources come to $210 billion.

It would be easy to calculate ratios and say that own capital is a low percentage of aggregate resources and should be much higher, even a fixed percentage as proposed recently by a group of financial firms and commonly referred to as ‘skin in the game’. However I think that is a massive over-simplification of a complex topic and best left to an article where time and space permits a consideration of the arguments. One point to highlight is that prefunded resources total $99 billion or 47% of total resources, a healthy percentage and highlights the readily available funds to address defaults.

Cash for initial margin and default funds

In fact if we look at the disclosures of how much cash (not securities) is held by clearing houses for initial margin and default resources, we see the following:

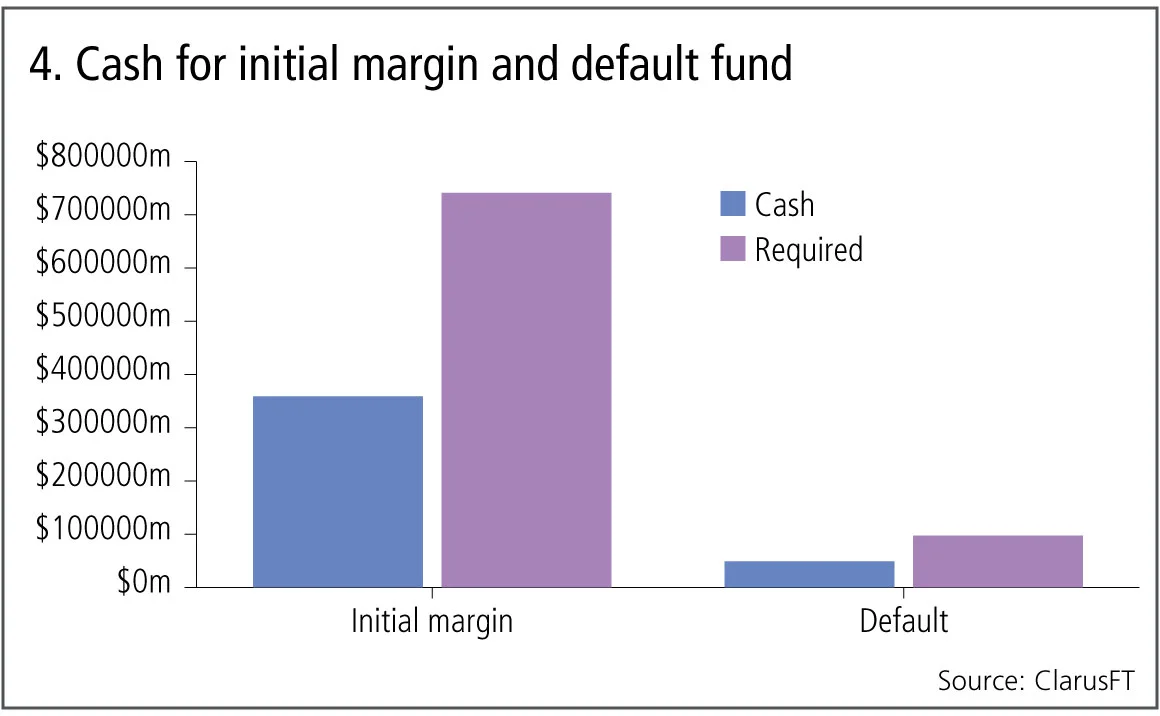

Figure 4 shows:

- $360 billion of the IM required of $740 billion is cash.

- $49 billion of the prefunded DF of $97 billion is cash.

A lot of liquid cash resources to utilise in the event of market stress and defaults, while a quick look at the largest holders shows that LCH SwapClear held $68 billion cash for IM required, while CC&G held $10 billion cash for DF contributions.

Stress loss

Given that we have highlighted the size of financial resources held by clearing houses, it is appropriate next to consider disclosures on credit risk and stress losses in extreme but plausible market conditions.

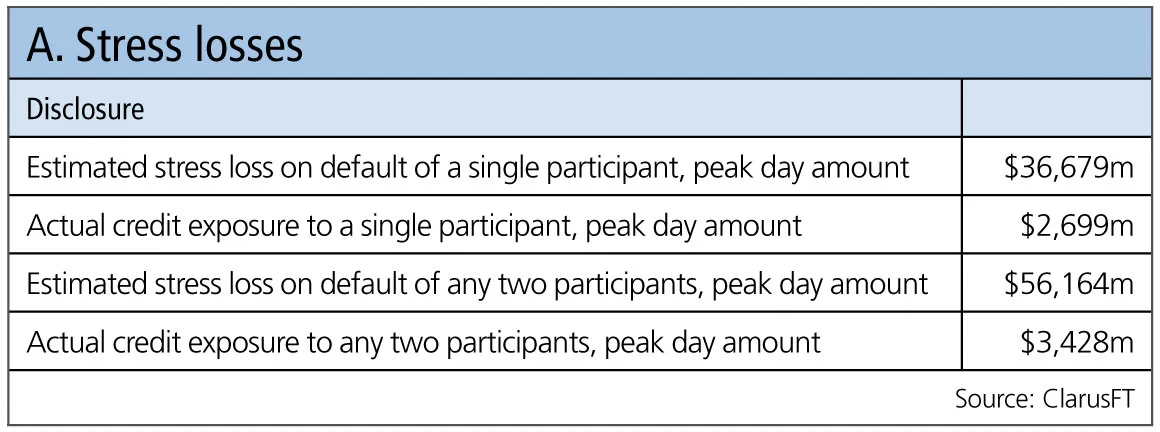

Table A shows:

- Estimated stress losses, as a peak day amount for the default of a single participant or any two participants of $37 billion and $56 billion, each of these are figures in excess of the initial margin of the participant.

Importantly the $56 billion figure is much lower than the prefunded default resources of $98 billion, let alone the total default resources of $210 billion.

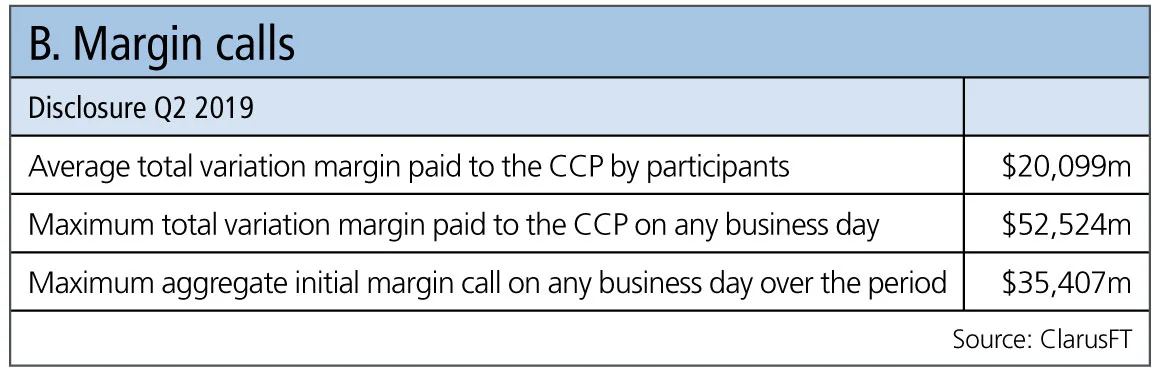

Margin calls

And last but not least, let’s take a peek at the aggregate size of margin calls.

Table B shows:

- Average total variation margin (VM) paid in the quarter ending June 28, 2019, was $20 billion.

- The maximum VM – this being an aggregate from each clearing service and which will have occurred on different days – was $52 billion.

- The maximum aggregate initial margin call, again on different days no doubt, was $35 billion, and we know some services include intra-day VM calls within this disclosure.

That’s it for now, $740 billion of initial margin, $210 billion of default resources, average daily variation margin calls of $20 billion, oodles of cash; clearing houses really are a $1 trillion systemically important market infrastructure.

Amir Khwaja is chief executive of Clarus Financial Technology.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

イタリアのスプレッド問題は(常に)信用問題というわけではない

イタリアの通貨同盟における役割に対する時折の疑念が、政治リスクプレミアムを増すと、経済学者は主張しています。

市場は決して忘れない:平方根則の持続的な影響

ジャン=フィリップ・ブショー氏はトレードの流れは資産価格に大きく、かつ長期的な影響があると主張する。

ポッドキャスト:ピエトロ・ロッシ氏による信用格付けとボラティリティ・モデルについて

確率論的手法とキャリブレーション速度の向上により、クレジットおよび株式分野における確立されたモデルが改善されます。

オペリスクデータ:カイザー社、病気の偽装により5億ドルの支払いを主導

また:融資不正取引が韓国系銀行を直撃;サクソバンクとサンタンデール銀行でAMLが機能せず。ORXニュースのデータより

大げさな宣伝を超えて、トークン化は基盤構造を改善することができる

デジタル専門家によれば、ブロックチェーン技術は流動性の低い資産に対して、より効率的で低コストな運用手段を提供します。

GenAIガバナンスにおけるモデル検証の再考

米国のモデルリスク責任者が、銀行が既存の監督基準を再調整する方法について概説します。

マルキールのサル:運用者の能力を測る、より優れたベンチマーク

iM Global Partnersのリュック・デュモンティエ氏とジョアン・セルファティ氏は、ある有名な実験が、株式選定者のパフォーマンスを評価する別の方法を示唆していると述べています。

IMAの現状:大きな期待と現実の対峙

最新のトレーディングブック規制は内部モデル手法を改定しましたが、大半の銀行は適用除外を選択しています。二人のリスク専門家がその理由を探ります。