Monthly credit data review: the Amazon effect and a rising Russian state

David Carruthers of Credit Benchmark looks at bank, sovereign and corporate credit risk data

As the world’s largest petro-state, at least by land area, Russia’s prosperity depends heavily on the behaviour of the energy markets. The sustained low prices of the 1990s brought a crippling depression; the oil boom of the 2000s led to a newly confident and aggressive Russia. The second piece of the picture is the sanctions imposed on Russian businesses, banks and individuals after the invasion of Ukraine in 2014. Though they remain in place and are set to be strengthened after the US Congress voted on renewed sanctions this month, the Russian financial sector has staged a modest recovery, with credit ratings for major Russian banks - mostly state-owned - and the Russian government itself rising gently, though still remaining below investment grade.

Energy may be part of the reason why. Though oil benchmark prices have not moved substantially over the last month, there has been a general increase in credit quality in the energy sector around the world, with upgrades outnumbering two to one - significantly better than the picture in other sectors, where the downward trend of the previous month continued.

This month we take a more detailed look at the Russian government and Russian banks, as well as retailers, asset management firms, and investment-grade gains and losses in the past 12 months.

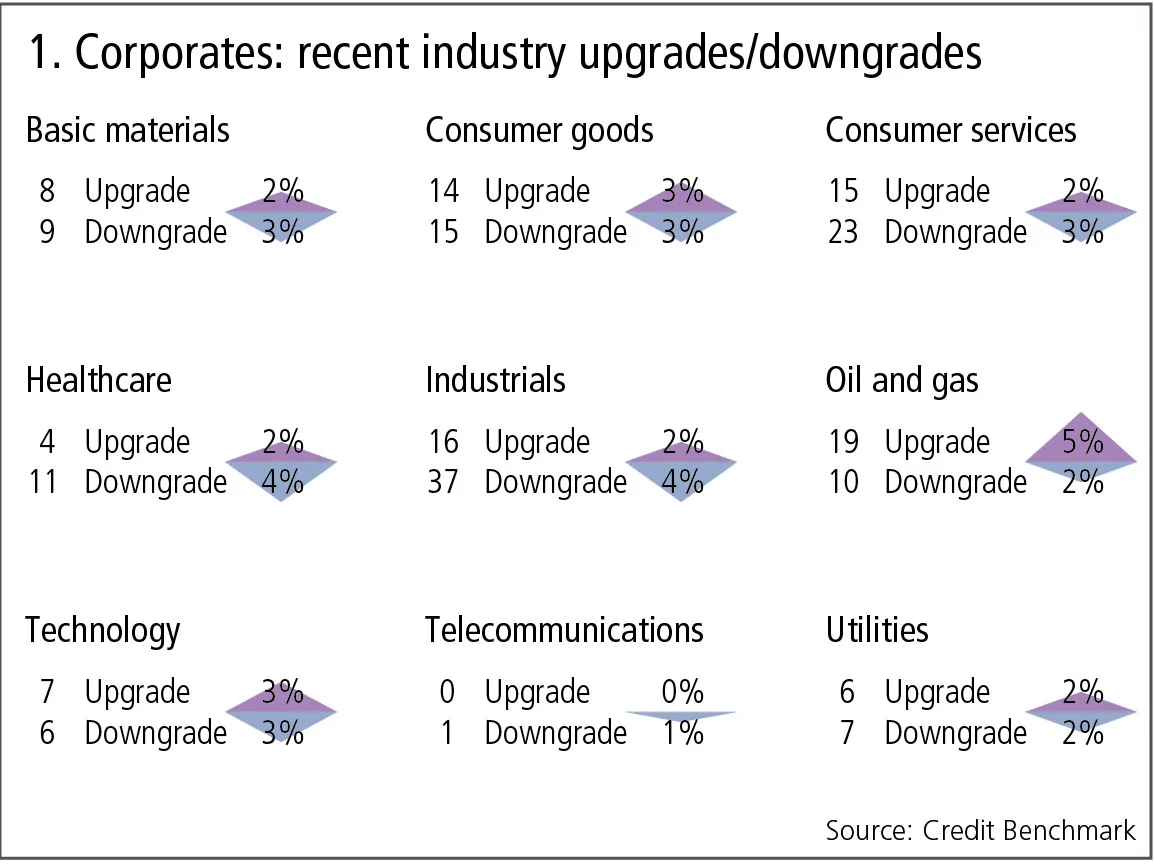

Global credit industry trends

Figure 1 shows industry migration trends for the most recent published data, as well as the history for the past 12 months.

Figure 1 shows:

- Global corporate downgrades still outnumber upgrades by 1.3 to 1, but this is more balanced than last month when the ratio was 1.4 to 1.

- Industrials continue the pattern of last month, showing 37 downgrades against 16 upgrades. Last month, the equivalent figures were 39 downgrades against 35 upgrades, so the imbalance has increased.

- Consumer services and health care also show significant imbalances, with downgrades exceeding upgrades by a significant margin.

- Consumer goods have moved to a more balanced position following recent downgrades, and oil and gas upgrades outnumber downgrades by almost two to one.

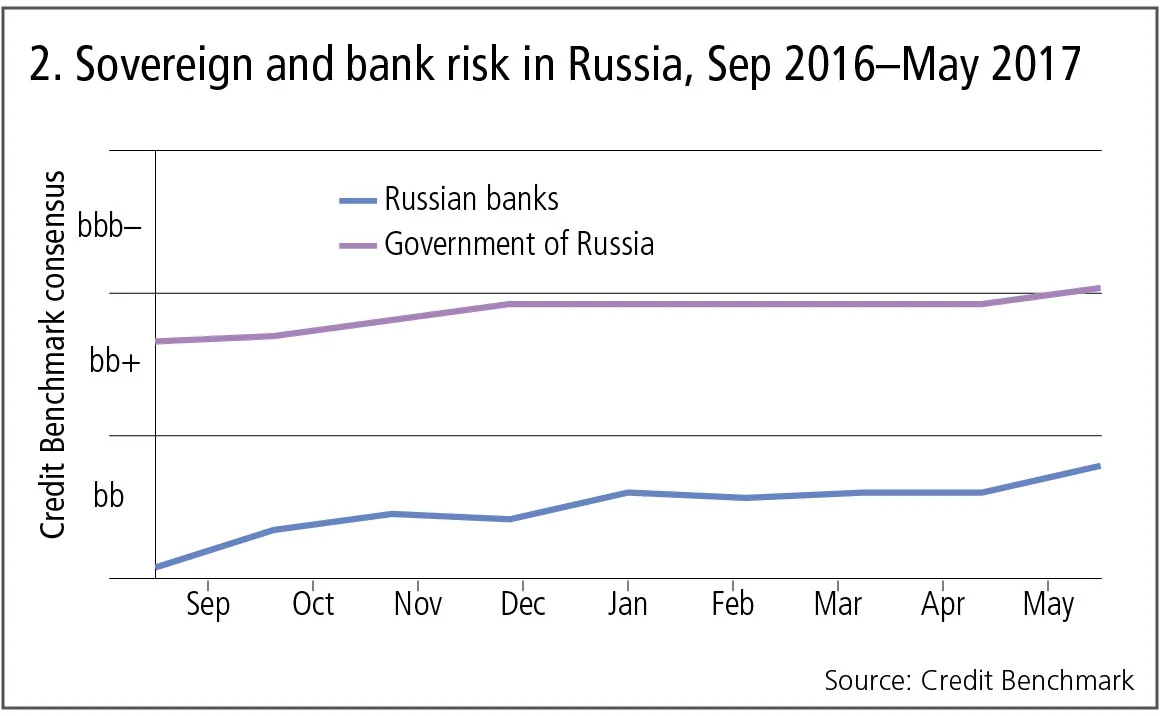

Russia: sovereign risk and banks, comparison with global banks

The Russian economy has been severely hit by sanctions and weak oil prices, but recent data shows that the credit outlook is improving. Figure 2 plots the nine-month time series of credit trends for the government of Russia and 12 of the major Russian banks.

Figure 2 shows:

- The Russian government was viewed as bb+ in September 2016. It improved every month until the end of the year, but stabilised just below the investment-grade threshold. At the end of May, IRB banks moved the Russian government to investment grade (bbb–).

- The trend for the major Russian banks (mainly state-owned) is very similar, but they are still currently viewed as non-investment grade.

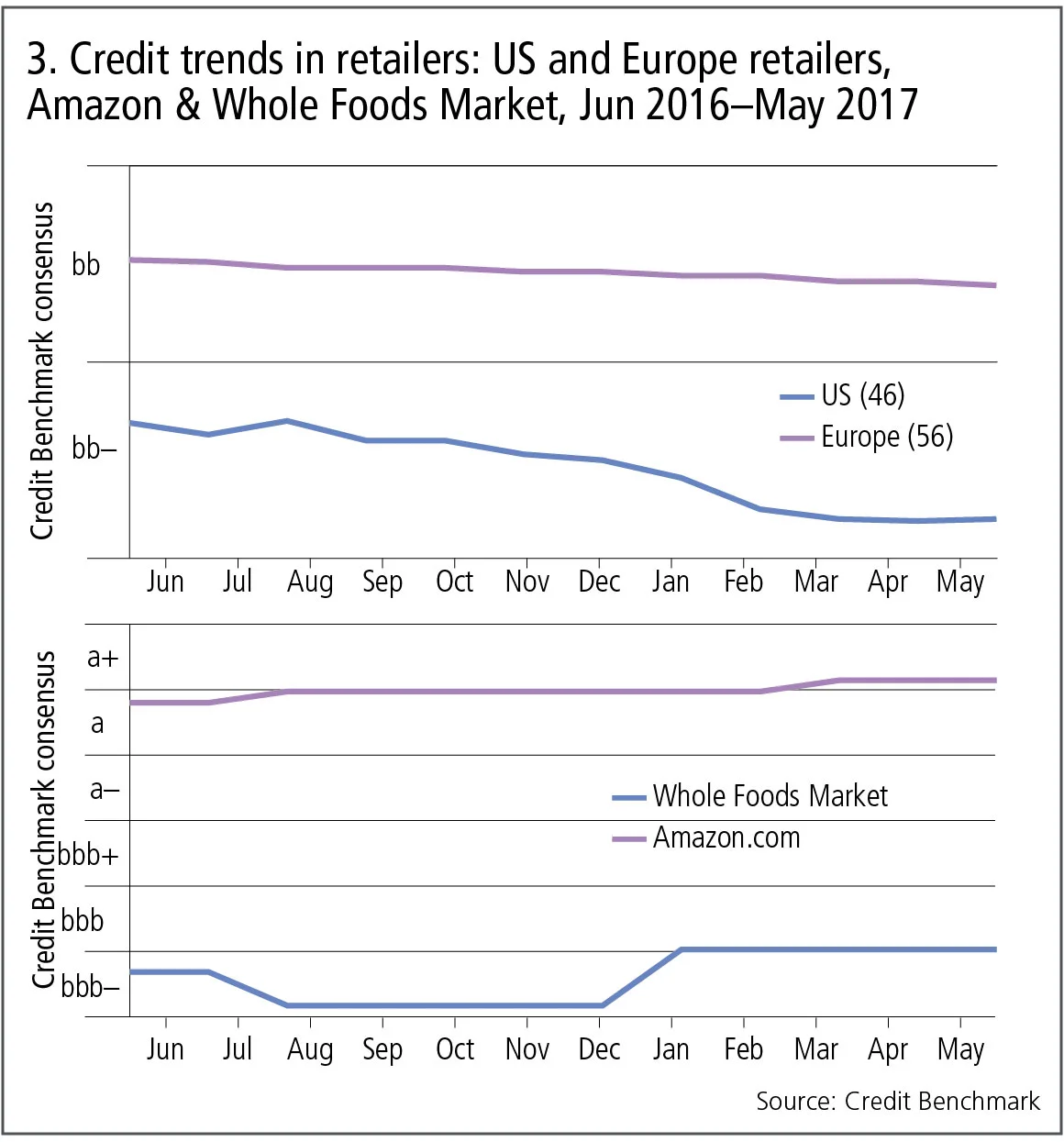

Credit trends in retailers

The traditional retail industry is suffering from the ‘Amazon effect’. But Amazon’s acquisitions of traditional retail businesses show that the impact of online competition can play out in a number of different ways. Figure 3 compares the credit trends for 46 US and 56 European apparel and general merchandise retailers as well as for Amazon and Whole Foods Market.

Figure 3 shows:

- Apparel and general retailers in both regions are already viewed as non-investment grade. The down trends have been the dominant pattern over the past 12 months. By comparison, the credit status of specialised retailers and food retailers has been stable or improving.

- The deterioration in the US is particularly noticeable; this may have implications for the future credit standing of European retailers as well.

- The credit consensus for Amazon has been steadily improving, and is significantly better than a typical corporate like Whole Foods Market.

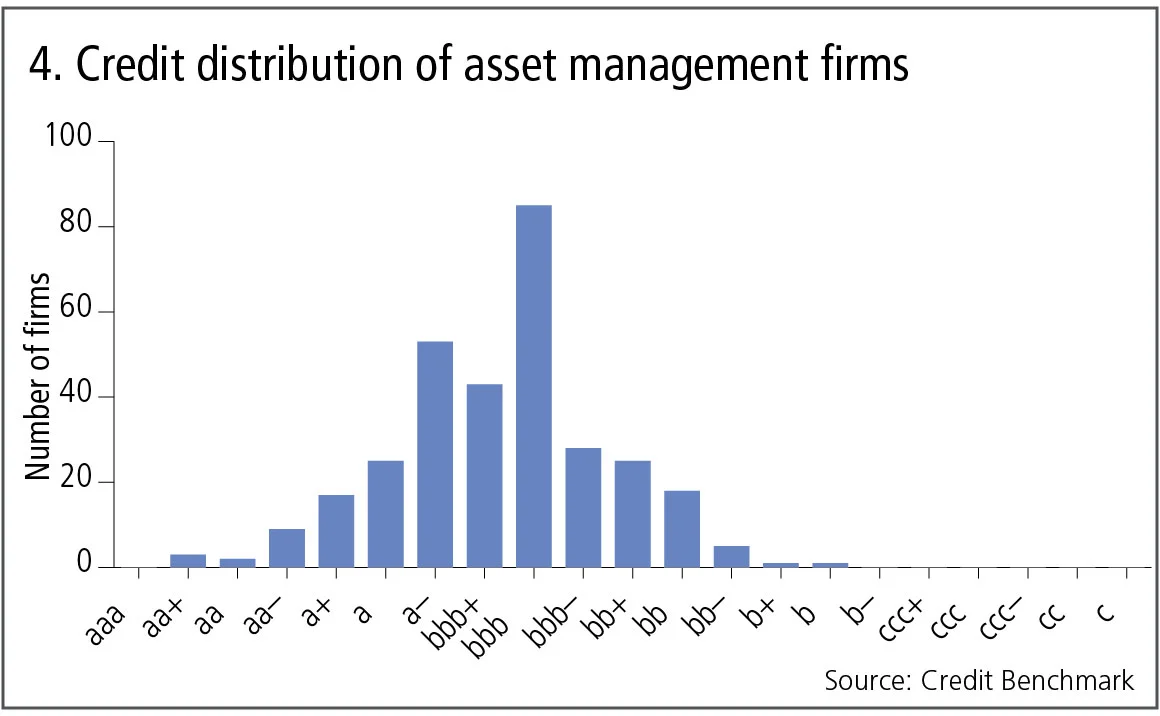

Credit distribution of asset management firms

Asset management firms rarely feature in discussions of credit risk. Figure 4 shows the range for about 350 managers. These are a mix of traditional long-only managers, hedge fund managers and hybrid management firms.

Figure 4 shows:

- Asset management companies show a surprisingly wide range of credit risks, from aa+ to b. The majority are viewed as bbb, with a large number just above this at a– and bbb+.

- This range probably reflects the size, longevity and performance of each firm, as well as the volatility and leverage of the assets that they manage. The distribution shown here indicates that the majority of firms represent a balance between these credit drivers, putting them in the same credit risk categories as a typical corporate.

- Firms in the right tail of the distribution may be excessively exposed to some of these risk sources.

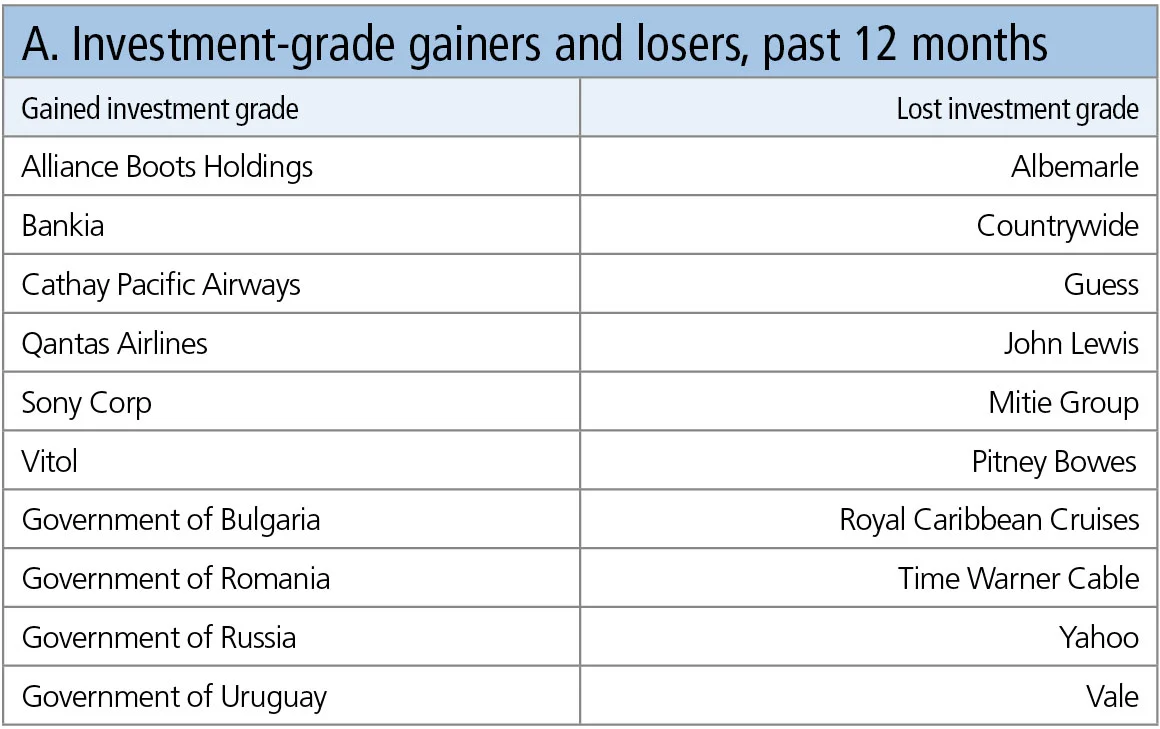

Investment grade: gainers and losers in the past 12 months

The table in Figure 5 shows some of the major borrowers that moved into, or out of, investment grade in the past 12 months. The investment-grade threshold corresponds to an annual probability of default of 0.48%.

Table A shows:

- Four sovereigns have achieved investment grade, including the recent move in Russia’s status discussed above.

- Cathay Pacific, recently voted one of the top airlines in the world, was moved to investment grade, along with Qantas. Bankia’s move to investment grade reflects recent success across the European banking industry in strengthening balance sheets.

- The Amazon effect can be seen in the downgrades of John Lewis, Guess and Time Warner Cable.

- Some of the other downgrades – Albemarle, Yahoo, Countrywide, Mitie and Royal Caribbean – are more company-specific, but the underlying economic drivers are likely to affect similar companies in the same sectors.

David Carruthers is the head of research at Credit Benchmark, a credit risk data provider.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

市場は決して忘れない:平方根則の持続的な影響

ジャン=フィリップ・ブショー氏はトレードの流れは資産価格に大きく、かつ長期的な影響があると主張する。

ポッドキャスト:ピエトロ・ロッシ氏による信用格付けとボラティリティ・モデルについて

確率論的手法とキャリブレーション速度の向上により、クレジットおよび株式分野における確立されたモデルが改善されます。

オペリスクデータ:カイザー社、病気の偽装により5億ドルの支払いを主導

また:融資不正取引が韓国系銀行を直撃;サクソバンクとサンタンデール銀行でAMLが機能せず。ORXニュースのデータより

大げさな宣伝を超えて、トークン化は基盤構造を改善することができる

デジタル専門家によれば、ブロックチェーン技術は流動性の低い資産に対して、より効率的で低コストな運用手段を提供します。

GenAIガバナンスにおけるモデル検証の再考

米国のモデルリスク責任者が、銀行が既存の監督基準を再調整する方法について概説します。

マルキールのサル:運用者の能力を測る、より優れたベンチマーク

iM Global Partnersのリュック・デュモンティエ氏とジョアン・セルファティ氏は、ある有名な実験が、株式選定者のパフォーマンスを評価する別の方法を示唆していると述べています。

IMAの現状:大きな期待と現実の対峙

最新のトレーディングブック規制は内部モデル手法を改定しましたが、大半の銀行は適用除外を選択しています。二人のリスク専門家がその理由を探ります。

地政学的リスクがどのようにシステム的なストレステストへと変化したのか

資源をめぐる争いは、時折発生するリスクプレミアムを超えた形で市場を再構築しています。