Monthly credit data review: gloomier than spreads suggest

David Carruthers of Credit Benchmark looks at banks’ credit risk data

Credit risk data is widely available for sovereigns and large corporates, but updates are infrequent and smaller companies are often ignored. In this series of monthly articles, David Carruthers, head of research at Credit Benchmark, discusses monthly credit risk trends in rated and unrated obligors based on bank-sourced data.

The first-quarter rally in equity markets was accompanied by a narrowing in high-yield credit spreads, but market measures of credit risk can be distorted by liquidity and technical factors. Banks’ own measures of credit risk offer a different – and clearer – picture of the underlying trend.

The Credit Benchmark dataset is based on internally modelled credit ratings from a pool of 13 contributor banks. These are mapped into a standardised 21-bucket ratings scale, so downgrades and upgrades can be tracked on a monthly basis. Obligors are only included where ratings have been contributed by at least three different banks, yielding a total dataset of more than 8,000 names.

The data for February is mixed, but in general is slightly more pessimistic than credit spread trends would imply. One-year default probabilities for both investment-grade (IG) and non-investment-grade (NIG) names rose in February, for example; over the past six months, corporate as well as financial obligors have migrated down the ratings scale, with downgrades heavily outnumbering upgrades by almost two to one.

By sector, downward migration is most pronounced for oil and gas and utilities names – eight upgrades are accompanied by 20 downgrades for the former, and three upgrades versus 12 downgrades for the latter.

There are some more optimistic signs, though. Financial downgrades are slowing; the February data even includes a small number of aaa-rated financials. Among corporates, the picture varies by sector, with downgrades and upgrades more or less in balance among consumer services and industrial obligors.

Global credit trends

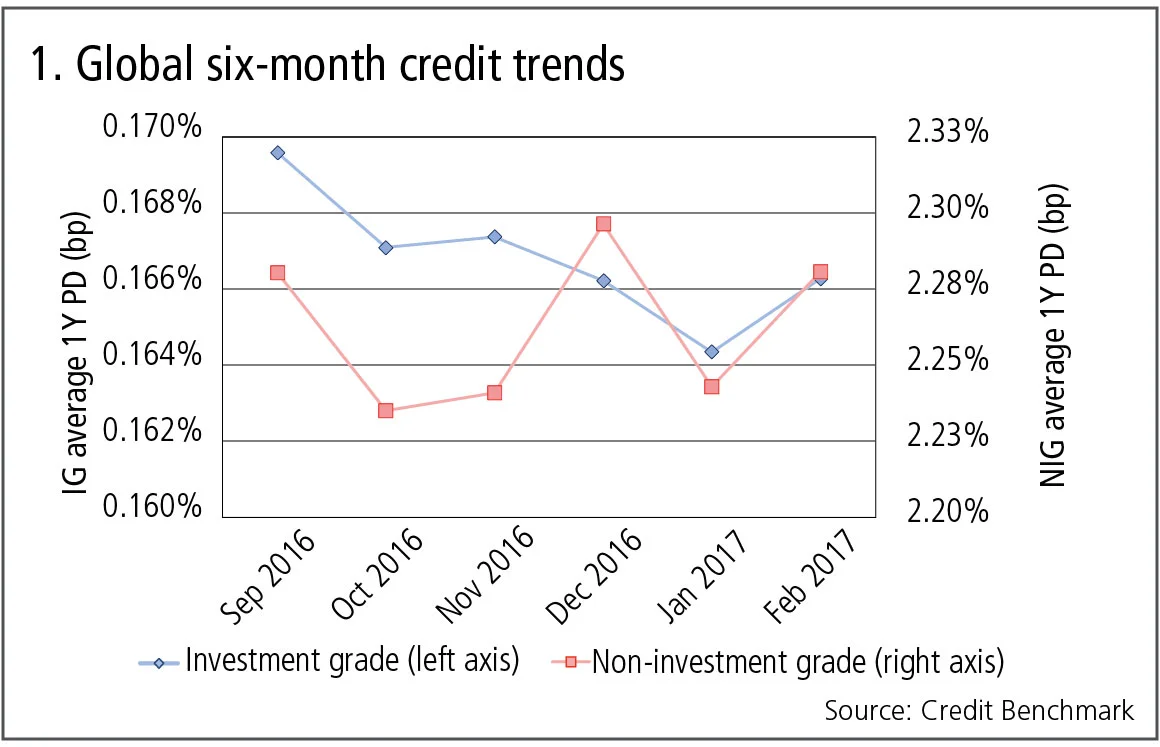

Figure 1 shows trends for the most recent six months of published data. The IF series is based on a fixed sample of 3,470 corporate obligors and the NIG series is based on a fixed sample of 1,475 corporate obligors. Of the two, the IG credit trend has been more stable.

Figure 1 shows:

- The trend decline in investment grade credit risk over recent months reversed in February; the current one-year average default probability is 16.6 basis points per annum.

- Non-investment grade credit risk has been more volatile, but also turned up in February. The current one-year average credit risk is 228bp per annum.

Corporate credit distributions

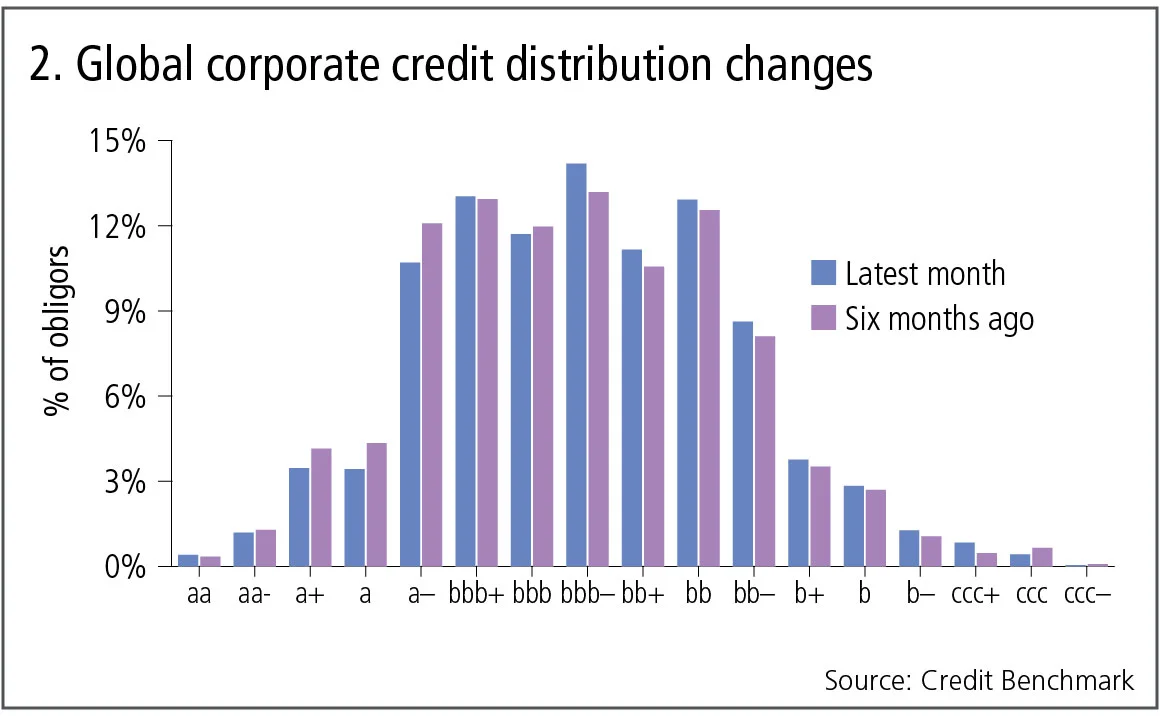

The distribution of corporate credit risk now and six months ago is shown in figure 2.

Figure 2 shows:

- The main six-month changes are small reductions in the proportion of names in the higher-quality credit categories and an increase in those in the middle categories, on the boundary between investment grade and non-investment grade.

- The credit distribution of corporate obligors is widely dispersed, with bbb- as the largest category, accounting for about 14% of all obligors.

- The published dataset does not include any corporates in the aaa or aa+ categories.

Financial credit distributions

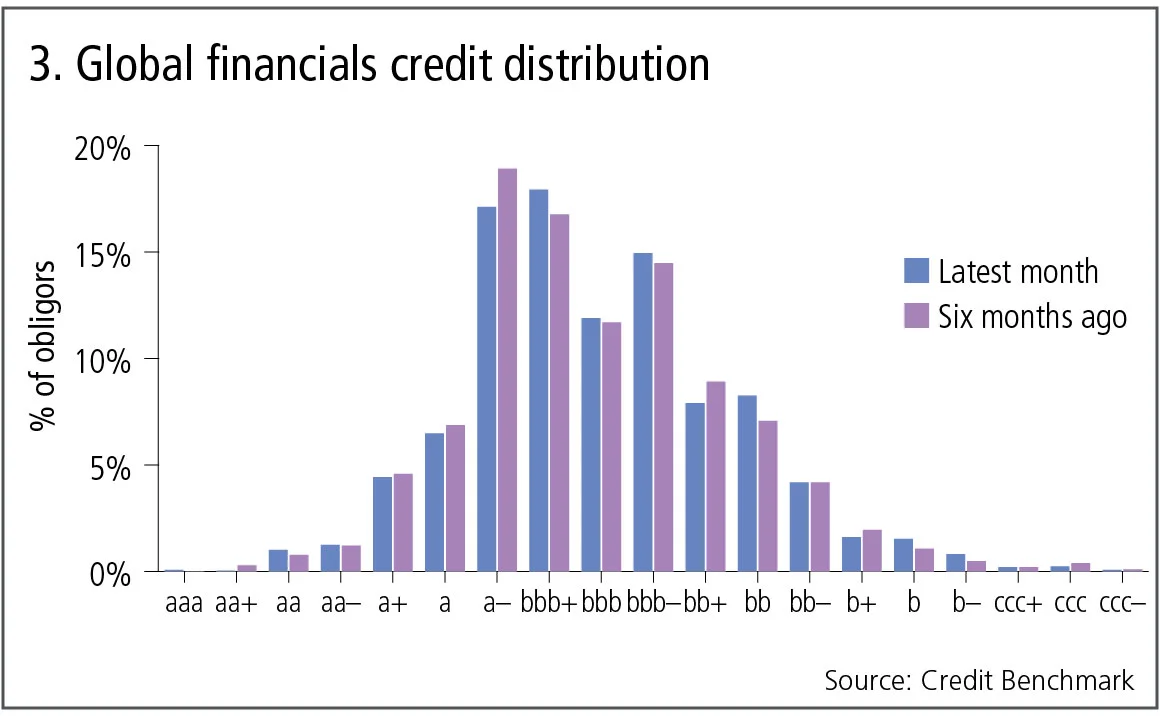

The distribution of financial credit risk now and six months ago is shown in figure 3.

Figure 3 shows:

- The main six-month changes are small reductions in the proportion of names in the a- credit categories and an increase in those in the bbb+ and bbb- categories.

- The credit distribution of financial obligors shows less dispersal than for corporates, with bbb+ as the largest category, accounting for about 17% of all obligors.

- The most recent dataset now includes a small number of financials in the aaa category, including government-owned KFW BankenGruppe.

Corporates and financials: upgrades and downgrades

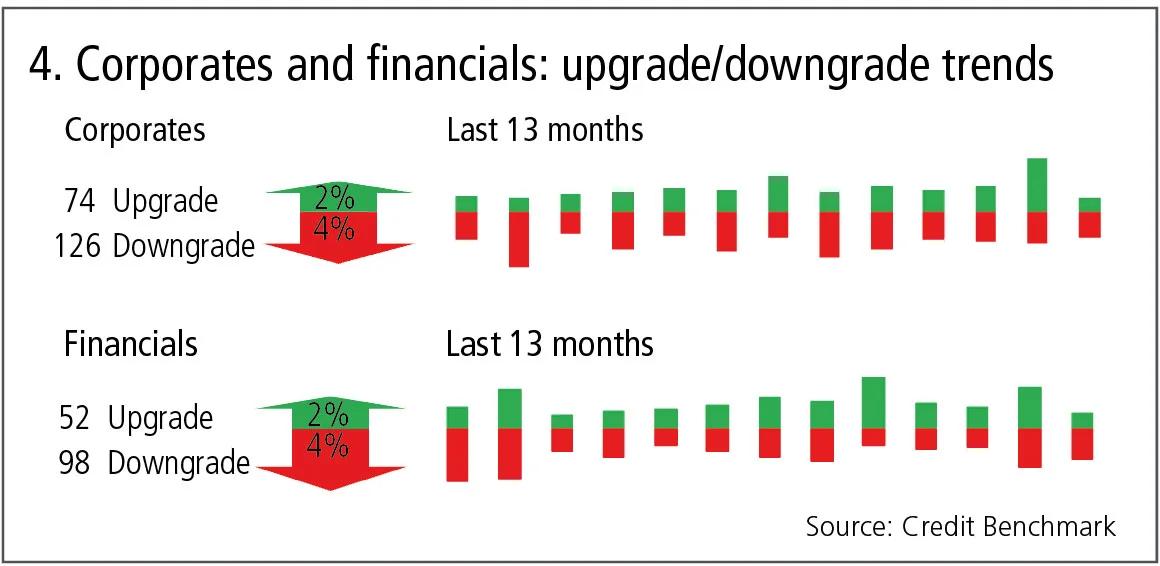

Figure 4 shows the frequency of upgrades and downgrades for the most recent month as well as for the previous 12 months.

Figure 4 shows:

- Recent global corporate downgrades outnumber upgrades by a significant margin (126 versus 74).

- Financials show a similar pattern to corporates, with downgrades outnumbering upgrades by almost two to one (98 versus 52).

- However, financials show a clear trend towards fewer downgrades over time, whereas for corporates, the downgrade trend is more mixed. The pattern of upgrades is more volatile for both categories.

Industry upgrades and downgrades

Figure 5 shows the frequency of upgrades and downgrades for the most recent month across the main industries.

Figure 5 shows:

- In a reversal of recent trends, downgrades tend to outnumber upgrades over the past month.

- The exceptions are consumer services and industrials, with upgrades and downgrades more or less in balance.

- Oil and gas and utilities show the largest imbalances, with downgrades outnumbering upgrades by around three to one.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

オペリスク・データ:企業スパイがBBVAに脅威をもたらす

他にも:BofAがエプスタイン氏との関与疑惑で追及されています。また、少数株主がブルックフィールドに異議を唱えています。データ提供:ORX News

AI政治の台頭

MASの顧問であるデビッド・ハードーン氏は、AIを単なる一つの技術として扱うべきではないと述べています

AIリスク管理と能力制御への移行

リスク管理者によると、検証の枠組みを見直すことで、銀行はイノベーションと規制上の要件を両立させ、強固なリスク管理体制を維持することができます

トークン化された商品市場は、経済の円滑な運営に寄与する可能性がある

暗号資産の専門家は、実物資産をブロックチェーンに移行することで、担保に関する摩擦が緩和されると主張しています

GenAIの時代において、未だに優れたモデルが必要なのはなぜなのか?

ジャン=フィリップ・ブショー氏は、モデルが人工知能をレジームシフトの過程で導き、過学習から遠ざけることができると述べています

取引のスピードがガバナンスを上回る時:一瞬の統制の隙間

デリバティブの専門家によると、光駆動型エレクトロニクスの新たな形態が、市場インフラにおける次のリスクとなる可能性があるとのことです

先物とオプションが示す戦争のコスト

現物価格は大きな混乱を示していますが、先物市場はこれが一時的なものだと示唆しており、オプション市場は不安定な状況が続くと示唆しています

担保に関して、TINAはTIAになることができるのか

あるエコノミストは、レポ取引やデリバティブ取引における担保としての米国債の優位性は、もはや揺るぎないものではないと指摘しています