Swaps data: cleared volumes drop for all markets – except FX

Smaller CCPs make market share gains in a quarter of double-digit declines for rates and credit

Longstanding growth in cleared over-the-counter derivatives volumes came to an abrupt halt in the fourth quarter of 2019, as all products other than foreign exchange posted double-digit declines compared with the same quarter in 2018.

Volumes of interest rate swaps in dollars and euros dropped 27% and 19% respectively, while credit default swap volumes in dollars and euros were down 35% and 27%. It could just be a blip, as data for the period January 2 to February 21, 2020, shows a recovery with volumes largely similar to the equivalent period in 2019. Foreign exchange non-deliverable forwards stand out as the only product where volumes actually increased in the fourth quarter of 2019 compared with a year earlier, though the 5% growth rate is anaemic compared to prior quarters.

Amid the drop in activity, some interesting market share developments emerged, as smaller players eked out gains. The standout swing came at Eurex, which increased its share in euro interest rate swaps from 1.7% to 5.5%. In credit markets, LCH CDSClear increased its share in euro credit default swaps from 12.8% to 16.5%.

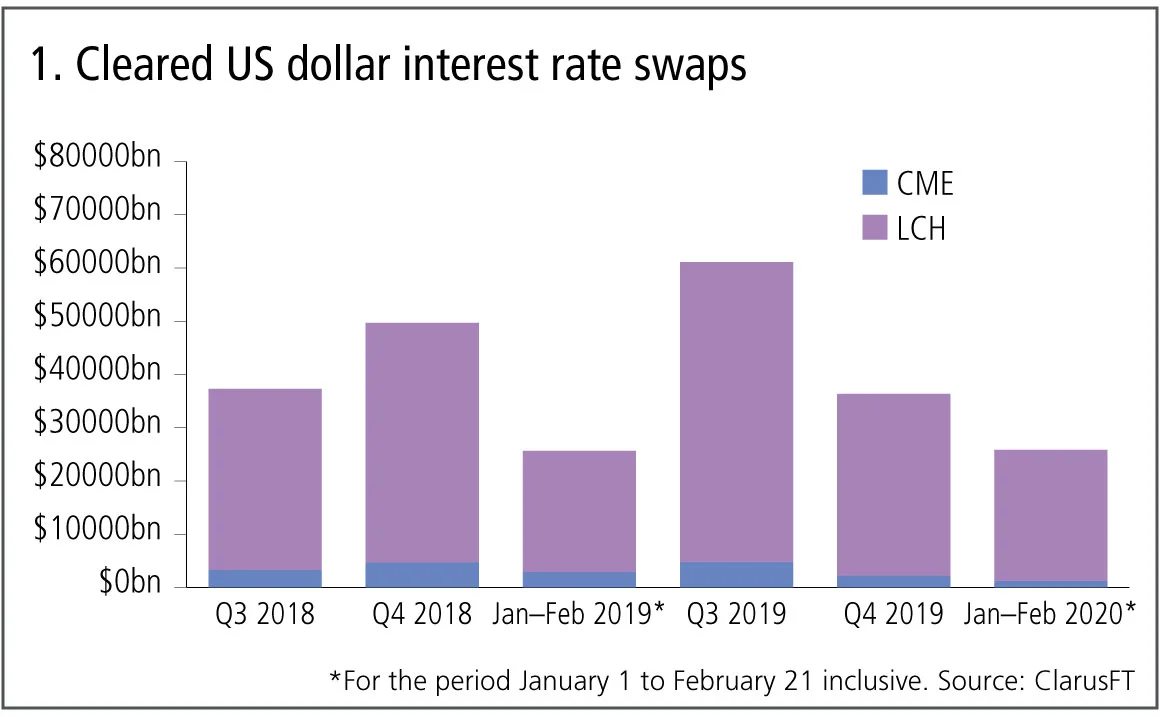

Cleared US dollar swaps

Let’s start with the largest product – cleared US dollar interest rate swaps. We include all clearable types – vanilla fixed versus float, overnight index, basis, zero coupon and variable notional – and use single-sided gross notional volumes.

Figure 1 shows:

- Q4 2019 volumes at $36 trillion are 27% lower than a year earlier and 40% lower than Q3 2019.

- Volumes in the period January 1 to February 21, 2020, are 1% higher than the corresponding period in 2019.

- LCH SwapClear with a 94% share in Q4 2019, up from a 92% share in Q3 2019, and CME with 6%, down from 8%.

- LCH SwapClear down $10.8 trillion or 24% from a year earlier.

- CME down $2.5 trillion or 53% from a year earlier.

The much lower volumes in the fourth quarter of 2019 is a real contrast to the large gains we saw in the second and third quarters of 2019, while the early signs in 2020 are that the first quarter will be similar to the corresponding quarter a year earlier.

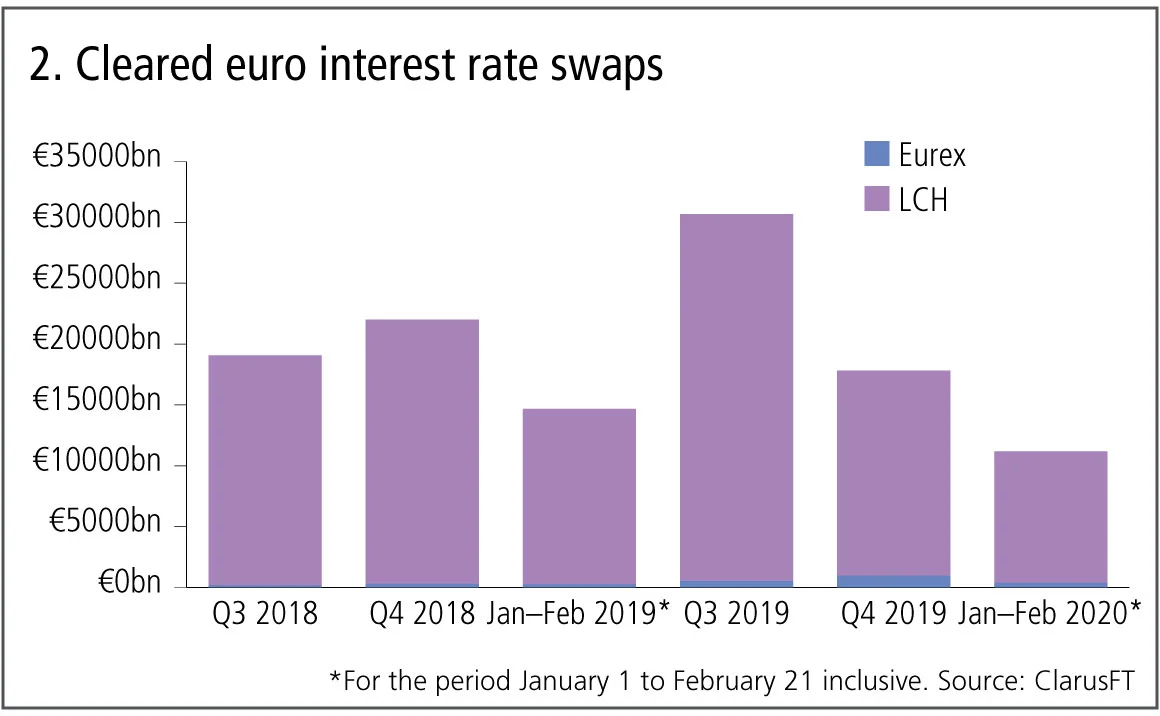

Cleared euro swaps

Next, cleared euro interest rate swaps, all clearable types.

Figure 2 shows:

- Q4 2019 volumes at €18 trillion ($20 trillion) are 19% lower than a year earlier and 42% lower than Q3 2019.

- Volumes in the period January 1 to February 21, 2020, are 24% lower than the corresponding period in 2019.

- LCH SwapClear with 94.5% share in Q4 2019, down from 98.3% share in Q3 2019 and Eurex with 5.5% share up from 1.7%, though in the early part of 2020, this is down to 3.3%.

- LCH SwapClear is down 22%, or €4.9 trillion from a year earlier.

- Eurex is up 224% or €0.7 trillion from a year earlier.

Euro volumes are showing similar drops to US dollar volumes, while Eurex continues its high growth rates with its share increasing from 1.7% to 5.5% between the third quarter and fourth quarters of 2019.

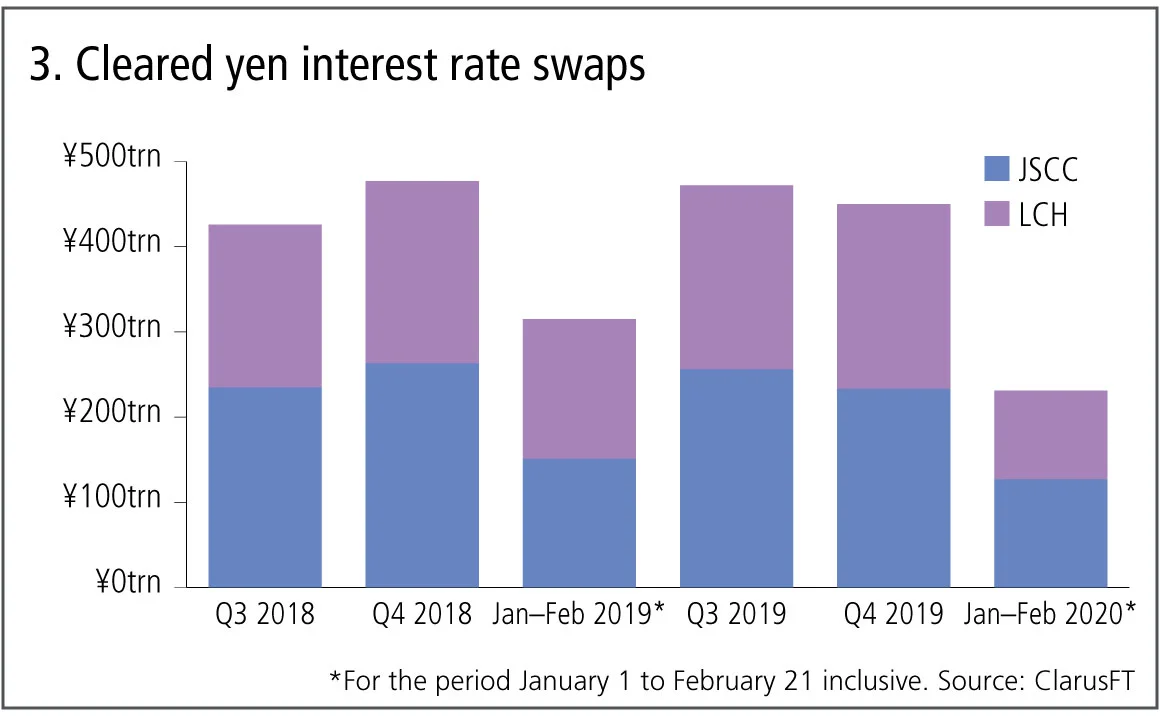

Cleared yen swaps

Figure 3 shows:

- Q4 2019 volumes at 450 trillion yen ($4.17 trillion) are 6% lower than a year earlier and 5% lower than Q3 2019.

- Volumes in the period January 1 to February 21, 2020, are 27% lower than the corresponding period in 2019.

- JSCC with 52% share and LCH SwapClear with 48% in Q4 2019 – a loss of 2% in JSCC’s share compared with Q3 2019.

- JSCC is down 11% in Q 2019 from a year earlier.

- LCH is up 2% from a year earlier.

The cleared yen swap volumes market share remains fairly evenly split between JSCC and LCH, but with LCH clawing back 2% in the fourth quarter of 2019.

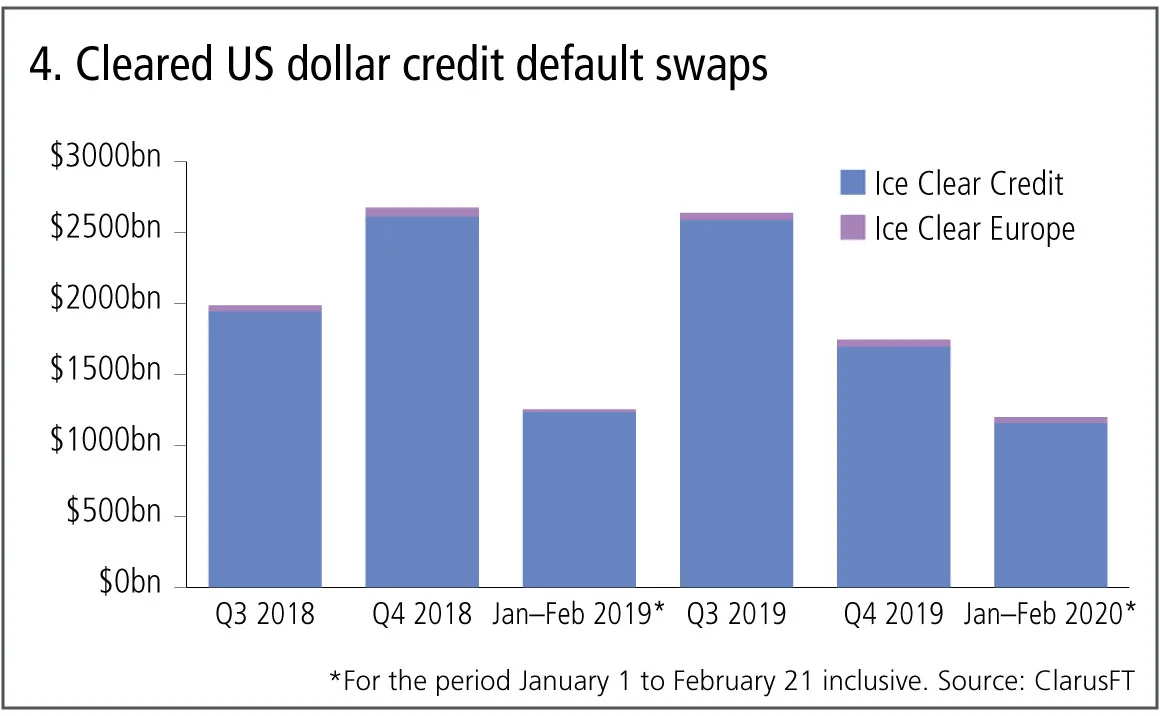

Cleared US dollar credit default swaps

Let’s now switch focus to credit derivatives and the volume of credit indexes and single names in US dollars.

Figure 4 shows:

- Q4 2019 volumes at $1.75 trillion are down 35% from a year earlier and down 34% from Q3 2019.

- Volumes in the period January 1 to February 21, 2020, are 4% lower than the corresponding period in 2019.

- Ice Clear Credit dominates with 97% share.

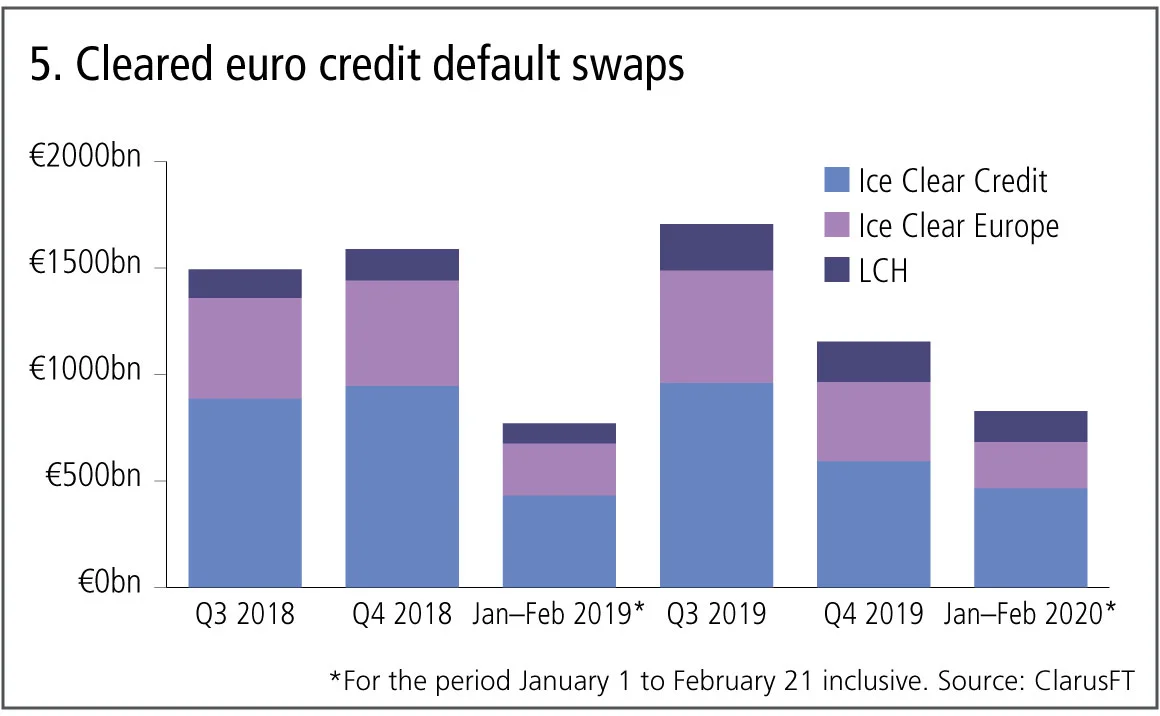

Cleared euro credit default swaps

Next, the volume of credit indexes and single names in euro.

Figure 5 shows:

- Q4 2019 volumes at €1.15 trillion are 27% lower than a year earlier and 32% lower than Q3 2019.

- Volumes in the period January 1 to February 21 are 8% higher than the corresponding period in 2019.

- Ice Clear Credit with 51.3%, Ice Clear Europe 32.3% and LCH CDSClear with 16.5% market share in Q4 2019, which compares with 56.3%, 31.9% and 12.8% in Q3 2019.

- Ice Clear Credit down 37%, Ice Clear Europe down 25% and LCH CDSClear up 28% from a year earlier.

Cleared credit derivatives volumes in euro are lower by a similar amount to US dollars, with Ice Clear Credit the largest. LCH CDS Clear is growing faster from a lower base and is the only CCP to increase volume in the fourth quarter.

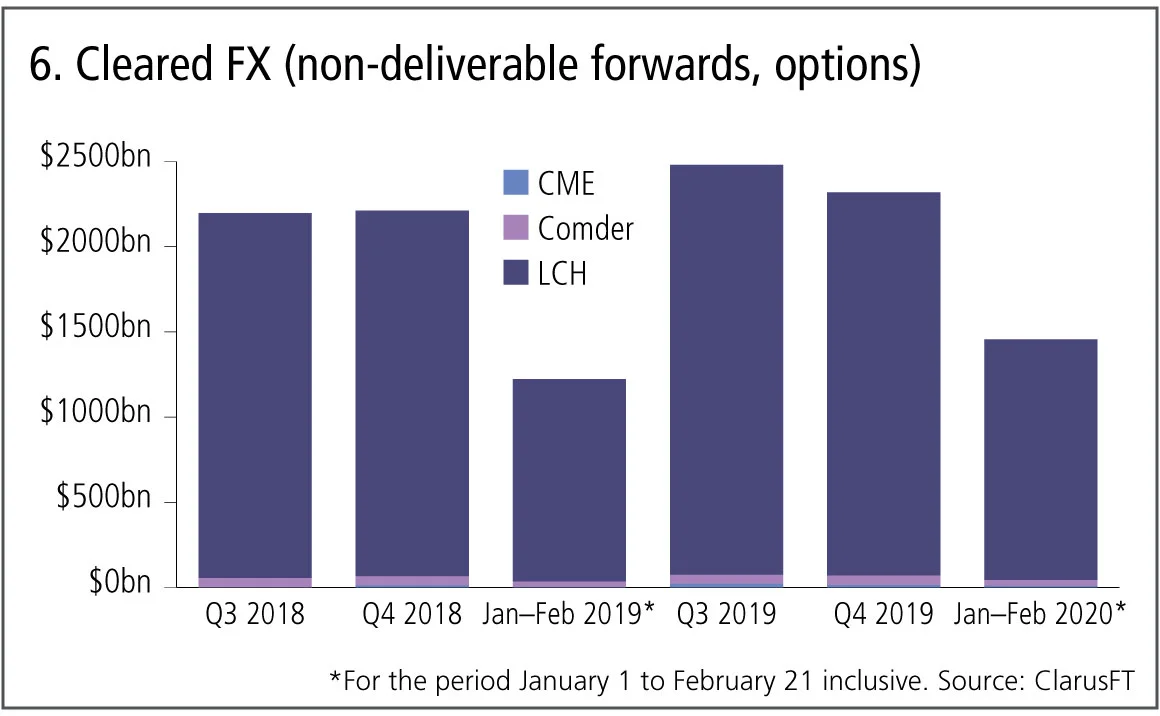

Cleared non-deliverable forwards

Finally, cleared non-deliverable forwards and FX options.

Figure 6 shows:

- Q4 2019 volumes at $2.3 trillion are 5% higher than a year earlier but down 7% from Q3 2019.

- LCH ForexClear, with 97% share in the quarter, unchanged from prior quarters.

- Comder with 2.4% and CME with 0.6%.

Cleared non-deliverable forwards are the only product we have looked at that has higher volumes in the fourth quarter of 2019 compared with a year earlier.

Amir Khwaja is chief executive of Clarus Financial Technology

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

オペリスク・データ:HSBC、外部による不正行為で4億ドルの損失を被る

また、中国における無許可取引への取り締まり強化、ソシエテ・ジェネラル銀行の保険不適切販売問題についても。データ提供:ORX News

ヴィニシウスの運命:ワールドカップの組み合わせ抽選における「運」の数値化

ジュリアン・ギヨン氏は、今夏の大会においてバイアス、分散、そして運がチームにどのような影響を与えるかを解説し、ポートフォリオ・マネージャーにとってのより広範な意義についても考察しています

G-Sibの資本サーチャージ:指数化と平均化がインセンティブに与える影響

資本リスク戦略担当者は、バーゼルIIIの最終局面が米国の大手銀行の行動に与える影響を予測しています

ポッドキャスト:アビ=ジャバー氏とリー氏が語る「スティッキー」なボラティリティ問題

二人は、VIX、SPX、SSRを同時に捉えるためのモデルについて議論しています

市場は未来を非常に歪んだ形で捉えている

ジャン=フィリップ・ブショー氏は、割引のパラダイムはより現実的なものへと適応すべきだと述べています

オペリスクデータ:サイバー攻撃が暗号資産プロトコルを揺るがす

他にも:JPモルガンが投資家の損失をめぐり罰金処分を受けた、Symetraのメソジスト系年金基金をめぐる混乱など。データ提供:ORX News

予測市場は、炭鉱のカナリアのような役割を果たすことがある

リスクの専門家によると、Polymarketなどのプラットフォームにおける契約価格は、リスク管理やヘッジの指標となり得るとのことです

AIエージェントがリスク管理者の課題解決にどう役立つ

シティのリスク専門家は、取引や融資承認に関する構造化データと非構造化データを統合し、リスクに関する単一かつ統一されたビューを構築する自律型AIツールについて概説しました