Swaps data: are the new RFRs on track to replace Libor?

Progress on volumes of SOFR and Sonia swaps and futures

In just over two years’ time, Libor could cease to exist, so it’s no surprise to see regulators turning up the volume on transition to risk-free rates (RFRs). There’s a clear trend of rising activity in futures and over-the-counter swaps linked to replacement rates. What’s not so clear is whether participants are switching out of Libor exposures.

September 2019 was a watershed for US Libor’s successor, the Secured Overnight Financing Rate, or SOFR. The repo-based rate spiked to 5.25% on September 17, from just 2.43% the previous day. CME SOFR futures clocked up record trading volume in response, helping the contracts on their way to an impressive 11-fold jump in open interest compared to a year prior.

There are positive signs in the UK too, as swaps linked to the Sterling Overnight Index Average, or Sonia, continue to increase. But activity in sterling Libor swaps has also been rising. Worryingly for regulators, there’s little sign of a move away from Libor contracts expiring from January 2022, when the benchmark will be left to wither.

Libor transition in the UK may have enjoyed a head-start thanks to the selection of a pre-existing rate, but SOFR seems to have caught a slipstream. September’s volume jump may yet prove to be an anomaly, but there are clear triggers for wider SOFR adoption – most notably, a planned 2020 move by clearing houses to replace Fed funds with SOFR as the discount rate for all US dollar swaps.

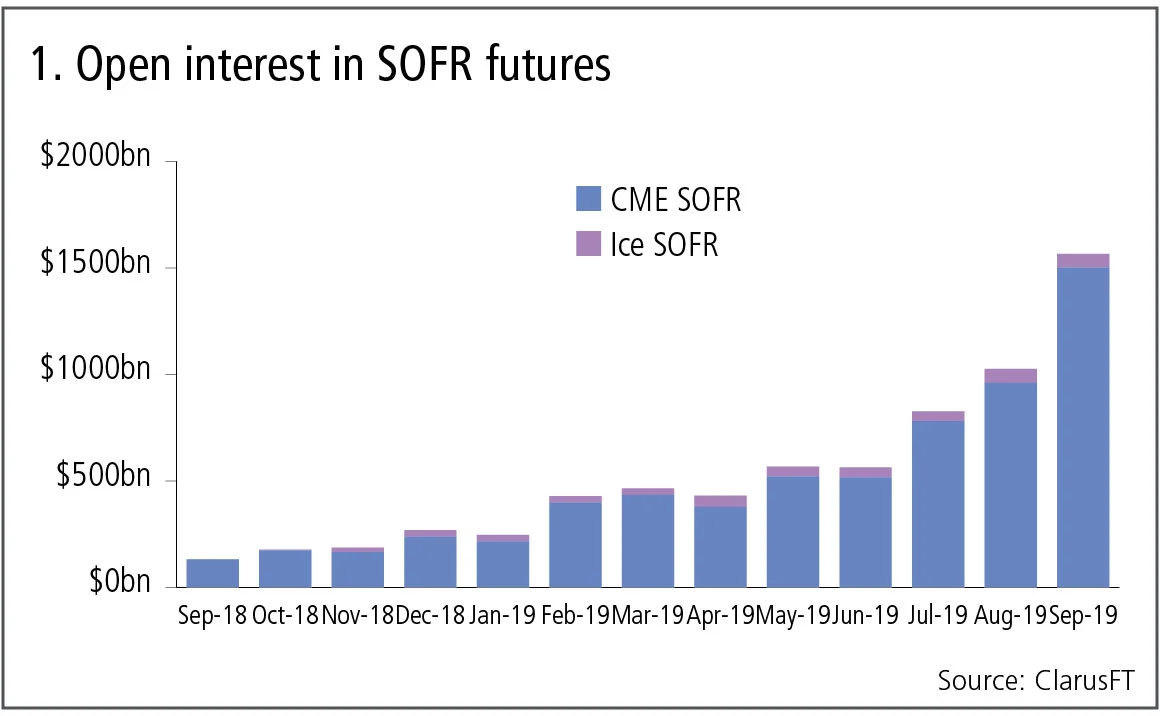

SOFR futures

Let’s start with the largest currency, US dollars and futures on the SOFR index. We can chart the growth in open interest over the past year for CME and Ice contracts.

Figure 1 shows:

- September 2019 has been a stellar month for CME SOFR contracts, which now have $1.5 trillion notional of open interest, with significant increases from September 16 onwards. This was most likely linked to the jump in SOFR and Federal Reserve actions in the repo market, which have been widely commented on.

- Ice SOFR futures have open interest of $64 billion

- A total in September 2019 of $1.57 trillion open interest compared to $132 billion in September 2018 – massive growth indeed.

To put this into perspective, on September 27, 2019, CME Fed funds futures open interest was $10.6 trillion and CME Eurodollar was $12 trillion, which means that CME SOFR futures open interest is now 12.5% of CME Eurodollar open interest. That is a meaningful chunk and a significant achievement, it will be very interesting to see if the remaining months in 2019 live up to the massive increase seen in September.

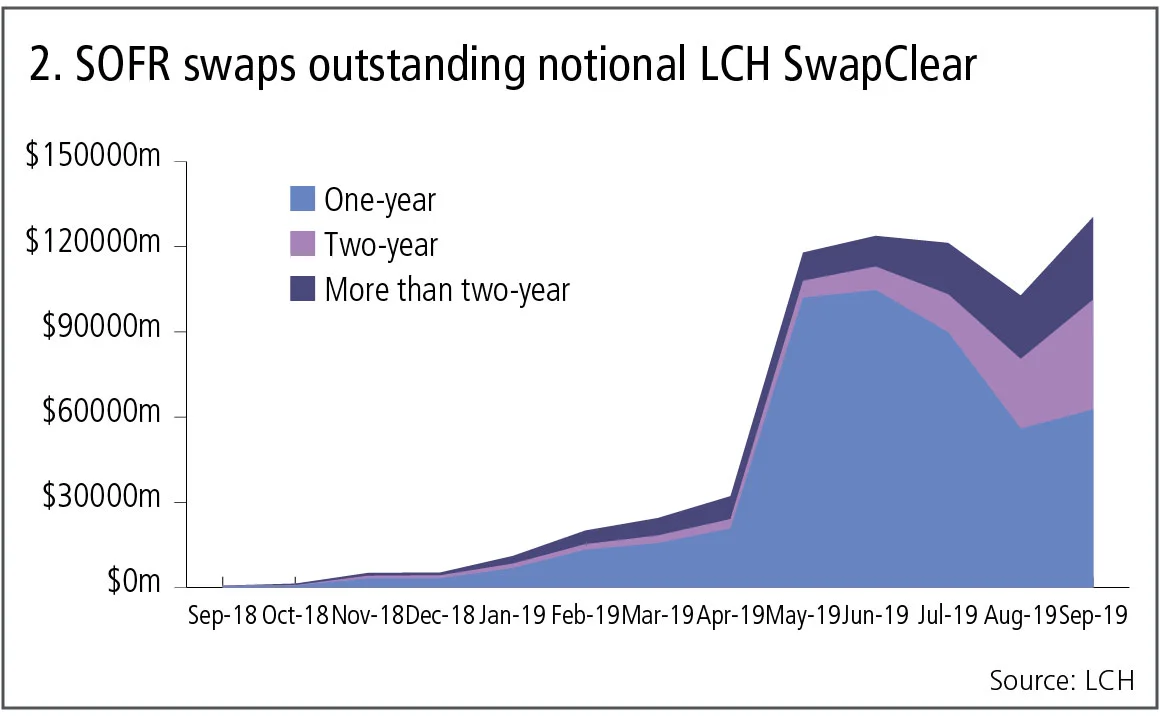

SOFR swaps

Next let’s look at progress in SOFR swaps trading.

Figure 2 shows:

- Outstanding notional (single-sided) of SOFR swaps at LCH SwapClear over the past year, broken out by tenor.

- A big jump in May 2019, flat for two months, down in August and back up to a new high in September.

- At the end of September, total outstanding notional stood at $130 billion, so similar to SOFR futures open interest in September 2018, meaning SOFR swaps volume is lagging a year behind futures.

Also, September sees a much higher proportion of two-year and greater than two-year tenor SOFR swaps compared to under one year. Longer tenors, where Libor swaps dominate, are crucial to a wider use of SOFR swaps.

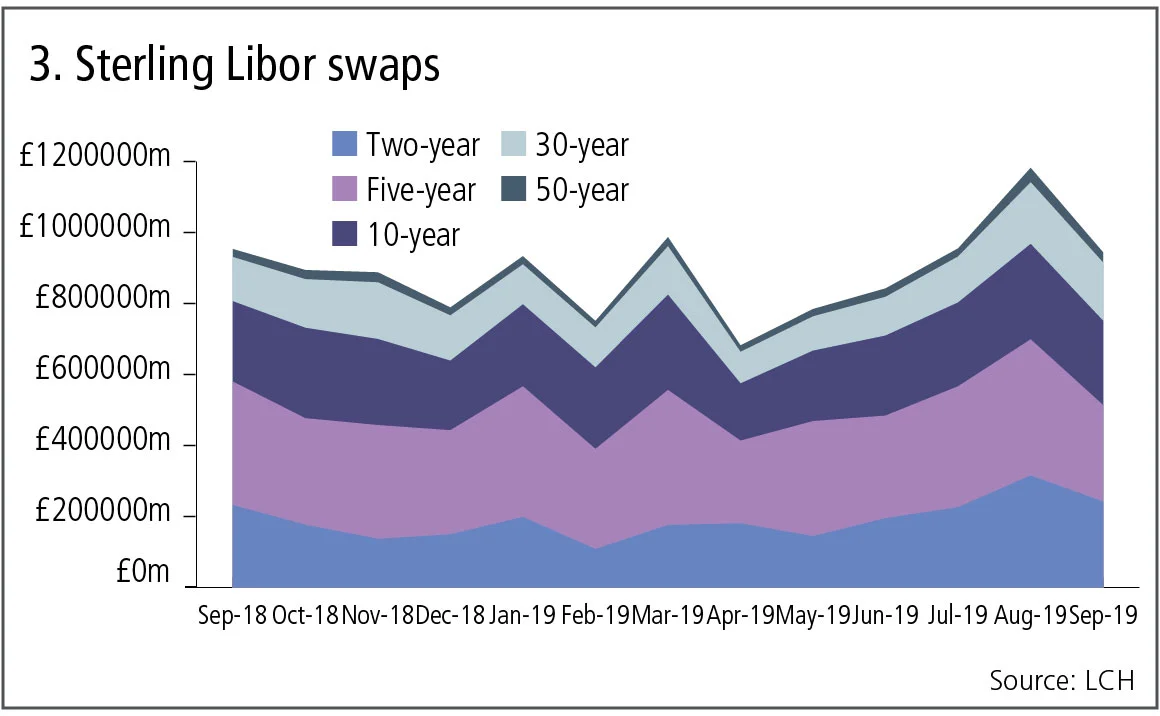

Sterling Libor and Sonia swaps

Let’s turn next to sterling, where the existing Sonia rate (after reform) has been selected as the RFR to replace Libor. The two questions we are most interested in are, first, is swaps volume in Sonia increasing and volume in Libor decreasing, and second, are longer tenors trading in Sonia.

Using data from LCH SwapClear, we can attempt to answer these.

Figure 3 & 4 show:

- Monthly gross notional cleared at LCH SwapClear over the past year, split out by the major tenor buckets for Libor and Sonia swaps.

- For Libor swaps we can see that volumes have continued to increase, with a high of £1.2 trillion cleared in August 2019 and September 2019 with £950 billion.

- In addition, there is no material change in the portion of Swaps trading in longer tenors.

- So nothing in the data here suggests firms are stopping or reducing their trading of Libor swaps with maturities beyond January 2022.

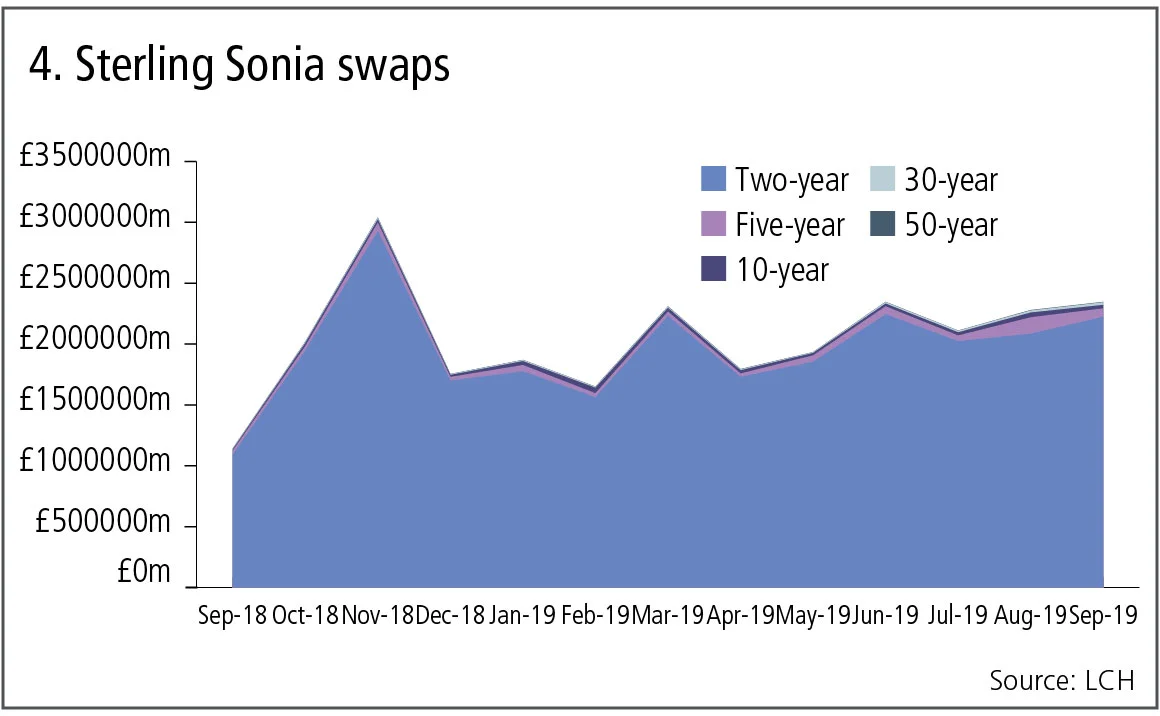

- For Sonia swaps, the monthly gross notional traded is much larger, at least double, with August 2019 showing £2.3 trillion, and there does seem to be a growth trend; however, volume is dominated by tenors below two years.

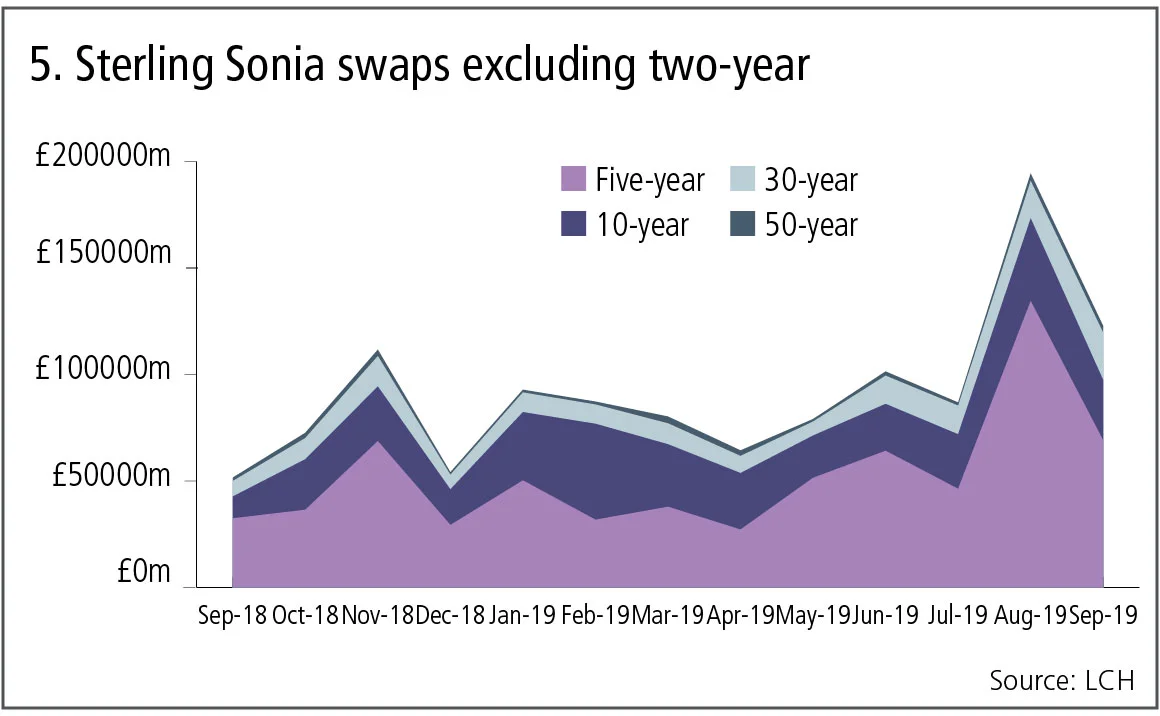

Let’s now chart Sonia swaps volume and exclude two-year and below tenors.

Figure 5 shows:

- A significant jump in August 2019 for the five-year tenor with £69 billion cleared and also for the 30-year with £28 billion cleared in September 2019.

So, encouraging signs at the longer end, but a long way to go to approach the Libor Swaps five-year volumes of £380 billion and 30-year of £184 billion in August 2019

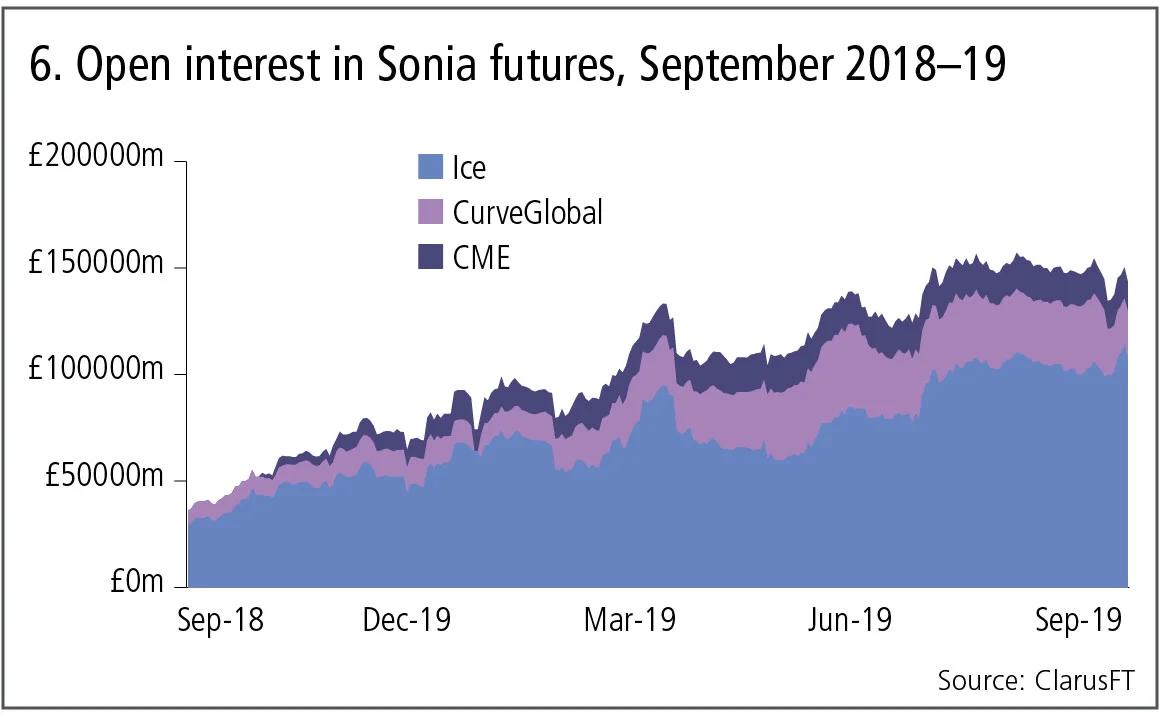

Sonia futures

Finally, Sonia futures, where we see a genuine competition between three exchanges – Ice, CME and CurveGlobal.

Figure 6 shows:

- Open interest growth in the past year, with a positive trend.

- Ice has the largest share – £107 billion open interest on September 27, 2019.

- CurveGlobal with £22 billion and CME with £14 billion.

- Aggregated for all three, there is £144 billion of open interest.

To put this into perspective, on September 27, 2019, Ice short sterling futures had £2 trillion of open interest, meaning Sonia futures now represent 7% of this figure. This is less than the 12.5% that SOFR futures represent compared to CME Eurodollar, so some way to go for Sonia futures.

As 2019 ends and we move into 2020, we expect to see much higher volumes in SOFR futures and SOFR swaps, with the upcoming Q3 move by clearing houses from Fed funds to SOFR discounting. While Sonia has no such trigger, as sterling swaps are already discounted with Sonia, continued exhortations from regulators should result in data showing higher Sonia and lower Libor volumes.

Amir Khwaja is chief executive of Clarus Financial Technology.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

なぜ価格が急騰する?

「長年にわたる調査を経ても、依然としてはっきりとは分かっていない」とジャン=フィリップ・ブショー氏は述べています

ギャップリスクは気にしないで:クレジット・リパックの規制上の取り扱い

シニア・クオンツのアンデレイ・チリキン氏は、リパッケージングにおけるギャップ・リスクは、バーゼルIIIの自己資本規制上の信用評価調整には該当しないと主張しています

オペリスク・データ:HSBC、外部による不正行為で4億ドルの損失を被る

また、中国における無許可取引への取り締まり強化、ソシエテ・ジェネラル銀行の保険不適切販売問題についても。データ提供:ORX News

ヴィニシウスの運命:ワールドカップの組み合わせ抽選における「運」の数値化

ジュリアン・ギヨン氏は、今夏の大会においてバイアス、分散、そして運がチームにどのような影響を与えるかを解説し、ポートフォリオ・マネージャーにとってのより広範な意義についても考察しています

G-Sibの資本サーチャージ:指数化と平均化がインセンティブに与える影響

資本リスク戦略担当者は、バーゼルIIIの最終局面が米国の大手銀行の行動に与える影響を予測しています

ポッドキャスト:アビ=ジャバー氏とリー氏が語る「スティッキー」なボラティリティ問題

二人は、VIX、SPX、SSRを同時に捉えるためのモデルについて議論しています

市場は未来を非常に歪んだ形で捉えている

ジャン=フィリップ・ブショー氏は、割引のパラダイムはより現実的なものへと適応すべきだと述べています

オペリスクデータ:サイバー攻撃が暗号資産プロトコルを揺るがす

他にも:JPモルガンが投資家の損失をめぐり罰金処分を受けた、Symetraのメソジスト系年金基金をめぐる混乱など。データ提供:ORX News