Swaps data: SOFR swaps slip, futures flip

After a banner month for the young OTC instrument in January, volumes then halved

With Libor rates on borrowed time, the adoption of new risk-free rates (RFRs) is being closely watched. Last month’s data revealed increased activity in derivatives linked to the secured overnight funding rate (SOFR), with both SOFR futures and swaps volume hitting new highs.

This month brings mixed tidings. On the one hand, open interest in SOFR futures traded at CME almost doubled. On the other, SOFR swaps volume is half what it was a month ago.

Meanwhile, RFRs for other major currencies, including sterling and the Australian dollar, are seeing more activity.

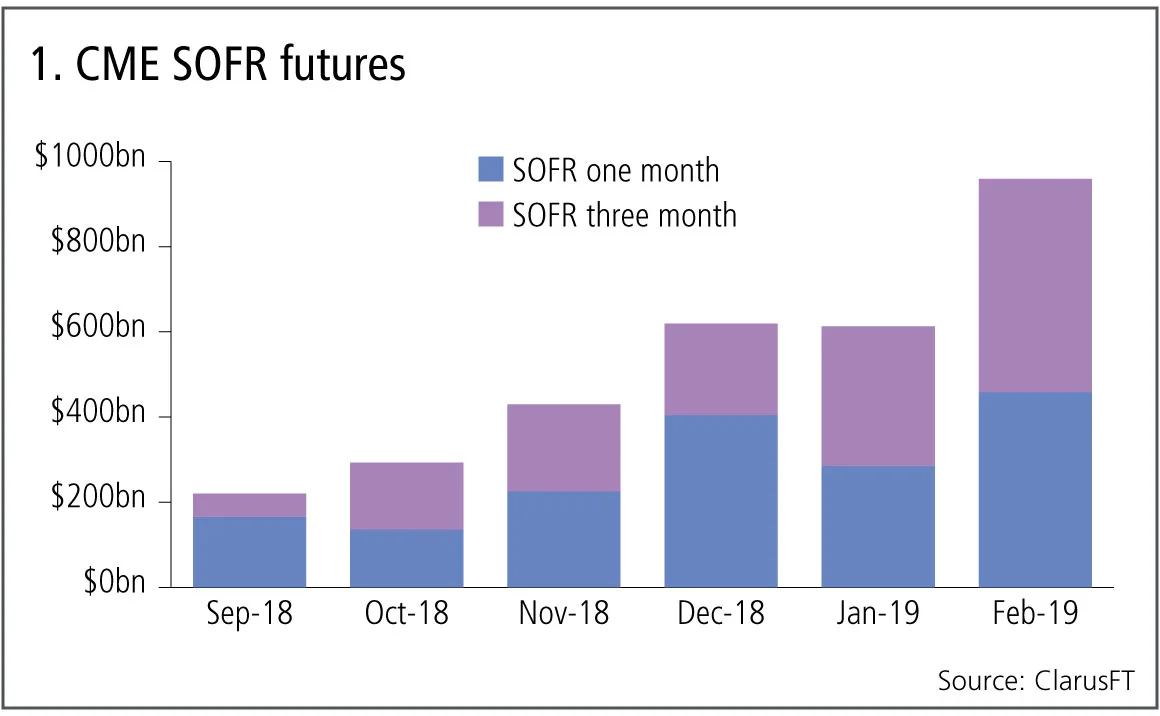

CME SOFR futures

February saw a big jump in volume and open interest.

Figure 1 shows:

- A record month, with volume touching $1 trillion, compared with $600 billion a month before.

- Both one-month and three-month contracts saw higher volumes.

- A clear trend of month-on-month increases.

Just as importantly, open interest almost doubled from $216 billion at the end of January to $400 billion at the end of February.

Futures volumes are coming along very well and it will be interesting to see if the trend holds over the course of this year.

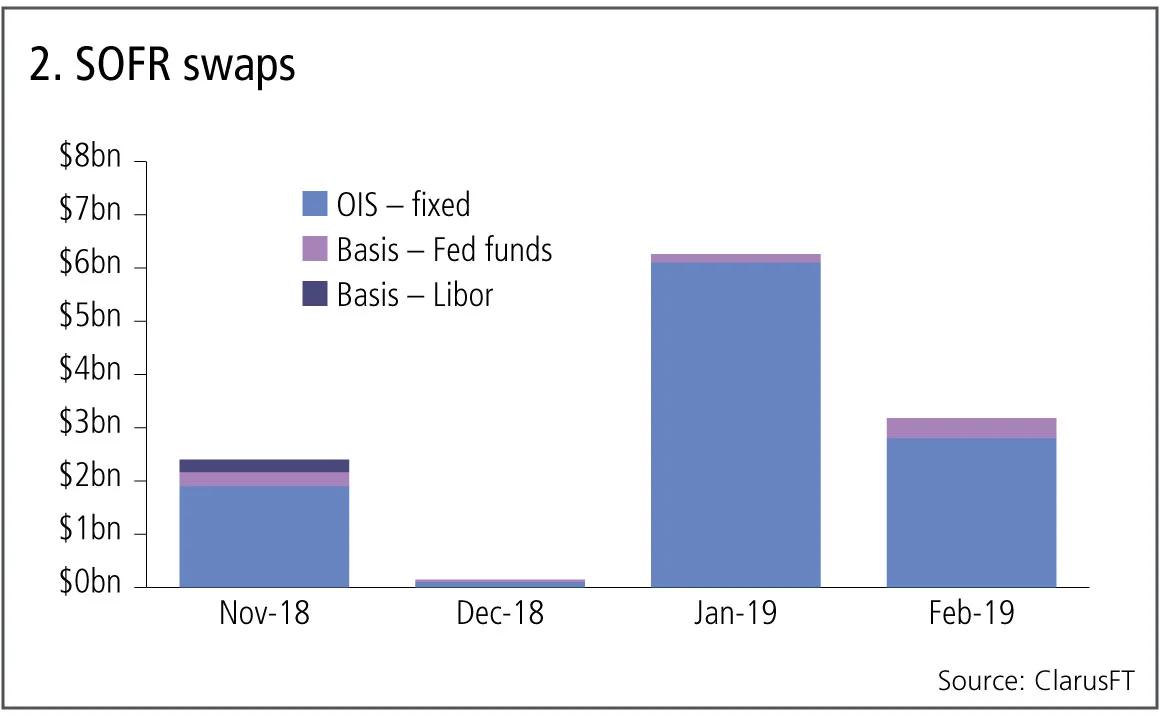

SOFR swaps

What about swap volumes? Using US trade repository data, we can isolate swaps that reference the SOFR index. In this case, the data is disappointing.

Figure 2 shows:

- Volumes are down, with only $3.2 billion gross notional.

- Only 24 trades were reported by US persons.

- Of these, 16 were SOFR versus fixed overnight indexed swaps, and six were SOFR versus Fed funds basis swaps.

SOFR swaps still have a long way to go. But it is early days for the Alternative Reference Rate Committee’s paced transition plan and, as 2019 progresses, we expect to see a sharp pick-up in volume.

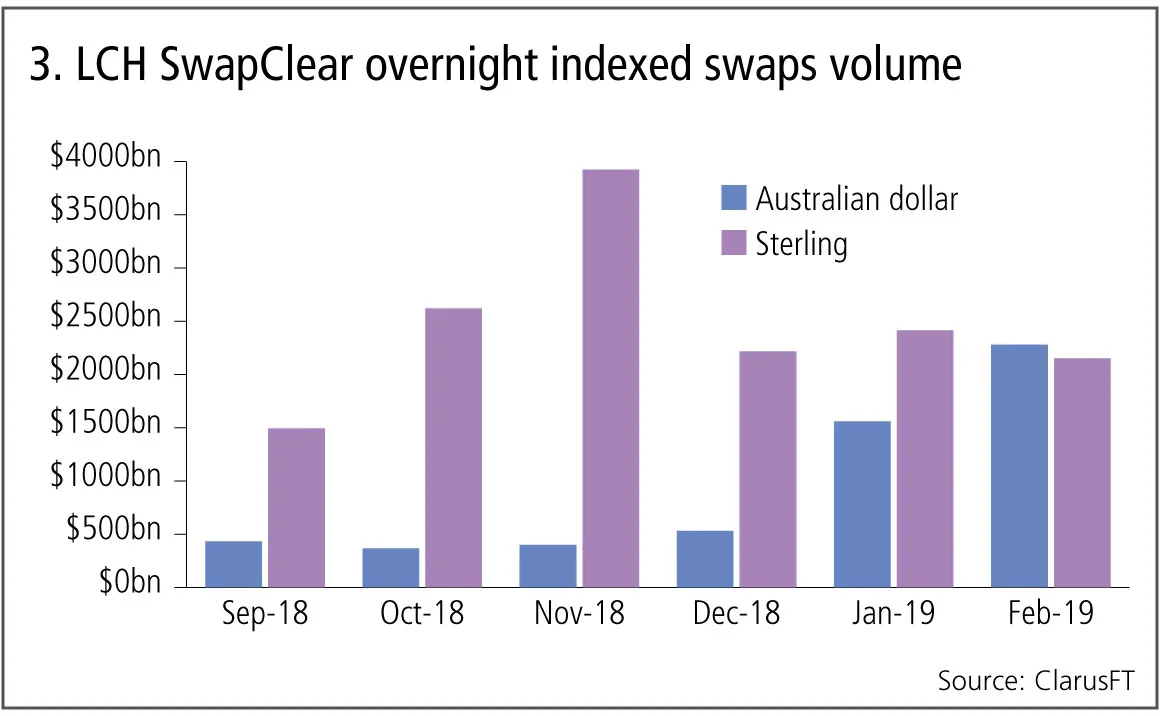

Aonia and Sonia swaps

For comparison, we can look at the RFR replacements for two major currencies: the sterling overnight interbank average (Sonia) and the Reserve Bank of Australia cash rate, also known as Aonia.

Figure 3 shows:

- The chart shows monthly volumes of Australian dollar and sterling OIS swaps at LCH SwapClear.

- For the first time, Australian dollar volume exceeded sterling, a result of recent uncertainty in the direction of the RBA cash rate.

- Sterling Sonia reached an all-time high of $3.9 trillion in single-sided gross notional in November 2018.

While Sonia is only cleared in material amounts at LCH SwapClear, Aonia also sees significant volume at ASX, which had record months in January and February, with A$250 billion and A$414 billion, respectively, of single-sided gross notional.

Aonia and Sonia are healthy markets. While sterling generally sees more gross notional trades in OIS than interest rate swaps, this was also true for Australian dollars in the months of January and February.

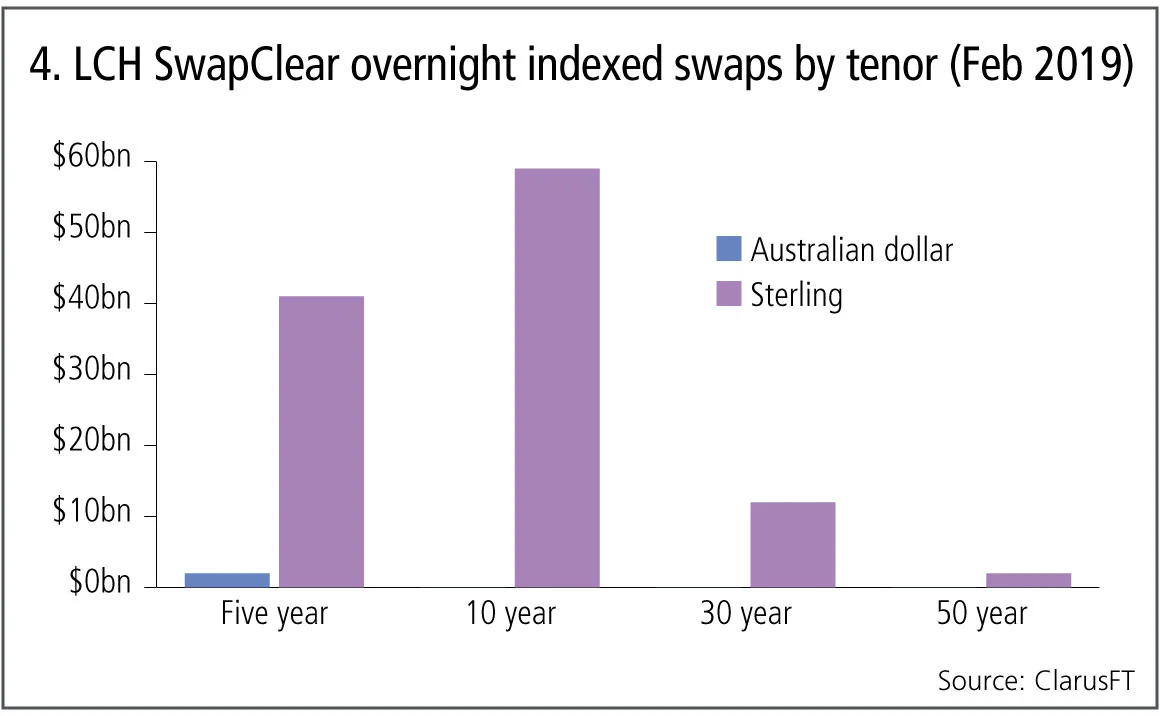

Now, let’s look at the maturities that are traded.

Figure 4 shows:

- This chart excludes tenors below two years, which have the bulk of the volume and would dwarf the remaining tenors if included.

- For the Australian dollar, there is just $2 billion in the two- to five-year bucket, and nothing in longer tenors.

- Sterling has $41 billion single-sided gross notional in the five-year, $59 billion in the 10-year, $12 billion in the 30-year and $2 billion in the 50-year.

Little to no trading happens in Aonia above two years. Sterling has some volume in each of the five-, 10- and 30-year tenors, but there is a long way to go compared with the $2 trillion in volume below two years.

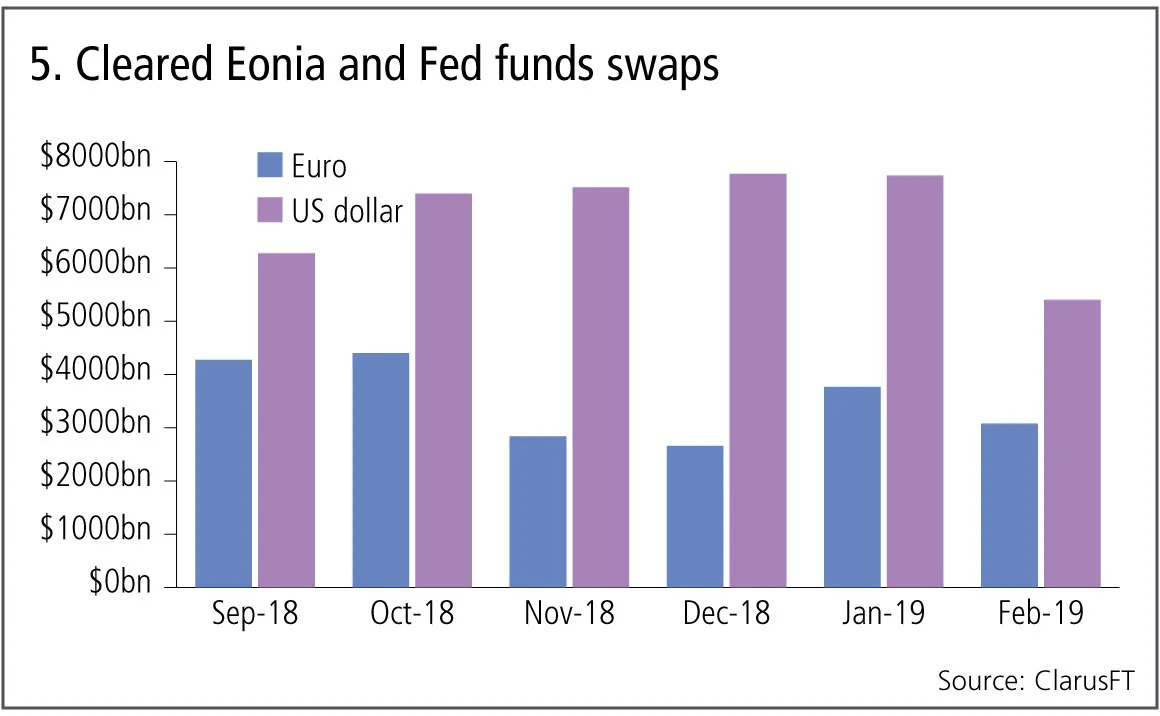

Eonia and Fed funds swaps

Finally, there are two extremely well-traded overnight index swap rates that have not been chosen as replacement RFRs for their respective currencies: Eonia and Fed funds.

Figure 5 shows:

- The chart shows cumulative volume at LCH, CME and Eurex by -currency for each month.

- Fed fund swaps gross notional hit $7.7 trillion in December and -January, but fell sharply in February to $5.4 trillion.

- Eonia gross notional stood at $3.8 trillion in January and $3.1 trillion in February.

This shows how far SOFR has to go. It will take some time to get from the current $3 billion a month to anything approaching the $7 trillion traded in Fed funds. The euro short-term rate (Ester), which is yet to be published, has an even bigger mountain to climb. It will be interesting to see how long it takes for these new RFRs to surpass existing overnight index swaps and Libor swaps.

Amir Khwaja is chief executive of Clarus Financial Technology.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

オペリスク・データ:企業スパイがBBVAに脅威をもたらす

他にも:BofAがエプスタイン氏との関与疑惑で追及されています。また、少数株主がブルックフィールドに異議を唱えています。データ提供:ORX News

AI政治の台頭

MASの顧問であるデビッド・ハードーン氏は、AIを単なる一つの技術として扱うべきではないと述べています

AIリスク管理と能力制御への移行

リスク管理者によると、検証の枠組みを見直すことで、銀行はイノベーションと規制上の要件を両立させ、強固なリスク管理体制を維持することができます

トークン化された商品市場は、経済の円滑な運営に寄与する可能性がある

暗号資産の専門家は、実物資産をブロックチェーンに移行することで、担保に関する摩擦が緩和されると主張しています

GenAIの時代において、未だに優れたモデルが必要なのはなぜなのか?

ジャン=フィリップ・ブショー氏は、モデルが人工知能をレジームシフトの過程で導き、過学習から遠ざけることができると述べています

取引のスピードがガバナンスを上回る時:一瞬の統制の隙間

デリバティブの専門家によると、光駆動型エレクトロニクスの新たな形態が、市場インフラにおける次のリスクとなる可能性があるとのことです

先物とオプションが示す戦争のコスト

現物価格は大きな混乱を示していますが、先物市場はこれが一時的なものだと示唆しており、オプション市場は不安定な状況が続くと示唆しています

担保に関して、TINAはTIAになることができるのか

あるエコノミストは、レポ取引やデリバティブ取引における担保としての米国債の優位性は、もはや揺るぎないものではないと指摘しています