Risk magazine - May 2018

In this issue: how a $5.4 billion deal could change the Treasury landscape; a clearing house basis for non-cleared derivatives; single-dealer platforms boosted by Mifid; some strange goings-on with APAs; and much more

Articles in this issue

Rolet is right – for now

CME/Nex deal could change the established logic on how to deliver rates market savings

Funding changes break cross-currency, Libor/OIS link

Tax reform and Treasury issuance focuses bank US dollar funding pressures onshore

Isins for swaps need ‘complete rethink’, say platforms

Three trading venues say Mifid II transparency objectives diminished by identifier choice

Libor death threatens to blow hole in hedges

Isda AGM: BlackRock, Fed stress need for fallbacks to marry up across rates universe

US will implement FRTB, insists Fed official

Isda AGM: “I don’t know why people doubt” US adoption, says Lynch

LCH and CME to start clearing SOFR swaps in third quarter

Scramble to offer clearing aimed at cutting clients’ margin and capital costs

US swap rate failed during volatility rout

The Ice swap rate was not published on February 6 due to a lack of electronic prices during equity turmoil

LCH-JSCC basis drops as hedge funds arrive

Capula and Rokos Capital among funds to have gained access to JSCC in recent months

Regional banks cheer tweaks to FRTB standardised approach

Planned softening of SBA makes it more appealing, but most banks still expect to adopt IMA

People moves: SG loses Mattatia, Deutsche’s Wisnia joins Eisler Capital, and more

Latest job changes across the industry

CME has chance to rule US rates after Nex deal

Market expects exchange to unite bond, repo, futures and swaps clearing – eroding grip of banks and DTCC

Vol virus: how a CCP basis leapt from swaps to swaptions

A clearing house basis has opened up between JSCC and LCH on yen swaptions – despite neither clearing the product

Single-dealer platforms win in Mifid forex shake-up

Best execution rules not driving liquidity away from sole dealer platforms as expected

Safeguarding liquidity in a changing environment

Nick Gant, head of fixed income prime brokerage for Europe, the Middle East, Africa and Asia-Pacific at Societe Generale Prime Services, discusses banks’ evolving responsibilities for providing liquidity in a post-financial crisis environment in which…

Europe struggles to get a grip on derivatives transparency

Mifid reporting has fallen short of US swaps data, but national regulators are partly to blame

Mifid data: hard to access, hard to use

Risk.net research shows four of 12 APAs and trading venues only provide information via other vendors

Fed risk rating system unifies stress testing and 3LOD

Some banks have qualms over potential downgrades and overlap between first and second lines

On the offensive – Seeking a new edge, buy-side invests in portfolio and risk analytics

A fast-moving, headstrong hedge fund – hit by rare losses after a black swan event touched on an overweight country exposure – ponders adding fresh quantitative expertise. Much to traders’ chagrin, the chief investment officer and chief operating officer…

Op risk capital: why US should adopt SMA today

No reason to delay roll-out of standardised approach, says TCH’s Greg Baer

Maybank takes to the dark web to tackle hackers

Bank’s CRO and CTO discuss front-foot approach to cyber threats

Power to the people: US bourse bets on retail rush into swaps

Eris Exchange hopes retail access to its swap futures will usher in new era of swaps for all

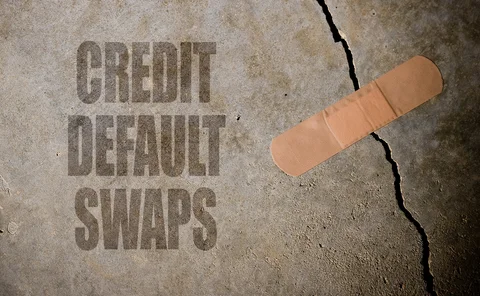

Fixing CDSs: lots of patches, no magic wand

Isda response to Hovnanian controversy could open new loopholes, traders warn

Going local: Brexit prompts rethink on MREL governing law

One EU regulator has already asked banks to avoid reliance on English law for bail-in

FRTB threatens dynamic forex hedging of capital ratios

Industry says recent Basel proposals are unclear and retain burden of pre-approval for hedges

Bridge to nowhere: gaps in Treasury G-Sib bankruptcy plan

US bankruptcy-first approach needs more thought on emergency liquidity, say experts

The long march: ECB struggles with supervisory convergence

Anti-money laundering supervision and emergency liquidity assistance still run at national level

Fears persist about forced unwind from ‘implicit’ short vol funds

February sell-off could presage a bigger slide if correlations change, buy-siders say

Start-up fund looks to profit from early-stage bubbles

Market feedback loops have a signature that can be spotted and monetised, new fund SIMAG says

Don’t wait for freight: suppliers look to boost demand

Growing interest in shipping derivatives means FFA market needs to change

Simple models won’t cut it for systemic risk

Understanding interconnectedness and capturing it within models is a key challenge, say quants

Credit Suisse sheds $11bn in op risk RWAs

Regulator allowed Swiss bank to cut op risk exposure from defunct business

Goldman Sachs’ VAR at three-year high

Increased client activity and market volatility increases firmwide risk

JP Morgan criticises revised leverage ratio

"Time is right" to reconsider G-Sib capital framework, says CFO

Monthly op risk losses: banks count the cost of IT failures

Also: top five loss breakdown led by Wells Fargo’s $1bn fine. Data by ORX News

Credit data: firms with fewer well-paid women are riskier

Gender pay gap disclosures could be a proxy for credit risk, writes David Carruthers of Credit Benchmark

Swaps data: the allure of liquidity

Liquidity in OTC trading concentrates at one venue, or splits across three, writes Amir Khwaja of Clarus FT

Putting swaptions pricing in the fast lane

Derivatives consultant proposes a model for arbitrage-free pricing

Discrete time stochastic volatility

Quant proposes faster model to price arbitrage-free swaptions

Isda chair on the swaps market’s power shift

A decade ago, dealers held 18 of 19 board seats – but crisis has forced trade body to change