Swaps data: cleared vs non-cleared margin

Growing margin burden for non-cleared swaps means cleared margin is likely to grow further, argues Amir Khwaja

Initial margin numbers are growing for the over-the-counter derivatives market – a result of rules that require some products to be centrally cleared, as well as separate requirements compelling a growing band of firms to collect margin for non-cleared trades.

But the two regulatory edifices function in different ways and also interact, it is likely that, as the non-cleared rules steadily expand, they will encourage more firms to clear voluntarily and create incentives for the scope of cleared products to be widened as well.

Currently, the non-cleared margining regime requires approximately 50 financial groups to collect and post initial margin for OTC derivatives they trade bilaterally. The first phase of 20 firms started doing so on September 1, 2016 and only for new trades executed subsequent to that date, so it will have taken some time to build up to the $50 million exposure threshold above which initial margin must be collected and posted.

The remaining phases in September 2019 and September 2020, cover phase four and phase five firms with – respectively – greater than $750 billion and $8 billion of gross notional in non-cleared derivatives. The influx of new firms has been estimated at 1,100 in a recent document by the International Swaps and Derivatives Association, the Securities Industry and Financial Markets Association and other trade associations.

Given the size of the numbers involved, let’s look at the data on initial margin.

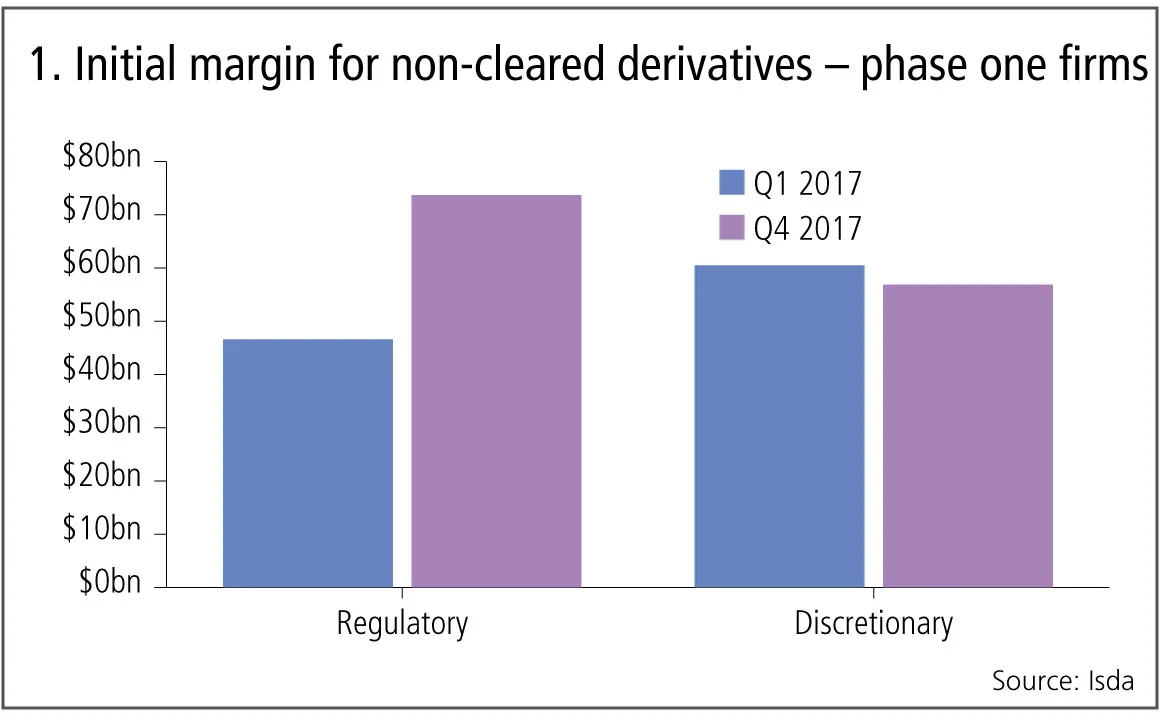

Initial margin for non-cleared derivatives

Isda’s most recent annual margin survey was published in April this year, covering 2017. It provides interesting insights as it has data provided by the 20 largest market participants (phase one firms).

Figure 1 shows:

- Regulatory initial margin increasing from $46.6 billion at the end of Q1 2017 to $73.7 billion at the end of Q4 2017, an increase of 58%.

- Isda attributes the large increase to the fact that each month more and more new trades are executed and so fall under the initial margin rules.

- In addition a smaller number of phase two firms started complying with the rules on September 1, 2017.

- Discretionary initial margin decreased to $56.9 billion from $60.5 billion, a drop of 6%.

- Isda attributes this decrease to more firms falling into regulatory initial margin, so more and more of this will move into the regulatory bucket.

A cumulative $131 billion of initial margin as at end Q4 2017 sounds like a large amount indeed, let’s see how this compared to cleared OTC derivatives.

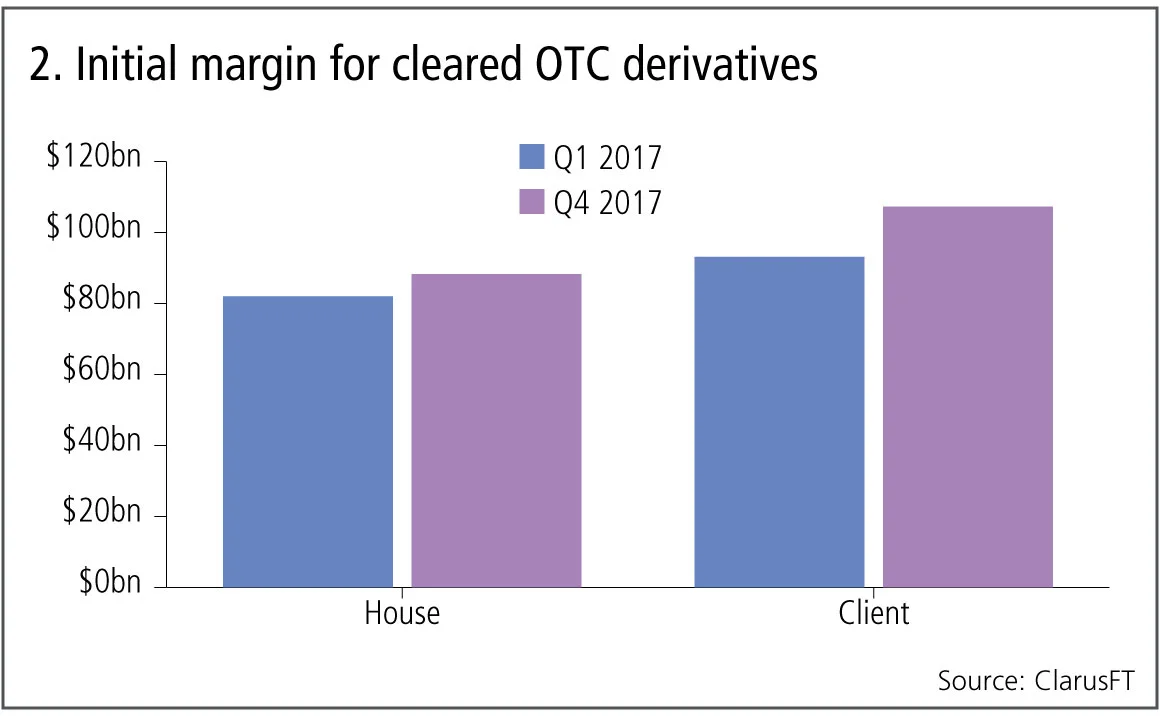

Initial margin for cleared OTC derivatives

Disclosures required of central counterparties (CCPs) by the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions cover initial margin totals. Using the data we can aggregate seven of the largest OTC derivative clearing services: CME IRS, Eurex OTC IRS, Ice Credit Clear, Ice EU CDS, JSCC IRS, LCH ForexClear and LCH SwapClear.

Figure 2 shows:

- House (or member) initial margin increasing from $82 billion to $88.3 billion over the same period, an increase of 8%.

- Client initial margin increasing from $93 billion to $107 billion from Q1 2017 to Q4 2017, an increase of 15%.

- A cumulative total of $196 billion of initial margin at end Q4 2017, so significantly larger than the $131 billion of cumulative uncleared initial margin in the prior section.

- It is also interesting to note the ratio of house to client initial margin is 45% to 55%, so while house margin contains the largest market participants – which are also the phase one, two and three firms in the non-cleared regime – the fact that client initial margin is larger is a reflection of the fact that these portfolios are more directional and so attract larger initial margin.

Now, in comparing cleared initial margin and uncleared initial margin, we have to be cognisant of the differences; in particular, in how netting operates.

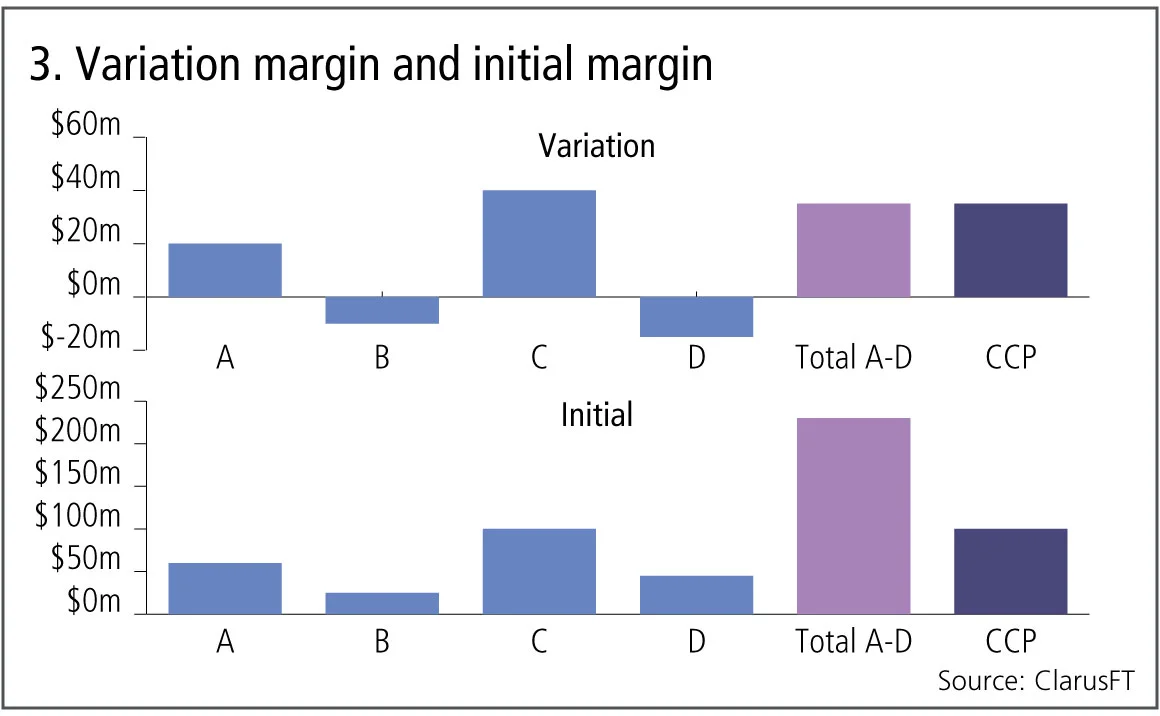

Multilateral netting

One of the most important benefits of central clearing is multilateral netting, meaning all my exposures can be netted down to one margin number, as opposed to individual bilateral margins against each counterpart. While this is of great benefit for variation margin, it is even more important for initial margin as the following figure illustrates.

Figure 3 shows:

- Variation margin that needs to be paid or received on a given day to each of four counterparties; A to D, the total of these is $35 million.

- If these same position were all cleared at one CCP, the net variation margin payment would also be $35 million, so economically exactly the same.

- However for IM, the situation is very different, as the sum of the four bilateral IM amounts is $230 million, while if one CCP cleared all of these, the IM could be $100 million, so economically the market is much better off.

In reality, market participants cannot net all cleared OTC derivatives into one CCP, so does the illustrated multilateral example still hold?

The answer is yes, as while a market participant may use a handful of CCPs for OTC derivatives, generally less than 10, the same participant is likely to have bilateral derivatives exposures against a much larger number of counterparties, generally in the low hundreds.

Consequently, the grossing up of initial margin in each of those relationships as more and more firms are captured by uncleared margin rules is likely to increase regulatory initial margin more and more.

The $50 million threshold below which initial margin only needs to be calculated and not collected and posted helps mitigate matters, however we still expect to see uncleared margin rules act as an incentive for firms to clear.

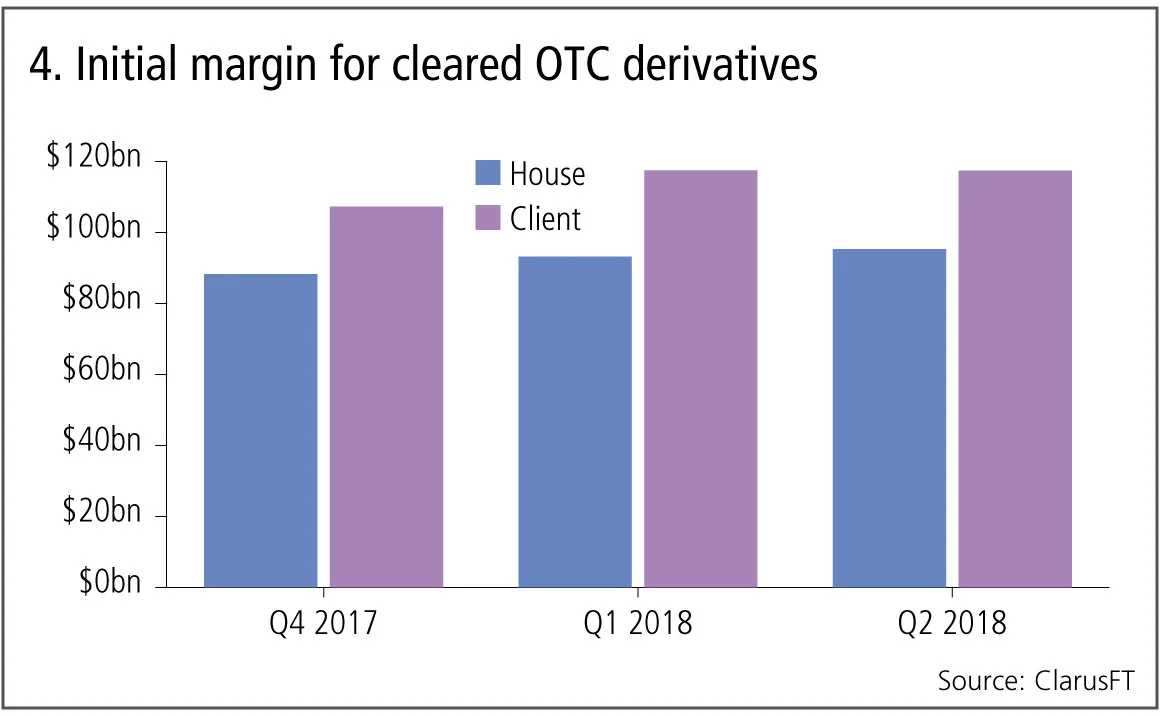

Increasing clearing

This incentive to clear, as well as mandatory clearing of certain products should mean cleared initial margin for OTC derivatives will continue growing for some years yet.

Let’s see if more recent data bears that out.

Figure 4 shows:

- House initial margin increasing from $88.3 billion at Q4 2017 to $95.3 billion at Q2 2018.

- Client initial margin increasing from $107 billion to $117 billion.

- A total of $213 billion initial margin at Q2 2018, up 9% over the six-month period, which projecting at the same rate implies 18% annual growth rates.

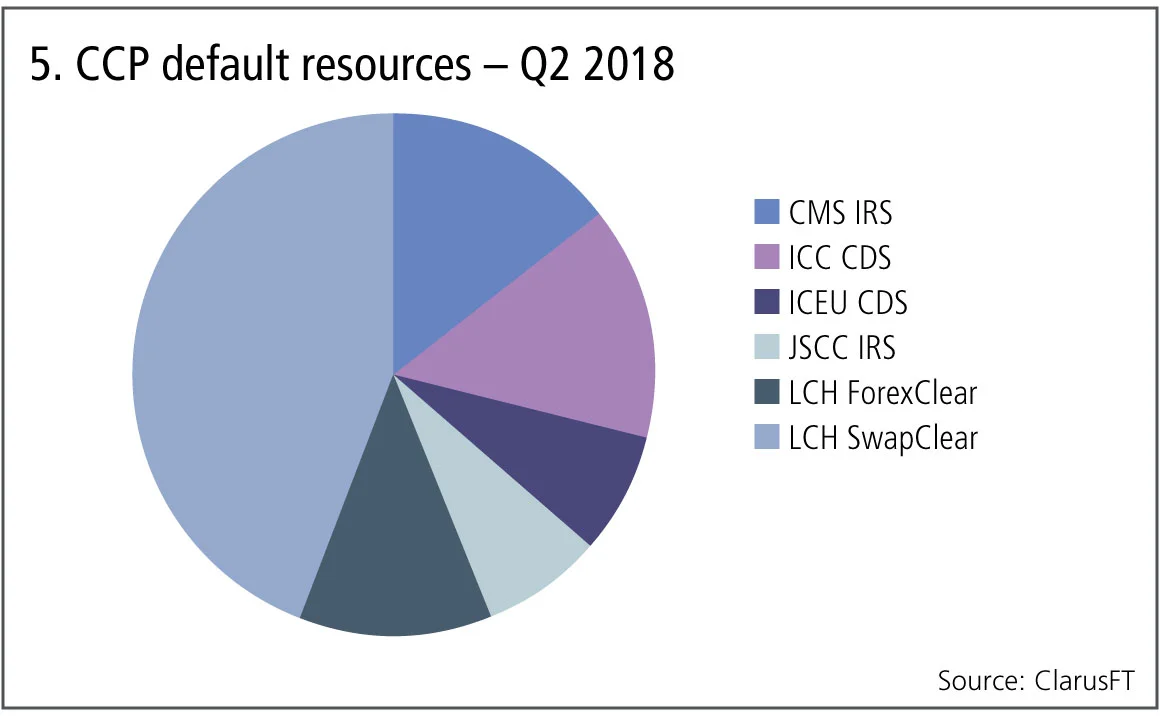

Default resources

Before I end, it is worth mentioning CCPs also require their members to contribute to a defult fund. Below, we aggregate default resources for the same OTC CCPs, excluding Eurex, which has a combined default fund.

Figure 5 shows:

- Composition of the pre-funded and committed financial resources available to each of the CCPs.

- A cumulative $16 billion of prefunded resources and a further $14 billion of resources that are committed on default of a member, a grand total of $30 billion.

This additional $30 billion provides additional security and a backstop to member defaults, above and beyond the $213 billion of initial margin held for cleared OTC derivatives.

Amir Khwaja is chief executive of Clarus Financial Technology.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

AIエージェントがリスク管理者の課題解決にどう役立つ

シティのリスク専門家は、取引や融資承認に関する構造化データと非構造化データを統合し、リスクに関する単一かつ統一されたビューを構築する自律型AIツールについて概説しました

オペリスク・データ:企業スパイがBBVAに脅威をもたらす

他にも:BofAがエプスタイン氏との関与疑惑で追及されています。また、少数株主がブルックフィールドに異議を唱えています。データ提供:ORX News

AI政治の台頭

MASの顧問であるデビッド・ハードーン氏は、AIを単なる一つの技術として扱うべきではないと述べています

AIリスク管理と能力制御への移行

リスク管理者によると、検証の枠組みを見直すことで、銀行はイノベーションと規制上の要件を両立させ、強固なリスク管理体制を維持することができます

トークン化された商品市場は、経済の円滑な運営に寄与する可能性がある

暗号資産の専門家は、実物資産をブロックチェーンに移行することで、担保に関する摩擦が緩和されると主張しています

GenAIの時代において、未だに優れたモデルが必要なのはなぜなのか?

ジャン=フィリップ・ブショー氏は、モデルが人工知能をレジームシフトの過程で導き、過学習から遠ざけることができると述べています

取引のスピードがガバナンスを上回る時:一瞬の統制の隙間

デリバティブの専門家によると、光駆動型エレクトロニクスの新たな形態が、市場インフラにおける次のリスクとなる可能性があるとのことです

先物とオプションが示す戦争のコスト

現物価格は大きな混乱を示していますが、先物市場はこれが一時的なものだと示唆しており、オプション市場は不安定な状況が続くと示唆しています