Swaps data: breaking down CCPs’ $750 billion funding bill

Amir Khwaja of Clarus FT considers how initial margin, variation margin and default fund contributions can quickly add up

Initial margin, variation margin and default resources are three key weapons used by central counterparties (CCPs) to protect against risk. Under the voluntary Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions public quantitative disclosures, over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more are published each quarter.

The most recent available data is for the quarter ending September 30, 2017, and shows some interesting insights. For instance, across the three metrics, the total funding requirement for all CCPs could be as high as $750 billion. Variation margin calls could be as much as 2.5 times the average, while over half of initial margin is posted as government bonds.

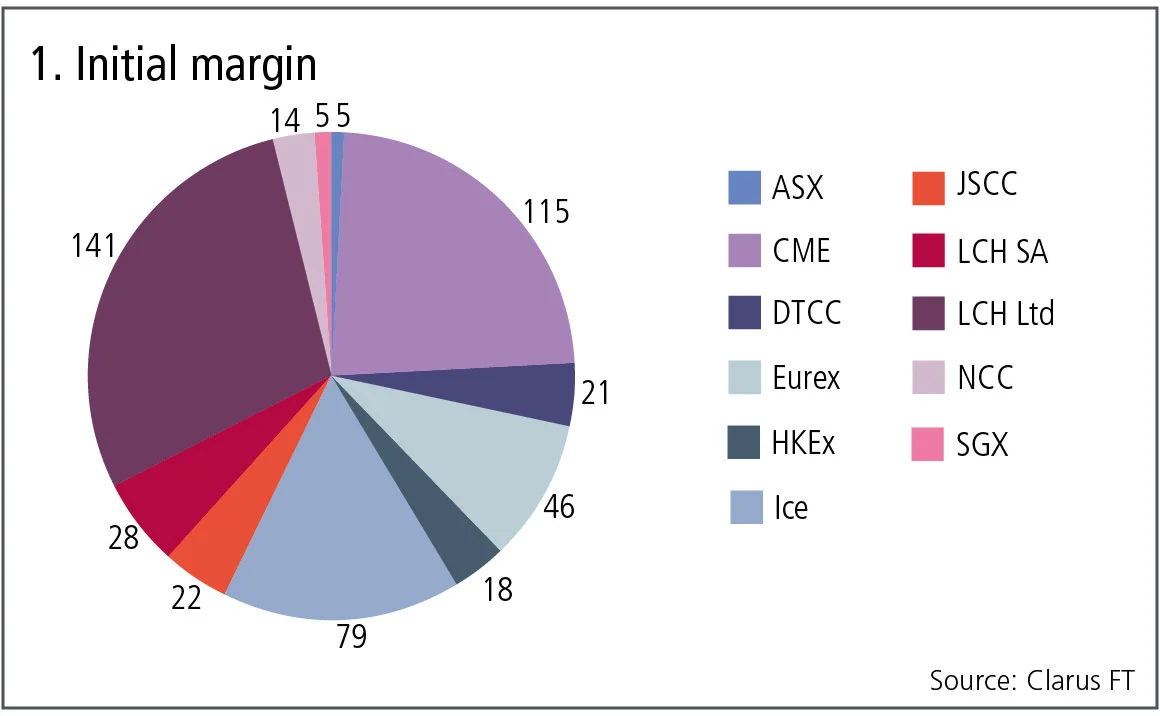

Initial margin required

Initial margin required from participant members is a good measure of the size of risk managed by a CCP and, aggregating this information for a wide selection of major clearing houses, we get a grand total of $500 billion.

Figure 1 is the breakdown for a clearing house, with the constituent CCPs aggregated in billions of dollars.

Figure 1 shows:

- LCH Ltd with $141 billion of initial margin is the largest, of which SwapClear contributes $121 billion.

- CME is next with $115 billion.

- Ice has $79 billion, aggregating Ice Clear Credit, US futures and options, Ice Clear Europe Credit and its futures and options – no data is available for other Ice-owned CCPs.

- Eurex with $46 billion.

- LCH SA with $28 billion and the Japan Securities Clearing Corporation with $22 billion.

- The Depository Trust & Clearing Corporation with $21 billion, of which the government securities division contributes $11.7 billion.

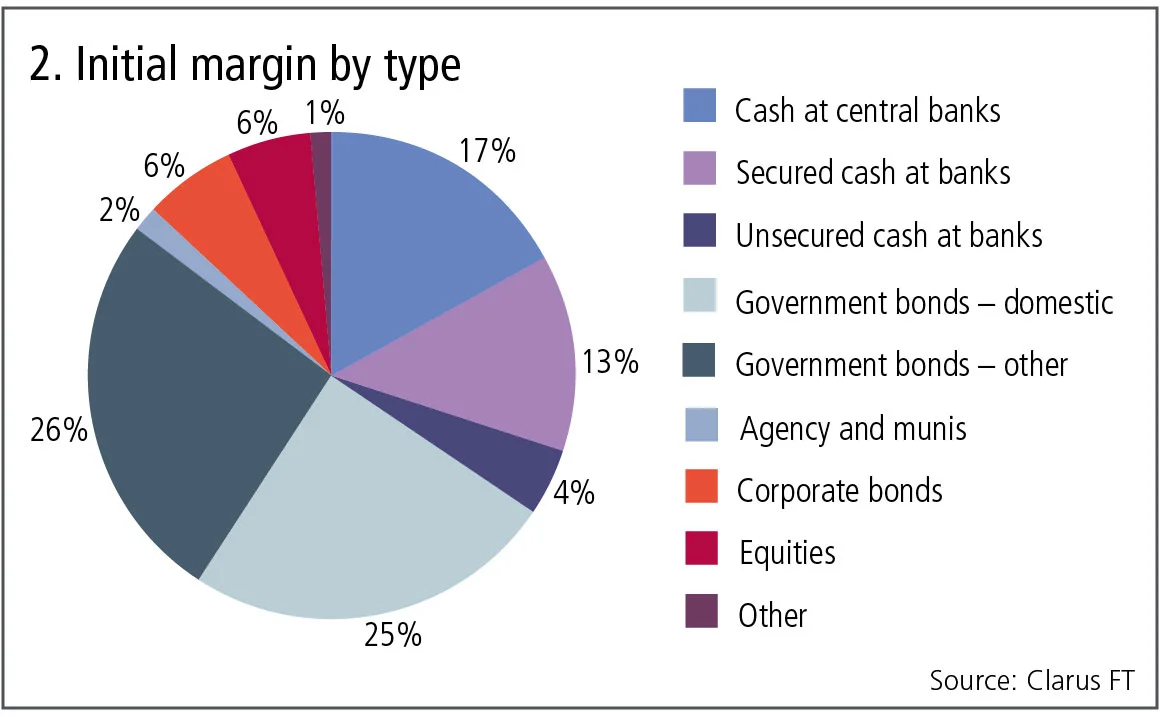

Initial margin type

A grand total of $500 billion of initial margin is required, which is a large sum indeed. Remember, this is the amount that members are required to post at the CCP, so it is real money and not a notional number.

Let’s look at data on how these clearing houses hold initial margin funds.

Figure 2 shows:

Government bonds are by far the largest at 51%, made up of almost equal amounts of domestic – meaning the sovereign of the CCP’s location – and other, meaning foreign country sovereigns.

- Cash at central banks is the next largest at 17%.

- Secured cash at commercial banks is 13% and includes reverse repo transactions.

- Corporate bonds and equities are 6% each.

- Unsecured cash at commercial banks is 4%.

Clearing houses will impose larger haircuts on riskier securities, and these figures use pre-haircut amounts, there is additional data on the post-haircut amounts of these types, but this does not materially alter the above percentages.

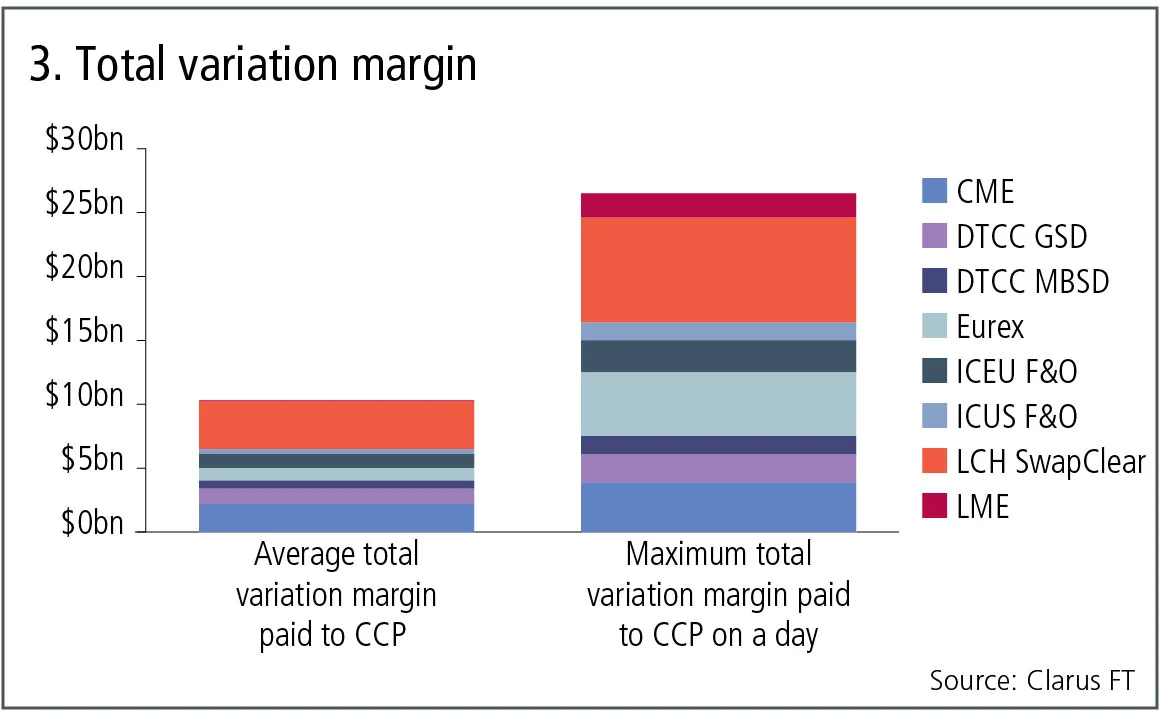

Total variation margin

CCPs also collect and post daily variation margin to participant members to reflect the daily profit and loss of their positions. Let’s look at the size of these flows.

Figure 3 shows:

- Average total variation margin paid to a CCP and the maximum total variation margin paid to a CCP on a day in the quarter ending September 30, 2017, for selected CCPs with large variation flows.

- The grand total for these eight CCPs is $10 billion, meaning on average this amount is being collected by CCPs from members and the same amount posted to other members.

- LCH SwapClear at $3.7 billion and CME at $2.2 billion are the largest two contributors.

- The total of maximum total variation in a day in the quarter is $26 billion, so two and a half times as large as the average.

- LCH SwapClear at $8.2 billion and Eurex at $5 billion are the largest two contributors.

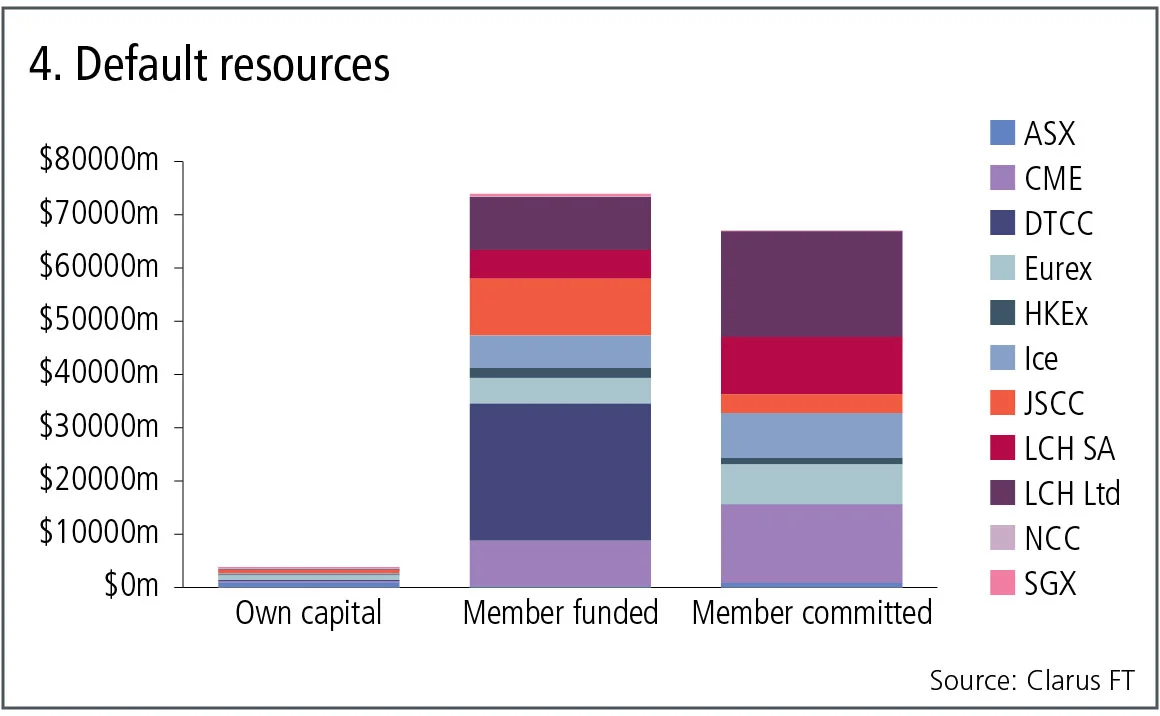

Default resources

Besides initial margin and variation margin, the other important measure of a CCP’s significance is the default fund or guarantee fund. These are the resources that will be called into action should a defaulting member’s variation margin, initial margin and pre-funded default fund contribution not be sufficient to close out their positions. As such it provides the backstop that gives a high level of confidence to the safety and risk management provided by a CCP.

Let’s look at these default resources for the same clearing houses that we aggregated initial margin by their constituent CCPs.

Figure 4 shows:

- Three columns: the clearing houses’ own capital; member-funded contributions, so already held by the CCP; and member-committed contributions that would be available in the event of a default, should they be needed.

- Clearing houses’ own capital of $3.8 billion is the smallest of these figures and there has been much comment over recent years on “skin in the game” and whether CCPs should be required to have more of their own capital. However, there has been no movement by the regulators who authorise, monitor and stress test CCP models and resources, which by implication means they are satisfied by the amount of this capital.

- Member-funded contributions are very significant at $74 billion – this is cash or securities provided by members to CCPs.

- DTCC has the largest amount of member-funded contributions at $26 billion, followed by LCH Ltd at $10 billion.

- Member-committed contributions are next at $67 billion.

- LCH Ltd has the largest share at $20 billion, followed by CME at $15 billion.

Initial margin, variation margin, default resources

In the preceding section we have looked at the three key numbers, initial margin, variation margin and default resources and shown that for selected major CCPs, these amount to:

- $500 billion of initial margin.

- $10–26 billion of variation margin.

- $78–145 billion of default resources.

- A grand total of $670 billion.

A big number, but one that is likely to be higher if more CCPs are included, for example B3 in Brazil or Shanghai Clearing in China, perhaps by $30 billion to $80 billion.

Irrespective of whether the number is $670 billion or $750 billion, the size of these numbers shows the systemic importance of CCPs as a major part of financial market infrastructure.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

オペリスク・データ:企業スパイがBBVAに脅威をもたらす

他にも:BofAがエプスタイン氏との関与疑惑で追及されています。また、少数株主がブルックフィールドに異議を唱えています。データ提供:ORX News

AI政治の台頭

MASの顧問であるデビッド・ハードーン氏は、AIを単なる一つの技術として扱うべきではないと述べています

AIリスク管理と能力制御への移行

リスク管理者によると、検証の枠組みを見直すことで、銀行はイノベーションと規制上の要件を両立させ、強固なリスク管理体制を維持することができます

トークン化された商品市場は、経済の円滑な運営に寄与する可能性がある

暗号資産の専門家は、実物資産をブロックチェーンに移行することで、担保に関する摩擦が緩和されると主張しています

GenAIの時代において、未だに優れたモデルが必要なのはなぜなのか?

ジャン=フィリップ・ブショー氏は、モデルが人工知能をレジームシフトの過程で導き、過学習から遠ざけることができると述べています

取引のスピードがガバナンスを上回る時:一瞬の統制の隙間

デリバティブの専門家によると、光駆動型エレクトロニクスの新たな形態が、市場インフラにおける次のリスクとなる可能性があるとのことです

先物とオプションが示す戦争のコスト

現物価格は大きな混乱を示していますが、先物市場はこれが一時的なものだと示唆しており、オプション市場は不安定な状況が続くと示唆しています

担保に関して、TINAはTIAになることができるのか

あるエコノミストは、レポ取引やデリバティブ取引における担保としての米国債の優位性は、もはや揺るぎないものではないと指摘しています