Technical paper/Hedging

On optimizing risk exposures with trend-following strategies in currency overlay portfolios

This paper proposes using an optimization mechanism in the currency overlay portfolio construction process.

Simulating meaningful uncertainty for complex energy portfolios

The meaningful uncertainty simulation framework can enable energy firms to make better decisions

Risk management and portfolio optimization for gas- and coal-fired power plants in Germany: a multivariate GARCH approach

This paper investigates the hedging effectiveness of energy derivatives traded at the EEX for the purpose of mitigating the risk exposure of gas- and coal-fired power plants in Germany.

Stochastic receding horizon control for short-term risk management in foreign exchange

The authors of this paper formalize a methodology to manage short-term FX risk.

How to get maximum value from power plant hedging

Dynamic hedging is becoming more common among plant operators

Liability-side pricing of swaps

Wujiang Lou presents a framework to compute recursive CVA and FVA via Monte Carlo simulation

CVA with Greeks and AAD

Reghai, Kettani and Messaoud present new technique to calculate CVA using adjoints

Numerical methods for the quadratic hedging problem in Markov models with jumps

In this paper algorithms are developed using the Hamilton–Jacobi–Bellman approach for parabolic partial integrodifferential equations related to the quadratic hedging strategy in incomplete markets.

Internal transfer price optimisation for integrated energy firms

A framework that demonstrates optimal internal pricing will deviate from ‘arm’s length principle'

Cutting Edge: Co-simulation of risk factors in power markets

A simple but realistic model to co-simulate the time series of temperature, electricity load and prices is proposed

Quant ideas: Building a better LNG forward curve

An overview of effective methods for constructing long-term LNG forward price curves

Pricing and hedging variance swaps on a swap rate

A pricing tool for fixed-income volatility products is introduced

Hedging iTraxx credit default swap index trading on an intraday basis: an empirical study

In this paper we examine the effectiveness of intraday hedging models for credit default swap index trading by means of more liquidly traded exchange-based futures contracts.

Regulatory costs break risk neutrality

Regulations impose idiosyncratic capital and funding costs for holding derivatives. Idiosyncratic costs mean that no single measure makes derivatives martingales for all market participants. Chris Kenyon and Andrew Green demonstrate that regulatory…

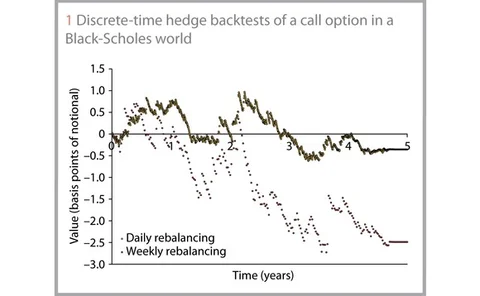

Hedge backtesting for model validation

Derivatives pricing and expected exposure models must be backtested as a basic regulatory requirement. But what does this mean exactly, and how can it be used to reserve against model risk? Lee Jackson introduces a general backtesting framework for…

Cutting edge: Valuation and optimal hedging of storage contracts in incomplete gas markets

In this paper, Magnus Wobben, Tilman Huhne, Yuri Ivanov and Sebastian Hanneken examine the impact of market incompleteness on the valuation of gas storage contracts. In contrast to prior research, their proposed valuation framework accounts for the…

Hedge backtesting for model validation

Hedge backtesting for model validation

LPI swaps with a smile

LPI swaps with a smile