Portfolio

Integrated stock–bond portfolio management

The authors put forward a stock-bond portfolio selection model which is based on CreditMetrics principles in which market and credit risks are naturally integrated.

Pricing the transition of Scope 3 emissions

A framework to measure banks’ costs associated with carbon emissions is proposed

Energy credit risk benefits from next-generation technology

Advances in energy credit risk technology are improving the accuracy and efficiency of the credit risk function, says credit risk technology expert

Five banks lowballed loan losses in latest DFAST

Banks project $23bn smaller hit to loan portfolios, with Wells Fargo and Citi the most off-target

Sherman ratio optimization: constructing alternative ultrashort sovereign bond portfolios

This paper explores the Sherman ratio and find that it has merit in the optimization of portfolio construction.

At US banks, share of HTM securities ticks up in Q1

Despite liquidity squeeze, regional banks increased proportion to a six-year high

Interest rate risk drives ING’s VAR to two-year high

Dutch lender’s trading risk indicator averaged €14 million in Q1

Western Alliance, PacWest put $9.8bn of loans up for sale

Embattled banks to dispose of 13% and 10% of respective loan books as strategic options talks continue

US banks seize chance to transfer securities from HTM to AFS

Wells Fargo, JP Morgan and Citi reclassify $34bn following new hedge accounting treatment

How Man Numeric found SVB red flags in credit data

Network analysis helps quant shop spot concentration and contagion risks

A model for small basket equities financing

A haircut model for equity baskets based on credit and equity indexes is introduced

ING’s Russia loans sour five times faster than UniCredit’s

Risk density of Dutch bank’s Russia portfolio soars from 54% to 229% during 2022

HTM securities hit $2.5trn at US banks in 2022

BofA, First Foundation and Wells Fargo reported largest share of HTM to total securities behind SVB

At regional US banks, BTFP-eligible securities top $300bn

Assets classified as held-to-maturity made up less than 19% of aggregate securities portfolios in 2022

Momentum transformer: an interpretable deep learning trading model

An attention-based deep learning model for trading is presented

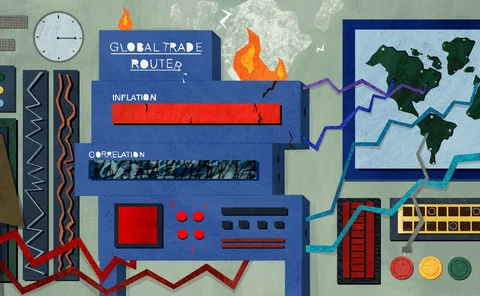

‘Globalisation rewired’: what does it mean for investors?

After half a century of outsourcing production to developing nations, companies are changing tack – with long-term implications for investors

Allocating and forecasting changes in risk

This paper considers time-dependent portfolios and discuss the allocation of changes in the risk of a portfolio to changes in the portfolio’s components.

FX Smart Clearing at LCH ForexClear: solving SA-CCR capital challenges

LCH ForexClear explores how, with the standardised approach to counterparty credit risk increasing the capital requirements of banks’ FX portfolios, its FX Smart Clearing solution can reduce capital burden and achieve additional savings for members

Is low vol crowded? That depends who you ask

Equity drawdowns have pushed more investors into low volatility strategies, raising fears of a build-up of risk

MMFs’ reverse repos with Fed surged 35% last year

Fidelity-run funds drove 29% of the $601 billion in new trades

IRB risk-weights highest at smallest EU banks – ECB

Lenders with less than €30 billion in assets consistently report lower risk densities than bigger banks across all modelled portfolios

JP Morgan nets $1.9 billion bond book gain in swift turnaround

Q4 reversal in fair-value securities powers record quarterly increase in CET1 capital

Pricing options using expected profit and loss measures

The authors investigate the pricing of options using an EP-EL approach, finding that this methodology generates large amounts of useful information for option traders.