Portfolio modelling

On capital allocation under information constraints

This paper offers a portfolio optimization framework that uses return data to calculate an optimal capital allocation based on a Cobb–Douglas utility function.

Covid scenarios: finding the worst worst-case

As pandemic trashes historical data, a Risk.net tie-up with Ron Dembo’s new outfit tests promise of polling

Genetic algorithm-based portfolio optimization with higher moments in global stock markets

This paper investigates the distributional characteristics of stock market returns and analyzes the significance of higher moments.

Energy trading firms race to improve analytics capabilities

Surging availability of data lets firms with best market insight gain an edge

The application of Hermite polynomials to risk allocation

This paper investigates a practical and fast analytic framework for portfolio modeling and tail risk allocation using Hermite polynomials.

Need for speed: banks explore FPGAs for portfolio modelling

The gate array way

Cutting edge introduction

A popular copula

CPM functions go back to basics

Old-school value

Myron Scholes predicts 'golden age' for quants

Top quant sees bright future for mathematical finance as it tackles problems thrown up by the crisis

State Street advises institutional investors to move away from modern portfolio theory

New report suggests investors should move away from using normal return distributions under modern portfolio theory

Component VAR for a non-normal world

Market Risk

Crossing the frontier

Portfolio risk management

Standard & Poor's enters portfolio risk modelling

Standard & Poor's (S&P) Risk Solutions has launched a portfolio risk tracker model. The model covers both credit and market risk, which should allow banks to calculate their economic capital and perform risk assessments across the full range of risks…

Credit ensemble

Kevin Thompson and Roland Ordovas address the question of how individual counterparties contribute to the total credit risk of a portfolio. They provide an analytic method, new to credit modelling, to estimate all joint default statistics conditional…

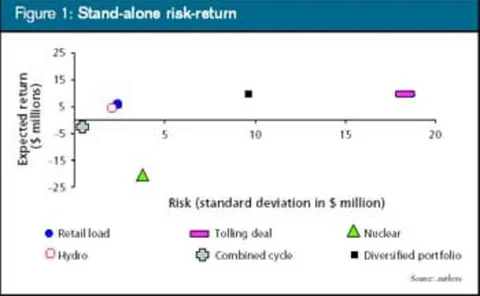

Optimise this

One of the reactions to recent energy trading difficulties has been a shift away from speculative activities towards portfolio optimisation, but what does the term really mean, ask Tim Essaye and Brett Humphreys

Minimising extremes

Portfolio diversification often breaks down in stressed market environments, but the co-movement of asset prices in a tail risk regime may be modelled using a coefficient of tail dependence. Here, Yannick Malevergne and Didier Sornette show how such…

VAR: who contributes and how much?

Portfolio risk management

Forward thinking

Forward simulation