Risk magazine - Volume18/No11

Articles in this issue

Dealers work to meet deadlines

New angles

Recovery swaps trading on the rise

New angles

Tranche value on a yo-yo

Correlation trading

A new sweet spot

Soft commodities

Unbiased risk-neutral loss distributions

Luigi Vacca introduces entropy maximisation (ME) to derive portfolio loss probabilities that are consistent with standard tranche prices on a credit default swap index. Tranche prices that are calculated using ME are free of arbitrage. A numerical…

An economic capital approach for hedge fund structured products

Hedge fund structured products are increasingly favoured by investors. Banks have been swiftly developing their commercial offers to meet this demand. However, the theoretical framework for the risk management of these products remains little explored,…

Trading down the slopes

The credit derivatives market is growing at an impressive rate, with the credit default swap (CDS) being the most popular instrument. This article is relevant for the trading of CDSs and bond portfolios. Mascia Bedendo, Lara Cathcart, Lina El-Jahel and…

Another chapter for credit

Comment

South Africa

Introduction

A focus on ETFs

Structured products

Direct access

Hedge funds

Nordic risk

Introduction

Harvesting potential

Profile: Hedge funds

Mixed signals for derivatives

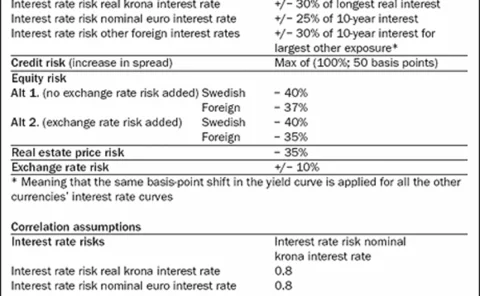

Solvency reform

Leading the pack

Basel II

A step up the ladder

Basel II

Widening the spectrum

Credit risk

Warming to exotics

Structured products