Risk magazine - Jun 2019

In this issue: the perils of placing regulators at the controls; how seven banks are tackling the Libor transition; the FXPB powder keg; US regional banks; and much mor

Articles in this issue

Can European banks crack the capital allocation code?

Banks “stuck on the same feedback loop” due to sheer weight of capital rules

JP Morgan turns to machine learning for options hedging

New models sidestep Black-Scholes and could slash hedging costs for some derivatives by up to 80%

Talk of delaying IM ‘big bang’ sparks backlash

EC official's recent comments may hamper compliance preparations, dealers say

Swaps users mull ‘big bang’ for SOFR discounting

Cleared and bilateral US dollar swaps could move to SOFR discounting on the same day in 2020

Fed pushes big banks to calculate CVA for CCPs

Banks including JP Morgan and Credit Suisse told to quantify exposure to CCPs for annual stress tests

Volatility scaling unravels as market patterns shift

Waning power of quant approach could be a reason for trend following’s malaise

Final FRTB tweak ‘will kill correlation trading’, say dealers

Some European banks plan to lobby ECB for relief when rules are transposed to local law

People moves: new role for SG CIB’s Cartier, LCH rates head departs, BNP Paribas’s Akbay joins Goldman, and more

Latest job changes across the industry

New applications in Asia’s financial crime analytics

Financial crime is a fast-growing problem for Asia‑Pacific financial services firms. Working with outmoded systems and patched-up processes to detect, monitor and eliminate potential threats, banks are spending millions on sophisticated new solutions to…

How capital rules overwhelmed bank strategy

Regulators shouldn’t run a bank – but Basel III and stress tests have put them in the cockpit

A powder keg in forex: the prime broker business

Brokerages look at high-speed algo trading paired with bloated credit limits – and shudder

US mid-sized banks may bulk up. (Is that safe?)

The crisis over a decade gone, the Fed’s ‘tailoring’ proposal will greatly relax rules on the mid-tier

Libor leaders: how seven firms are tackling the transition

BMO, Prudential, Associated British Ports, LCH and others reveal their plans to move off troubled benchmark

Not random, and not a forest: black-box ML turns white

Bayesian analysis can replace forest with a single, powerful tree, writes UBS’s Giuseppe Nuti

Financial firms toil to meet new EU rules on outsourcing

Negotiating right to audit vendors, including cloud providers, seen as toughest requirement

Operational resilience means learning from failure

Firms and regulators could share data on mistakes, says Garp’s Jo Paisley

Outsourcers eye bigger role in funds’ fixed income trading

Research suggests 20% of large asset managers will outsource part of overall trading by 2022

Sonia advances: liquidity builds as banks eye interdealer shift

Libor’s successor has some solid footholds. Wider acceptance could come as soon as later this year

Fund-linked structured products face extinction under FRTB

Global market risk capital standards carry sky-high charges for fund derivatives

How does it look from space? Satellite surge to alter investing

Higher-frequency images set for use in entirely new ways and by more investors than before

Fund houses get picky over where to use machine learning

Buy-siders limit usage of deep learning techniques due to haziness over their inner workings

Neuberger trusts market-timing model to hook China investors

Fund aims to smooth returns for buy-siders spooked by past market dips

Analytics become top priority at energy firms, poll finds

Middle office still grappling with use of blockchain and artificial intelligence

Getting risk models runway ready

Banks struggling with internal model requirements may soon opt for off-the-rack rather than bespoke

US G-Sibs keep on expanding repo books

JP Morgan has increased repo exposure by 34% year-on-year

Eurozone insurers’ bets on alternatives raises systemic risk

Dutch firms have more than 25% of total assets tied up in non-traditional investments

EU’s model study finds problems with bank VAR methods

Banks surveyed by the ECB had an average of 32 issues with their market risk models

Short-term bets push interest rate option volumes higher

Open interest in short-dated contracts surges 23% from December to March

UK public sector offloads swaps

Gross derivatives outstanding with public entities stood at £5.9 billion in Q1

Op risk data: Chinese regulators levy record fines

Also: top losses feature two frauds at Russia banks and AML provisions at Nordea. Data by ORX News

Credit data: more trouble in the oil and gas pipeline

US self-sufficiency in oil could be bad news for shale producers

Swaps data: a new era of competition in interest rate futures

The demise of Libor has set off a battle for market share in futures referencing new risk-free rates

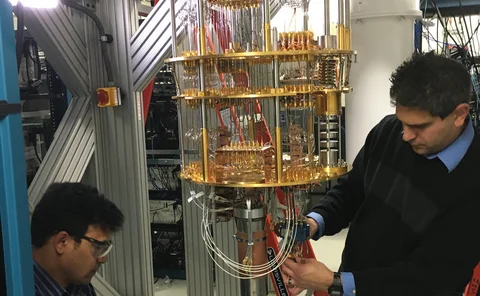

Time to put real problems to the quantum machines

There is a lot to learn before quantum computers can be applied to specific financial problems

Beyond Markowitz with quantum annealing

Venturelli and Kondratyev use quantum annealers to optimise portfolios

Capital allocation under the Fundamental Review of the Trading Book

Quants propose an allocation method for internal model capital charges

The fair basis

Wujiang Lou remodels credit arbitrage by introducing funding and capital costs

RJ O’Brien’s chief risk officer on margin models and clearing

CME’s looming switch to VAR model will have pronounced effect on broker and its clients, says Brad Giemza