Swaps data: Fed’s change of tack on rates fuels volume rise

Cleared dollar rates jump by half year-on-year, as LCH market share tightens

It was a mixed second quarter of 2019. The US Federal Reserve’s protracted signalling of its July rate cut prompted a significant rise in cleared US dollar rate swaps volumes versus the previous quarter and versus the same time last year. Yet cleared volumes in euro-denominated rate swaps are significantly down, as are credit default swaps in all currencies. Yen rate swaps and non-deliverable forwards meanwhile are flat or modestly up.

Little has changed in terms of market share between the big clearing houses. LCH’s SwapClear is slightly up in US dollar rates, while JSCC is slightly up in yen rates. In credit default swaps clearing, LCH’s CDSClear sees its share tick up in euro CDS clearing.

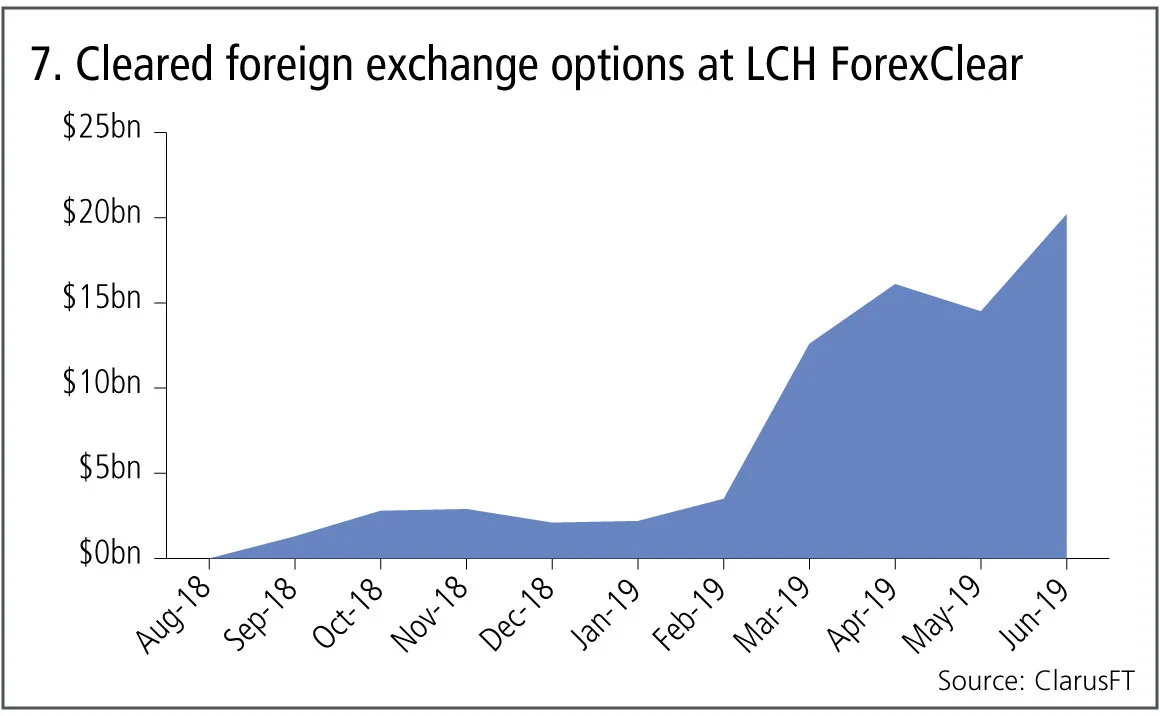

One notable pocket of growth is foreign exchange options clearing, where volumes at LCH ForexClear grew markedly in June. Could this be the first over-the-counter option to move in a big way to clearing? Or will regulators’ decision to split the final ‘big bang’ phase-in of margining for non-cleared derivatives and delay the mandate for smaller swaps counterparties check progress for now?

Some large dealers have historically underpriced their foreign exchange prime brokerage services in order to win more execution business from funds and proprietary trading firms. At least one large bank is repricing its offering to big buy-side users of OTC forex trades, which could be another factor behind the uptick in clearing volumes.

With the costs of trading non-cleared OTC rising significantly for some as a result – and with some banks quietly jettisoning clients in the meantime – the market could yet move to greater use of clearing. LCH should be the main beneficiary, if that happens; if the market instead looks to replicate its currency risk in cash-settled options, however, CME Group could be the happier central counterparty.

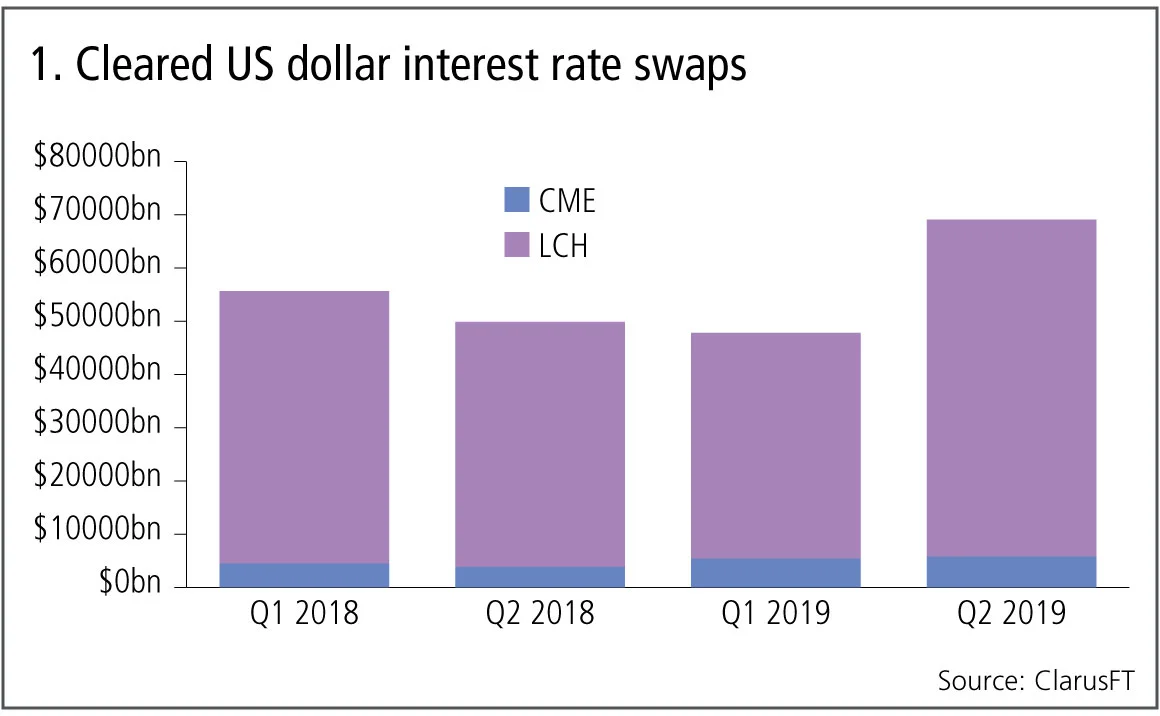

Cleared US dollar swaps

We include all clearable types when tracking US dollar interest rate swap volumes – vanilla fixed versus float, overnight index, basis, zero coupon and variable notional – and use single-sided gross notional volumes.

Figure 1 shows:

- Q2 2019 volumes are 44% higher than Q1 2019, at $69 trillion – 38% higher than a year earlier.

- That’s a very different trend to Q1 2019, which saw volumes fall 14% from a year earlier.

- LCH SwapClear sees its market share increase to 92% in Q2 2019, up from 89% during the prior quarter, with CME down to 8% from 11%.

- In terms of raw volumes LCH SwapClear is up $17 billion from a year earlier, or 38%. CME is up $1.9 billion or 49% from a year earlier.

The Federal Reserve signalling a cut in US interest rates certainly resulted in much higher dollar swap volumes during the quarter, as firms moved to reprice their expectations of a gradually rising path for US rates. However, how the market reacts to Fed chairman Jerome Powell’s verbal intervention dampening hopes of further rate cuts – much to US president Donald Trump’s ire – remains to be seen.

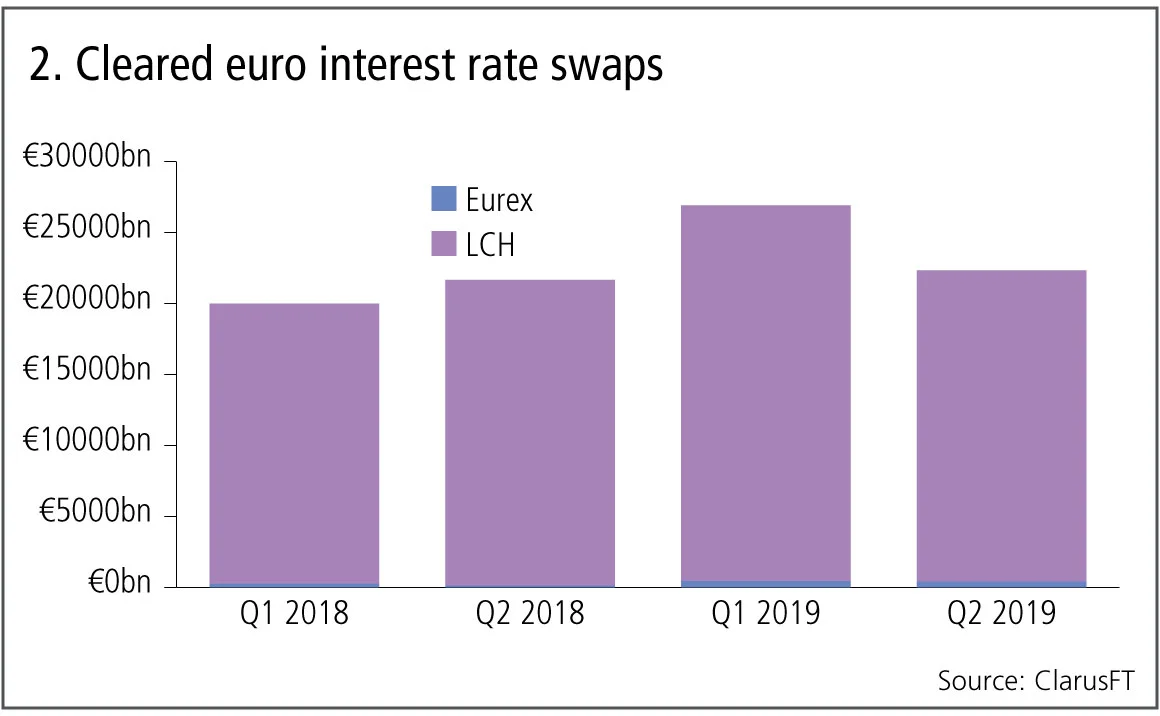

Cleared euro swaps

Figure 2 shows activity in the second-largest product, cleared euro interest rate swaps, across all clearable instrument types.

Figure 2 shows:

- At €22 trillion ($24.6 trillion), Q2 2019 volumes are 17% lower than Q1 2019, and 3% higher than a year earlier.

- Market share split is little changed from Q1 2019: LCH SwapClear has a 98.1% share, Eurex 1.9%.

- In terms of raw volumes, LCH SwapClear is up 2% or €386 billion from a year earlier, while Eurex is up 209% or €286 billion from a year earlier.

So, LCH SwapClear continues its dominance in euro swaps clearing – but Eurex is continuing to grow at a much faster rate, from a much lower base.

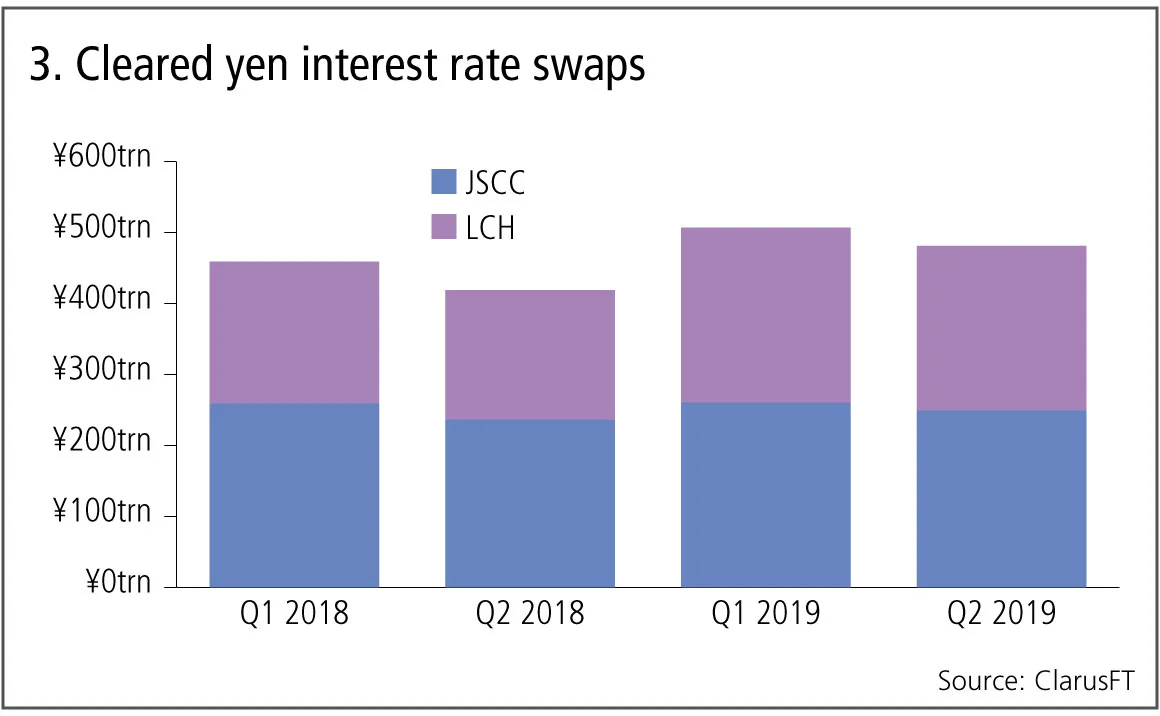

Cleared yen swaps

Figure 3 shows:

- At ¥481 trillion ($4.5 trillion), Q2 2019 volumes are 5% lower than Q1 2019, but 15% higher than a year earlier.

- JSCC market share sits at 52% and LCH’s at 48% in Q2 2019 – a gain of 1% in JSCC’s in favour compared with Q1 2019. A 52:48 split sounds like unfinished business.

- In terms of raw volumes, JSCC is up 5% or ¥13 trillion from a year earlier; LCH is up 26% or ¥49 trillion.

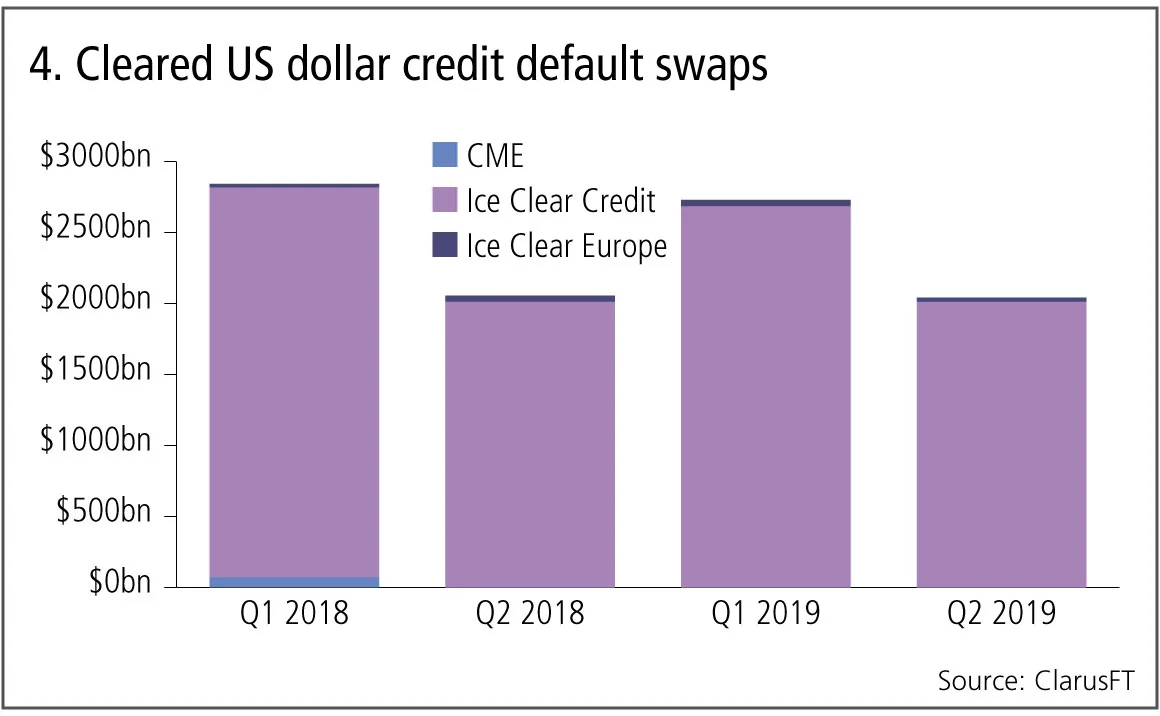

Cleared US dollar credit default swaps

Next, let’s take a look at volumes in cleared dollar-denominated credit default swaps.

Figure 4 shows:

- Q2 2019 volumes are 25% lower than Q1 2019 at $2 trillion, and 1% or $13 billion lower than a year earlier.

- Ice Clear Credit dominates with a 99% market share.

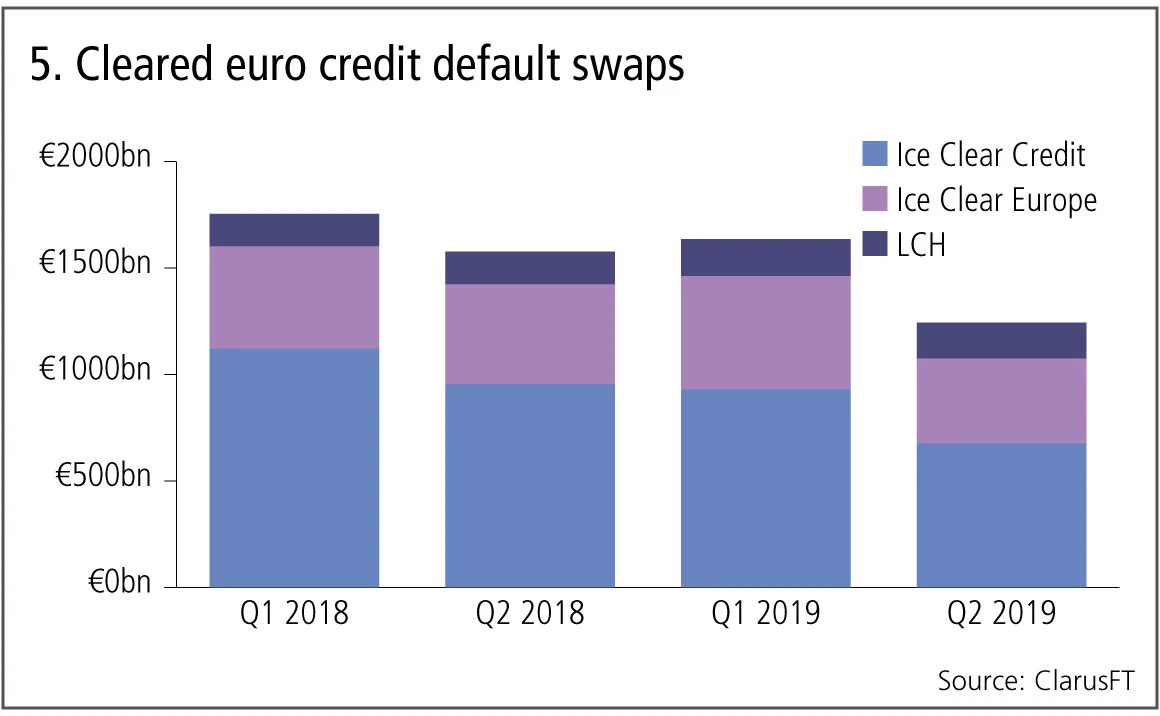

Cleared euro credit default swaps

Next, the volume of credit indexes and single names in euros.

Figure 5 shows:

- Q2 2019 volumes are 24% lower than Q1 2019 at €1.25 trillion, and 21% lower than a year earlier.

- Ice Clear Credit with 54.3%, Ice Clear Europe 32% and LCH CDSClear with 13.7% market share in Q2 2019, which compares with 56.8%, 32.6% and 10.6% in Q1 2019, respectively.

- Ice Clear Credit’s volumes are down 29% from a year earlier, Ice Clear Europe down 15% and LCH CDSClear up 10%.

Cleared credit derivatives volumes denominated in euro mirror the drop in US dollars for the most recent quarter, and show a much larger drop year-on-year, with only LCH CDSClear increasing its volumes and share.

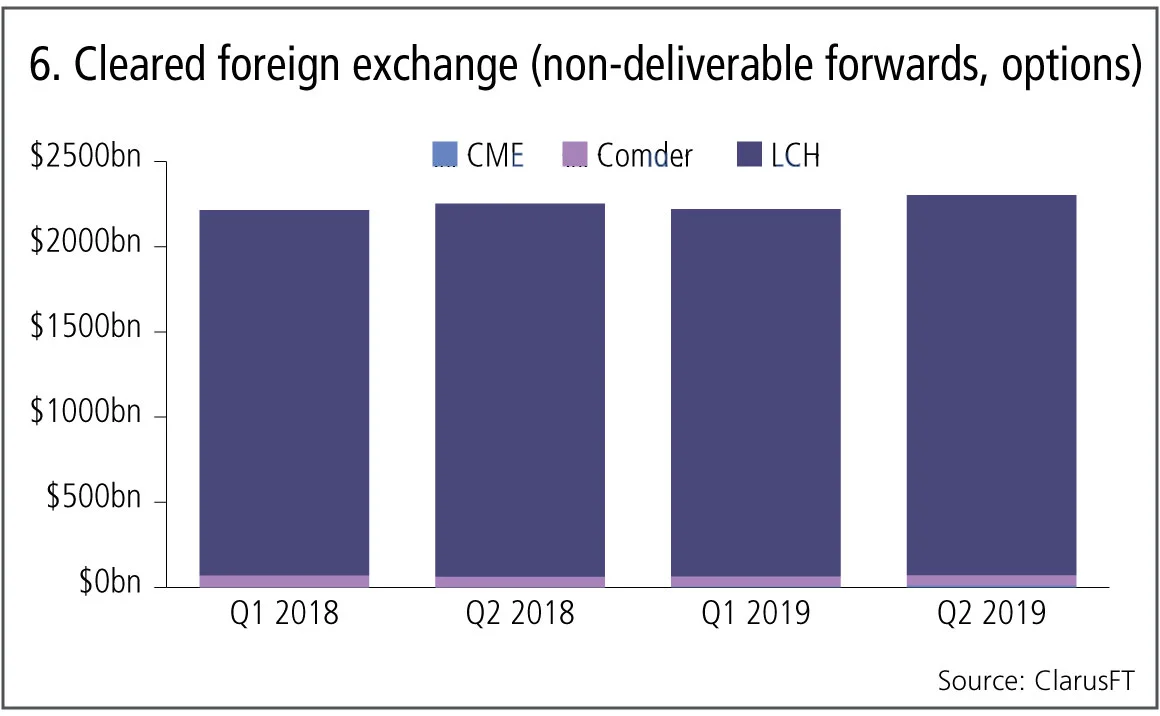

Cleared non-deliverable forwards

Finally, let’s take a look at cleared non-deliverable forwards.

Figure 6 shows:

- Q2 19 volumes are 2% higher than a year earlier at $2.3 trillion.

- LCH ForexClear with 97% share in the quarter, with Comder on 2.6% and CME with 0.5%.

Cleared non-deliverable forwards volumes no longer show their long-running trend of high growth, pre-2018. We may have to wait for non-cleared margin rules phase 4, 5 and 6 for a return to that.

However, delving further into the LCH ForexClear numbers, we do see growth in forex options clearing, with $20 billion gross notional in June 2019, up from $14.5 billion in May 2019.

Amir Khwaja is chief executive of Clarus Financial Technology

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

オペリスク・データ:企業スパイがBBVAに脅威をもたらす

他にも:BofAがエプスタイン氏との関与疑惑で追及されています。また、少数株主がブルックフィールドに異議を唱えています。データ提供:ORX News

AI政治の台頭

MASの顧問であるデビッド・ハードーン氏は、AIを単なる一つの技術として扱うべきではないと述べています

AIリスク管理と能力制御への移行

リスク管理者によると、検証の枠組みを見直すことで、銀行はイノベーションと規制上の要件を両立させ、強固なリスク管理体制を維持することができます

トークン化された商品市場は、経済の円滑な運営に寄与する可能性がある

暗号資産の専門家は、実物資産をブロックチェーンに移行することで、担保に関する摩擦が緩和されると主張しています

GenAIの時代において、未だに優れたモデルが必要なのはなぜなのか?

ジャン=フィリップ・ブショー氏は、モデルが人工知能をレジームシフトの過程で導き、過学習から遠ざけることができると述べています

取引のスピードがガバナンスを上回る時:一瞬の統制の隙間

デリバティブの専門家によると、光駆動型エレクトロニクスの新たな形態が、市場インフラにおける次のリスクとなる可能性があるとのことです

先物とオプションが示す戦争のコスト

現物価格は大きな混乱を示していますが、先物市場はこれが一時的なものだと示唆しており、オプション市場は不安定な状況が続くと示唆しています

担保に関して、TINAはTIAになることができるのか

あるエコノミストは、レポ取引やデリバティブ取引における担保としての米国債の優位性は、もはや揺るぎないものではないと指摘しています