How Amazon and Netflix disrupted value investing

New business models have upset a common metric in the quant strategy

The disruption economy is upsetting one of the oldest systematic investment strategies.

Value investors buy unfashionable underpriced stocks and wait for them to come back into vogue with investors. The difficult part is distinguishing those stocks that are cheap for a reason from those that are just cheap. At its core, the strategy relies on frothy markets reverting to the mean.

Digital disrupters have thrown a spanner in those works and are an important part of the reason the strategy has done poorly in recent years. By wrecking old business models, companies like Amazon, Netflix and Uber have created a class of companies that are dying slow deaths and a class of winners that value strategies inadvertently ignore.

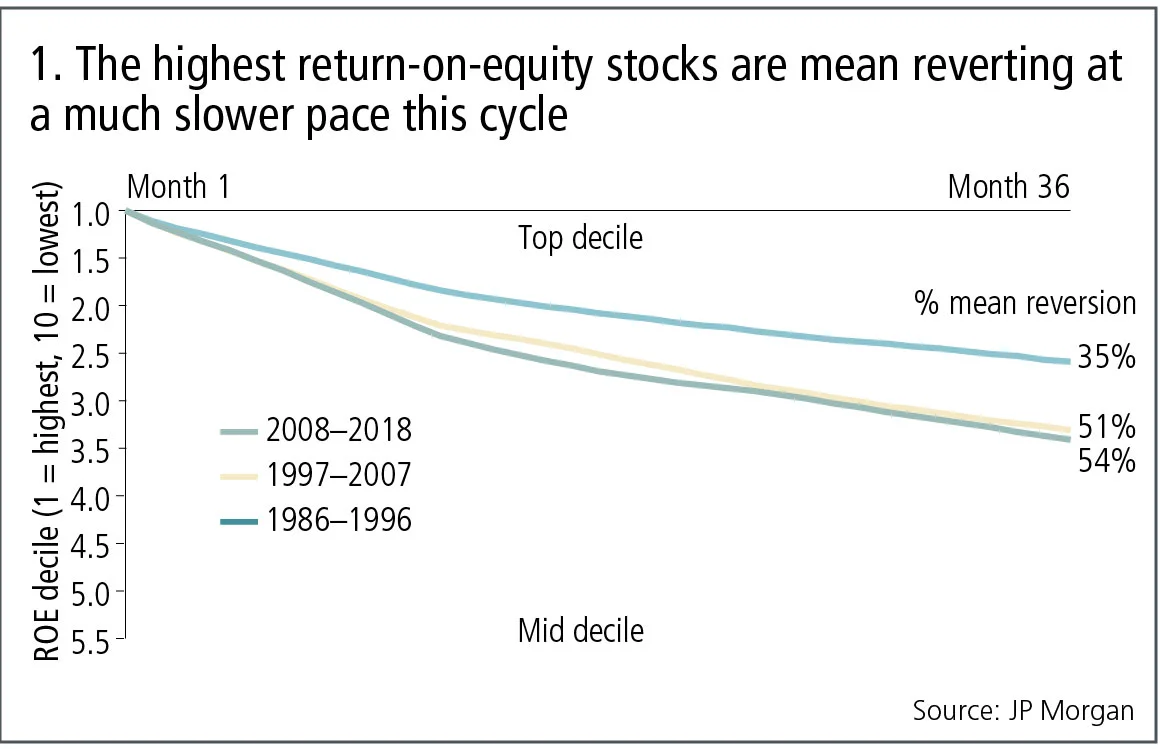

The effect is that mean reversion has slowed. Winning stocks are winning for longer and cheaper stocks are languishing for longer, too, creating a drag on the strategy (see figure 1). Dubravko Lakos-Bujas, JP Morgan’s global head of quantitative research, calls it a “winner takes all” economy. “The mean reversion story that we’ve seen play out in history over and over is still alive, but in this cycle it is taking a lot more time,” he says.

Lifetime bargains

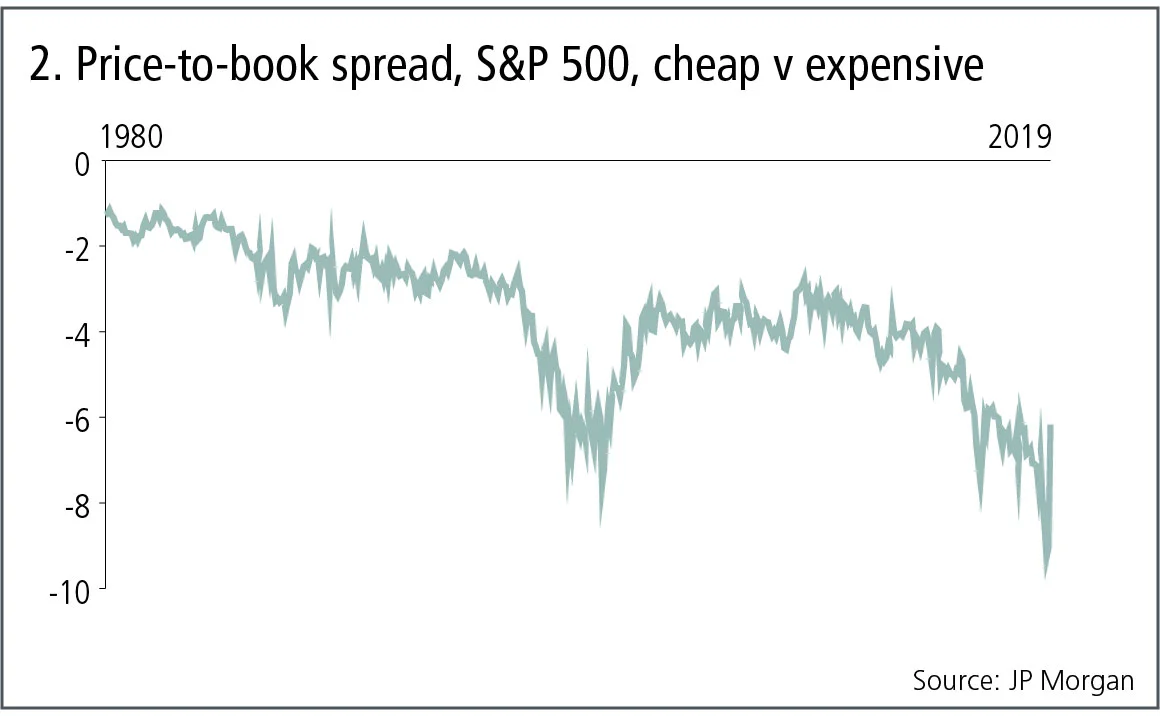

The irony here is that in one sense quant value strategies have seldom looked more attractive. Cheap stocks are close to the cheapest compared with rich stocks they have ever been (see figure 2). But the value trap created by disrupters calls for changes to quant thinking.

Price-to-book – the longest-standing and most common metric used to filter value stocks – “stands out as the big loser”, says Vitali Kalesnik, head of quant equity research at Research Affiliates.

This simple ratio of a company’s stock market valuation to the worth of its assets is more prone to selecting junky companies, ignores intangible assets and is oblivious to the quality of the enterprise. “In the current environment, it’s not a good measure,” as Kalesnik puts it.

An undervalued technology company with few tangible assets other than computers, desks and sharp-minded programmers, for example, scores a high price-to-book ratio. Value filters that rely too far on price-to-book will ignore such companies, along with a host of other key sectors. That is a special problem in the US, where service-based businesses dominate.

Partly, this should be no surprise. Price-to-book was conceived as part of an academic exercise. When Eugene Fama and Kenneth French, the architects of systematic value investing, developed and tested quant value strategies 30 years ago, they didn’t try to create the best approach for all environments and all eventualities.

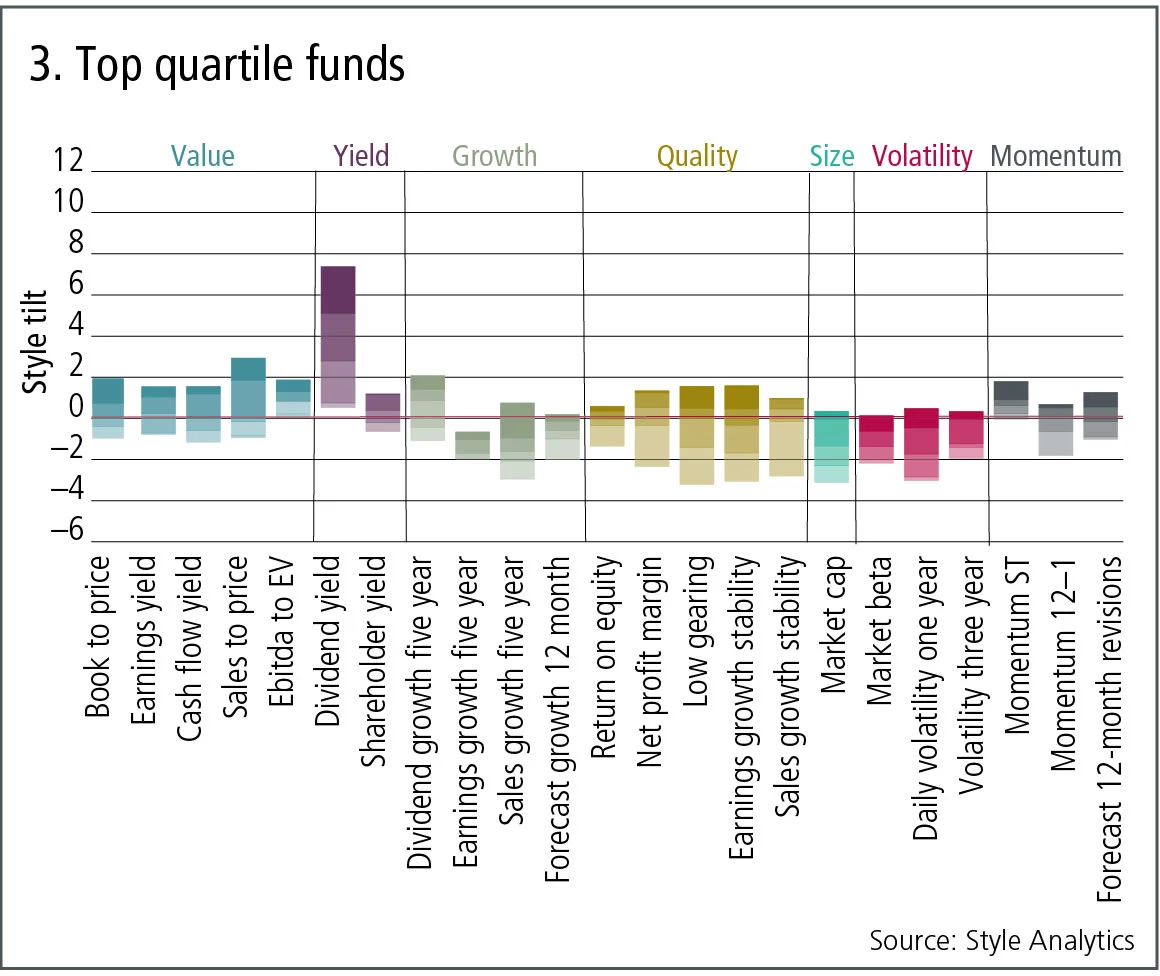

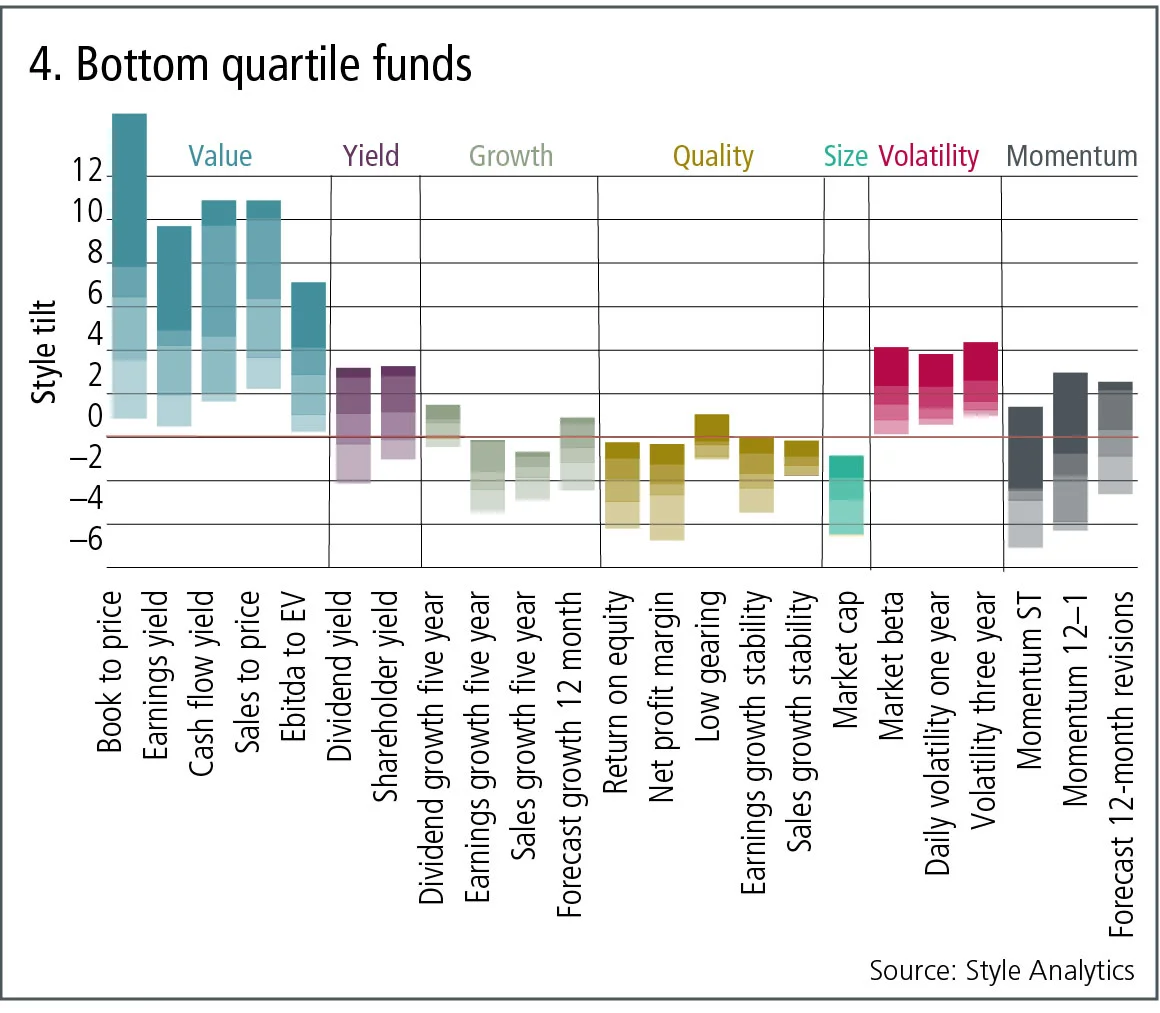

US value funds with an outsized tilt to price-to-book did especially badly in the last quarter of 2018 and first quarter of this year (see figures 3 and 4), according to Style Analytics, a provider of factor analytics. Funds that fared better tended to favour an alternative metric – high dividends.

That’s not to say quants should simply ditch price-to-book. For a start, it still works in some regions. In Europe, for example, where the manufacturing base is proportionally bigger, price-to-book remains more useful.

And other indicators have flaws, too. Dividend yield – the standout metric in the Style Analytics analysis – generally works well in Europe, but less well in the US where share buybacks are a popular way to return cash to investors.

One solution is to tailor the metrics to the markets and sectors where they are applied. Kalesnik advocates adding to quant models measures such as price-to-cashflow, -sales and -dividends over five-year averages. Doing so is a way to capture “quality companies that are also cheap”, he says.

Many quants see good prospects for a revival in value strategies, despite the drudgery of recent years. But the influence of Amazon and the like means quants must be careful about how they measure what they manage.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら 我々の見解

「ライトタッチ・ブリゲード」への追加料金

米国のG-Sibサーチャージの改革は、単なる見直しをはるかに超えるものです

Do banks still need to validate GenAI models?

Regulators carved out GenAI models from new risk guidance. Banks shouldn’t see this as a reason to stop validating them.

イランをめぐる混乱は、因果モデル化の必要性を裏付けている

Claudeを用いて構築された新しい予測モデルによると、原油価格は再び100ドルを上回る可能性があると示唆されています

クレジット市場の計算が合わない様子である

今日の投資家にとっては、「リスクの高い」債券を購入するほうが得策であるように思われます

イラン情勢により、外国為替取引は不可能になってしまったのだろうか

コストの高さや機会の短さにもかかわらず、FXオプションの取引高が急増しています

Can AI be the great equaliser in e-FX?

FX market-makers see real benefits for agentic AI in code generation and data analysis

モデル・リスク・マネージャーの孤独

取締役会は、それらをイノベーションの足かせと見なすかもしれません。リスク管理部門は、効率性を重視していることを示す必要があります

複雑なボラティリティ曲面へのスムーズフィット

Quantは、オプティマイザーを用いたインプライド・ボラティリティの新たな捕捉手法を示しています。