Doubts cast on Europe’s IFRS 9 transition period

Dynamic transition viewed as too complicated for banks to use or investors to understand

Doubts have been raised over the usefulness of a transition period designed to mitigate the day one capital impact of new accounting rules, owing to the complexity of the European Union’s chosen approach.

International Financial Reporting Standard 9 (IFRS 9), which comes into force for European banks in January 2018, will upend current accounting convention by forcing banks to recognise expected losses on loans when the likelihood of the borrower defaulting increases materially. This is expected to increase provisions significantly, especially for smaller banks.

The likely knock-on effects on bank capital, with dealers forced to divert retained earnings to increase loss provisioning, has prompted the EU to offer a five-year transitional arrangement, but banks have criticised its approach as too complex to be of use.

“Personally, I would prefer to have no transition. The reason is that the impact studies are showing the one-off impact is not going to be that big, so therefore I don’t think there is any institution that is going to struggle with a one-off application of IFRS 9,” said Adrian Docherty, head of financial institutions advisory at BNP Paribas, speaking at the Banking Book Summit in London on November 28.

“If it reduces the impact, then great, but the cost of that is complexity. Europe has decided to allow a multitude of approaches and to allow the dynamic approach, which is very difficult to understand,” he added.

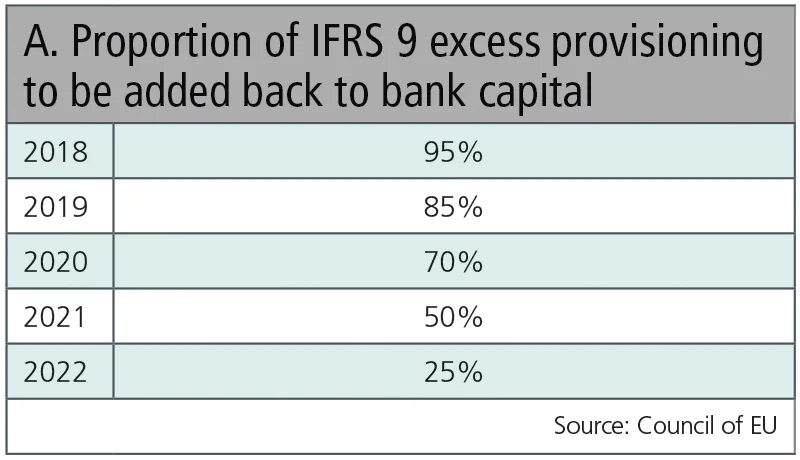

On 15 November, the Council of the EU endorsed an agreement with the European Parliament for a five-year transition period, which will allow banks to add their expected credit loss provisions resulting from IFRS 9 back to their capital in a decreasing amount over five years (see table A).

This is designed to offset the impact of extra provisioning on capital, particularly for banks using the standardised approach to calculate credit risk-weighted assets, rather than using forward-looking loan-loss models.

We have seen with Basel transitioning that the market, faced with all of this complexity and lack of harmonisation, just says ‘give me fully loaded’

Adrian Docherty, BNP Paribas

The final transition package allows banks to choose between static or dynamic approaches – that is, to calculate the capital offset once at the start of the transition period or to update it each year. The European Banking Authority had earlier advised against the dynamic approach, which is much more complicated to calculate – for banks and their investors.

“We have seen with Basel transitioning that the market, faced with all of this complexity and lack of harmonisation, just says ‘give me fully loaded’. With the phase-in, I know the provisioning is coming, so it may as well be shown in today’s numbers anyway,” said Docherty.

Speaking on the same panel, Ingrid Nemetz, an IFRS 9 specialist at the Austrian Financial Market Authority, acknowledged Docherty’s concerns.

“It is a difficult compromise solution. There were many views contradicting each other, and what we are now getting in the end is a very complex transitional arrangement. In this way, it has quite some similarity with IFRS 9 itself, which had a simple goal, and there were so many views and [so much] lobbying that it is rather complicated. Personally, I would have preferred, if we had a transitional arrangement, to have a simple one that is easy to understand, which would have been a static one,” said Nemetz, who emphasised she was speaking in a personal capacity.

“But, on the other hand, there was reasoning, which was the fear of volatility and the dynamic nature of IFRS 9 itself, so now we have this dynamic component of the transition period. I think it is hard to understand and even harder to implement technically, because there are so many consequential calculations you have to do for exposure values and for deferred tax assets. If you want to do that, it is quite an effort, and I’m not sure if banks are going to use it,” she added.

Nemetz also agreed with Docherty that investors are likely to look through the transitional number to the final IFRS 9 reported balance sheet.

Waiting for Basel

However, Docherty emphasised the transition period could be useful if it gave time for the Basel Committee to agree changes to credit risk capital rules that would allow all banks to add back to capital any accounting provisions beyond the regulatory expected 12-month losses. This is essential for banks on the standardised approach to credit risk, which must otherwise double-count the cost of the additional IFRS 9 provisions in their capital ratios.

“If it’s the wrong destination, then any transition is the wrong thing to do… But any solace, any mitigant, any reduction or neutralisation of IFRS 9 is welcome,” said Docherty.

He said the European Banking Federation was already in contact with the Basel Committee, which understood the situation, but he warned the market needed clarity quickly.

“That process is happening, but I don’t think the Basel process is going to adapt to IFRS 9 very quickly. The transition helps, but we have to make sure the market realises there is going to be some sort of ‘compatible-isation’ of the capital with the provisions framework, and try to keep it together until Basel can do something. But, as we have seen with Basel IV, the Basel process is quite difficult when working internationally,” said Docherty.

In its half-yearly Financial Stability Report, also published on November 28, the Bank of England made clear the need for the capital impact of IFRS 9 to be neutralised: “The Financial Policy Committee will take steps to ensure the interaction of IFRS 9 accounting with its annual stress test does not result in a de facto increase in capital requirements.”

Nemetz also expressed pessimism regarding how fast the Basel Committee could proceed with adapting the credit risk capital framework for IFRS 9.

“It is good to have simple solutions and equal methods, but that is hard to reach – there are different goals from the prudential point of view and the accounting point of view, [which is] the true and fair view. I am not sure if that is going to be reached in the mid- or long-term. We didn’t even reach common accounting standards with US GAAP,” said Nemetz.

Following six years of negotiation, a project to converge IFRS with the US Generally Accepted Accounting Principles failed in February 2014.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら 規制

EU当局者は銀行の資本規制緩和への期待を抑制している

欧州委員会の競争力見直しにおいて、資本規制緩和は米国での規制緩和にもかかわらず、確定したものではありません。

EU規制当局、ESMAへの監督権限移譲をめぐり対立

ベルギーとスペインの規制当局は、国境を越えて事業を行う企業に対する集中的な監督体制の構築に向けた取り組みについて見解が分かれています。

トランプ氏の最新の「真実」が伝統的金融業界を不安にさせる理由

ウォール街はトランプ氏のクリプト映画の中の悪役となりつつあります

EBAのガイダンスにより、銀行はCSRBBの範囲について再考するよう促されている

銀行は、勧告を受けて信用スプレッドリスクのカバー範囲を拡大する必要が生じる見込みです。

市場関係者は欧州のレポ決済義務化に警鐘を鳴らしている

規制当局には、米国による義務付けの結果を待つよう求められ、国債の流動性に対するリスクに警戒を怠らないことが求められています。

ESMAはクラウドとAIに関する規制上の期待を緩和することはない

CCPの監督責任者は、サードパーティリスクとオペレジに対する監視強化を示唆しました。

BPIはSR 11-7の廃止を主張しているが、銀行のモデルリスク責任者らはそれを反対している

ロビー団体は米国の指針廃止を求めておりますが、実務家側は一貫したモデル監督と監査を望んでおります。

ESMAの監督案がブルームバーグとトレードウェブを巻き込む

デリバティブおよび債券取引所は、中央集権的な監督の対象となります。