Asia Risk - July 2006

Articles in this issue

Taking stock in shanghai

Q&A: James Liu

Still much to do

Basel II

Editor's Letter

Comment

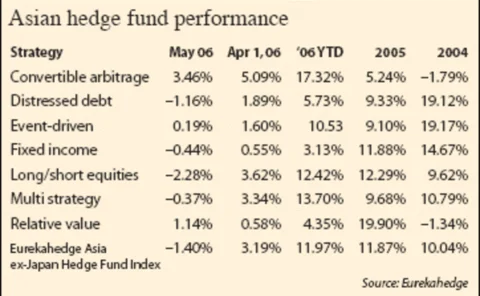

Asian hedge funds down, says Eurekahedge

Negative hedge fund returns on the back of a downturn in regional equity markets

Mining a rich seam

BHP Billiton

A classic chinese recipe

Profile: Jean-Philippe Frignet

Sweet and sour

Crude oil

CME to launch renminbi futures in August

Chicago Mercantile Exchange sets out its stall in Asia

Called to account

Japan auditing

China's changing face

China

Keeping it simple

Profile: Towngas

Hedge funds are cash kings among asset managers

Risk professionals at asset managers see big compensation rises

Cash for old smoke

Carbon emissions

Back on the ranch

Profile: Ralph Liu

More bond market transparency desirable, say Iosco panelists

Regulators need balanced touch on bond market

Bank of China warrants list in Singapore

Deutsche Bank is the first to list call warrants on BoC IPO

A seasonal evening

End-user survey

A tale of two structures

Securitisation

Taking the slow road

CDOs

Ready to catch fire

Energy

Ready for take-off

Regulation

CMCDS valuation with market models

There is little, if any, literature available on constant-maturity credit default swap (CDS) valuation. Here, Damiano Brigo builds on his no-arbitrage dynamic CDS market model to derive a formula involving a 'convexity adjustment' feature correction,…

Drawn to derivatives

Market overview

Return of a heavyweight

Japan derivatives

Hedge funds need balanced supervision by regulators, say Iosco panelists

Investors must be protected, but hedge funds should not be discouraged

Insurers warm to synthetic debt

Taiwan CDOs

Sun sets on yen carry

Carry trades

Banks bemoan Basel

Taiwan