Option pricing

Error analysis in Fourier methods for option pricing

The authors provide a bound for the error committed when using a Fourier method to price European options, when the underlying follows an exponential Lévy dynamic.

An efficient convergent lattice method for Asian option pricing with superlinear complexity

In this paper the authors present an efficient convergent lattice method for Asian option pricing with superlinear complexity.

Valuation of barrier options using sequential Monte Carlo

The authors present Sequential Monte Carlo (SMC) method for pricing barrier options.

A reduced basis method for parabolic partial differential equations with parameter functions and application to option pricing

The authors introduce an RB space–time variational approach for parametric PPDEs with coefficient parameters and a variable initial condition.

Deconstructing correlation

Peter Austing introduces an analytic or semi-analytic valuation of basket options

A new improvement scheme for approximation methods of probability density functions

This paper develops a new scheme for improving an approximation method of a probability density function.

Johnson-Omega performance measure

Alexander Passow presents a portfolio performance measure that combines the omega measure with Johnson distributions

Stratified approximations for the pricing of options on average

The authors propose stratified approximations of option prices using the gamma and lognormal distributions, with an application to bond pricing in the Dothan model.

A novel Fourier transform B-spline method for option pricing

By means of B-spline interpolation, this paper provides an accurate closed-form representation of the option price under an inverse Fourier transform.

Trading calendar spread options on energy futures

Sponsored feature: CME Group

American options: time-critical pricing

Time constraints can be binding for ‘heavy’ Monte Carlo calculations of risk analytics – value-at-risk, potential future exposure, credit valuation adjustment – in intraday risk monitoring, so fast approximations are sometimes preferred. Vladislav…

Quantized calibration in local volatility

Quantization is applied to price vanilla and barrier options

Funding in option pricing: the Black-Scholes framework extended

Wujiang Lou shows the impact of funding costs on option valuation

Heston model: shifting on the volatility surface

Stochastic volatility model combining Heston vol model and CIR++

Cutting edge: Incorporating forex volatility into commodity spread option pricing

Spread option pricing: importance of forex risk factors illustrated

Smile transformation for price prediction

Prediction of arbitrage-free option prices that outperform existing models

Time for a timer

Time for a timer

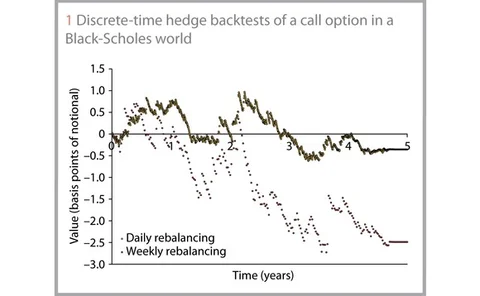

Hedge backtesting for model validation

Hedge backtesting for model validation