Technical paper

Pitfalls and solutions in current risk management methodology

Volume 16, Issue 5 (2014)

Diversifying risk parity

Volume 16, Issue 5 (2014)

Risk evaluation of mortgage-loan portfolios in a low interest rate environment

Volume 16, Issue 5 (2014)

The Bayesian roots of risk balancing

Risk balancing has been considered a heuristic asset allocation method. In this paper, the authors show that, on the contrary, risk balancing is a special case of a utility optimization problem with log regularization that constrains risk concentration.

Risk–return-efficient target-volatility strategies

Volume 3, Issue 3 (2014)

Two centuries of trend following

Volume 3, Issue 3 (2014)

Cutting Edge introduction: The trouble with algorithmic execution

New set-up allows fast, tractable optimisation of trade execution, without neglecting downside risk

Operational risk modelled analytically

Regulators require banks to use an internal model to compute a capital charge for operational risk, which is thought to be sensitive to assumptions on dependence between losses that still remain a matter of debate. Vivien Brunel proposes an analytical…

Optimal execution with a price limiter

Balancing the price uncertainty and price impact of large orders is an important issue for many market participants. While classical approaches lead to trading algorithms that are invariably price-path insensitive, in this article, Sebastian Jaimungal…

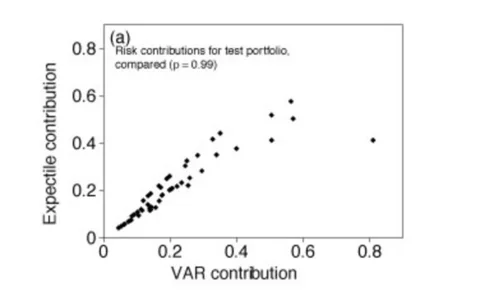

The properties of expectiles explored

Expectiles’ risk contributions are essentially the same as those of expected shortfall

Cutting edge intro: CDOs and the risk of risk aversion

New analysis shows CDOs can withstand high levels of correlation – what they can’t cope with, though, is a sudden change in risk appetite

Expectiles behave as expected

Expectiles' results are analogous to those of value-at-risk and expected shortfall

Credit goes to forward rate spreads

Term structure of interest rates explained with a credit model

Portfolio construction and systematic trading with factor entropy pooling

Portfolio construction and systematic trading with factor entropy pooling

Why CDOs work

Collateralised debt obligations have largely gone under the radar since the 2007 financial meltdown, when their market collapsed. Nearly every attempt at explaining the cause of their failure pointed towards flawed assumptions in pricing models and…

Smile transformation for price prediction

Prediction of arbitrage-free option prices that outperform existing models