Technical paper

Cross-market valuation

This article takes the guesswork out of what credit margin to use when valuing credit-risky derivatives, and also sheds light on how relative value trading and capital structure arbitrage may be analysed quantitatively.

PD estimates for Basel II

One of the main issues banks will have to face to comply with the new Basel II internal ratings-based approach is to prove that the long-run average probabilities of default they assign to their clients, which will be used as the basis for regulatory…

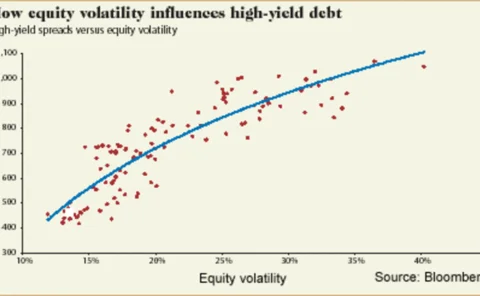

The effect of volatility

market graphics

Monthly snapshot

market data

An integrated framework for the governance of companies

Cases of insolvencies, losses and internal frauds have been increasing of late. As a result, the question is asked more and more often whether such cases could have been avoided with better governance of companies or a clearer organisational handbook. In…

String theory

Awards 2004

Constructing an operational event database

Michael Haubenstock of US bank Capital One outlines a framework for an event database, formulated with current US regulatory guidance on the subject in mind. The text is an abstract from The Basel Handbook, which has just been published by Risk Books.

The score for credit

Jorge Sobehart and Sean Keenan discuss the benefits and limitations of model performance measures for default and credit spread prediction, and highlight several common pitfalls in the model comparison found in the literature and vendor documentation. To…

Unifying volatility models

This article introduces a method for building analytically tractable option pricing models that combine state-dependent volatility, stochastic volatility and jumps. The eigenfunction expansion method is used to add jumps and stochastic volatility to…

Multi-factor adjustment

The author presents an analytical method for calculating portfolio value-at-risk and expected shortfall in the multi-factor Merton framework. This method is essentially an extension of the granularity adjustment technique to a new dimension.

Swap vega in BGM: pitfalls and alternatives

Raoul Pietersz and Antoon PelsserPractitioners who are developing the Libor BGM model for risk management of a swap-based interest rate derivative be warned: for certain volatility functions the estimate of swap vega may be poor. This may occur for time…

The one-year lag

market graphics

How good is your information?

Fraud, opaque accounting practices and incomplete data are unavoidable. Butare they factored into a credit risk forecast? An emerging class of models doesthe job by assuming incomplete information. Barra's Lisa Goldberg explains.

Trading techniques

Rankings 2004

Storage strategies

Rankings 2004

Corridor variance swaps

This article studies a recent variation of a variance swap called a corridor variance swap (CVS). For this swap, returns are not counted in the realised variance calculation if the reference index level is outside some specified corridor. CVSs allow…

What’s a basket worth?

Peter Laurence and Tai-Ho Wang take a significant step in the valuation of basket options with positive and fixed weights. These model all index options, price, cap or equal weighted. Departing from the usual Black-Scholes framework, the authors provide…

Come together

market graphics

Bringing credit portfolio modelling to maturity

Michael Barco shows how to perform mark-to-market credit portfolio modelling by extendingthe well-known saddle-point technique, introducing spread and recovery rate volatility. Hethen tests his results on a fictitious portfolio, showing how asset…