Technical paper

A forward-looking adjustment

Cutting edge: Operational risk

The impact of PD/LGD correlations on credit risk capital

Guido Giese applies econometric estimates of correlations between default rates and loss given default rates to modern credit portfolio models to quantify their impact on the calculation of credit risk capital

Omega portfolio construction

The omega risk-adjusted performance measure with Johnson distributions accountscomprehensively and non-discretionarily for the first potentially persistent moments includingskewness and kurtosis. The Johnson-omega ratio thus overcomes the shortcomings of…

Real option valuation

Emissions trading

Quant analysis by StructuredRetailProducts.com

Quant analysis

NDF

Quant analysis by StructuredRetailProducts.com

Bayerische Landesbank

Quant analysis by StructuredRetailProducts.com

CBA Vita

Quant analysis by StructuredRetailProducts.com

Banco Urquijo

Quant analysis by StructuredRetailProducts.com

The sum of its parts

Germany

Replication of flexi-swaps

Ingmar Evers and Farshid Jamshidian describe a relatively new product known as a flexi-swap and discuss its application in securitisation. A flexi-swap gives a counterparty an option to amortise the interest rate swap at an accelerated pace. They show…

Rating properties and their implications for Basel II capital

Internal ratings

Common interests

Interest rates

La Caixa

Quant analysis by StructuredRetailProducts.com

Sanpaolo IMI Group

Quant analysis by StructuredRetailProducts.com

Quant analysis by StructuredRetailProducts.com

Quant analysis

Barclays

Quant analysis by StructuredRetailProducts.com

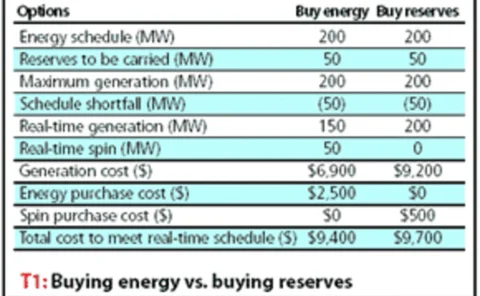

Real-time trading

Rankings 2005