Asia Risk

The development of structured deposits

Chinese regulation

Japanese investors exit PRDC notes

Late-2005 dollar rally against the yen catches some investors out

Asian growth to boost hedge funds

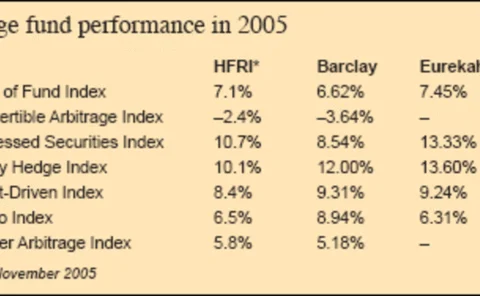

2005 a relatively good year for hedge funds, but convertible arbitrage still down

A new playing field

Chinese regulation

Operational risk - Operational VAR: a closed-form approximation

Klaus Bocker and Claudia Kluppelberg investigate a simple loss-distribution model for operational risk. They show that, when loss data is heavy-tailed (which in practice it is), a simple closed-form approximation for operational value-at-risk (VAR) can…

Future frameworks

Isda update

The call of the Ocean

Profile

Seeking an Accord

Economic capital

Making progress

Basel II

The CDO alternative

Credit CPPI

Investible hedge funds launch

New year launch for invesitble hedge funds trio

The evolution of variance

Variance swaps

Dealing with default

Credit Derivatives

A difficult landscape

Private banking