Swaps data: have SOFR and Sonia swaps and futures lived up to expectations?

Progress on volumes of SOFR and Sonia swaps and futures

In just two years’ time, Libor could cease to exist, casting uncertainty over the fate of financial contracts worth hundreds of trillions of dollars. Alternative risk-free rates (RFRs) have been selected in core markets and have the backing of the official sector, but it’s not so clear whether they have industry backing.

Given the huge significance and reliance on Libor, there are always going to be voices casting doubt on whether these new RFRs will succeed and the start of a new year is a good point in time for such sceptical views to be aired.

Hard data on open interest, outstanding notional and volumes traded for swaps and futures referencing Libor successors such as SOFR, Sonia and €STR provide some perspective on progress to date. So far, it seems to be a mixed bag.

There’s no doubt RFR derivatives volumes have been increasing over the past year, as an eight-fold jump in SOFR futures open interest attests. But in some of the most established RFR markets – for example Sonia swaps – growth has stalled, particularly at the long end. And there’s little sign of a slowdown in Libor-linked swaps activity in tenors past January 2022 – the benchmark’s assumed end date.

As the clock counts down, the switch from Libor to RFR contracts may need to accelerate to embed those rates in the new landscape. The year ahead will be critical, with some pivotal events to watch out for – not least in October, when CME and LCH change their discounting curve from Fed funds to SOFR for all US dollar swaps.

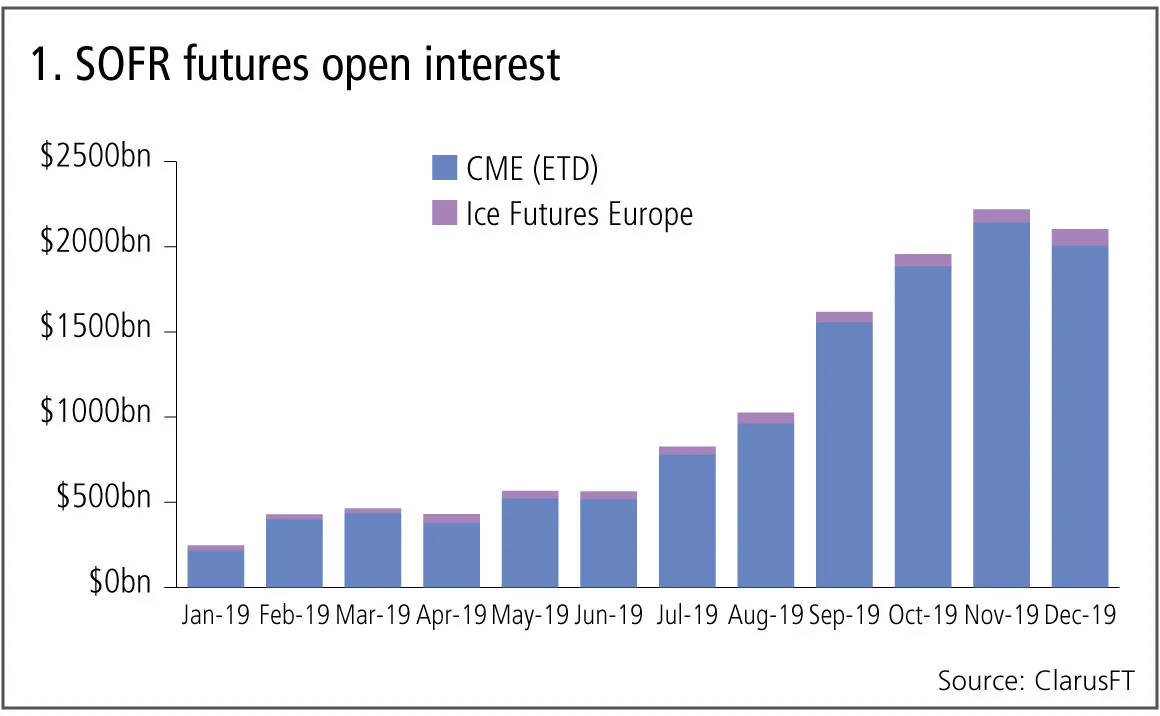

SOFR futures

Let’s start with the largest currency, US dollars and futures on the SOFR index, and chart the growth in open interest over the past year for the CME and Ice futures.

Figure 1 shows:

- As of December 31, 2019, the combined open interest of these two contracts was $2.1 trillion in notional terms, increasing from $250 billion as of January 31, 2019.

- September 2019 was a significant month, and one that has been covered a lot in the press, with disruption in the repo market and the Federal Reserve stepping in to provide liquidity.

- The data shows that October and November trading volumes continued to significantly increase open interest, which hit new peaks.

- CME market share was 95.5% of open interest, Ice had 4.5%.

To put this $2.1 trillion open interest into perspective, we need to compare with the CME Fed funds futures and CME Eurodollar to see whether the ratio of SOFR open interest to each of these is increasing.

The answer to that is an unequivocal yes.

Between January 31, 2019 and December 31, 2019, SOFR futures open interest has increased from 2% to 22% of CME Fed fund futures and from 2% to 19% of CME Eurodollar. Those are significant jumps indeed and augur well for the success of SOFR trading. We wait to see if CME’s launch of options on SOFR futures this month will add another fillip to volumes and open interest.

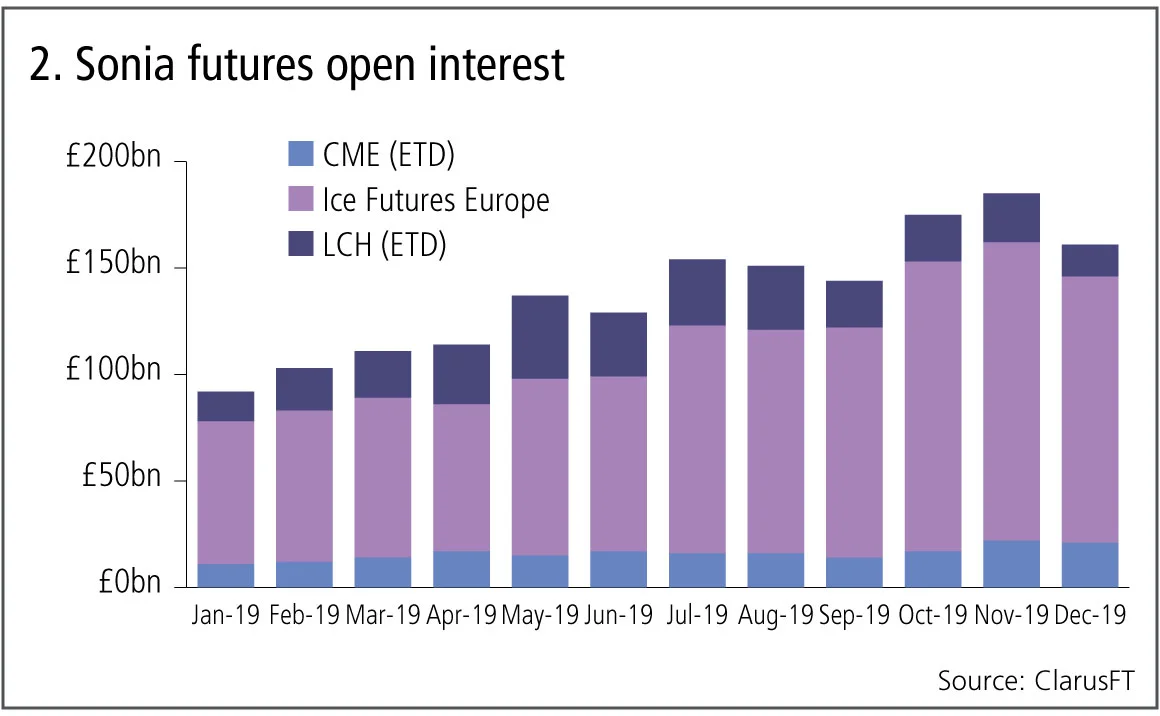

Sonia futures

Next, let’s look at Sonia futures open interest in 2019.

Figure 2 shows:

- Open interest increasing from £91 billion ($118.8 billion) in January to £160 billion in December, an increase of 75%.

- Ice with the largest share, £125 billion or 78% of open interest.

- CME with £21 billion or 13% of open interest.

- LCH, CurveGlobal with £15 billion or 9% of open interest.

We can get a perspective on the £160 billion of Sonia futures open interest by comparing with Ice short sterling and checking if we see a similar increase as evidenced in SOFR.

Between January 31, 2019 and December 31, 2019, Sonia futures open interest has increased from 4.5% to 8.3% of Ice short sterling – so far less than the 20% we saw in SOFR, but evidence of a gain none the less.

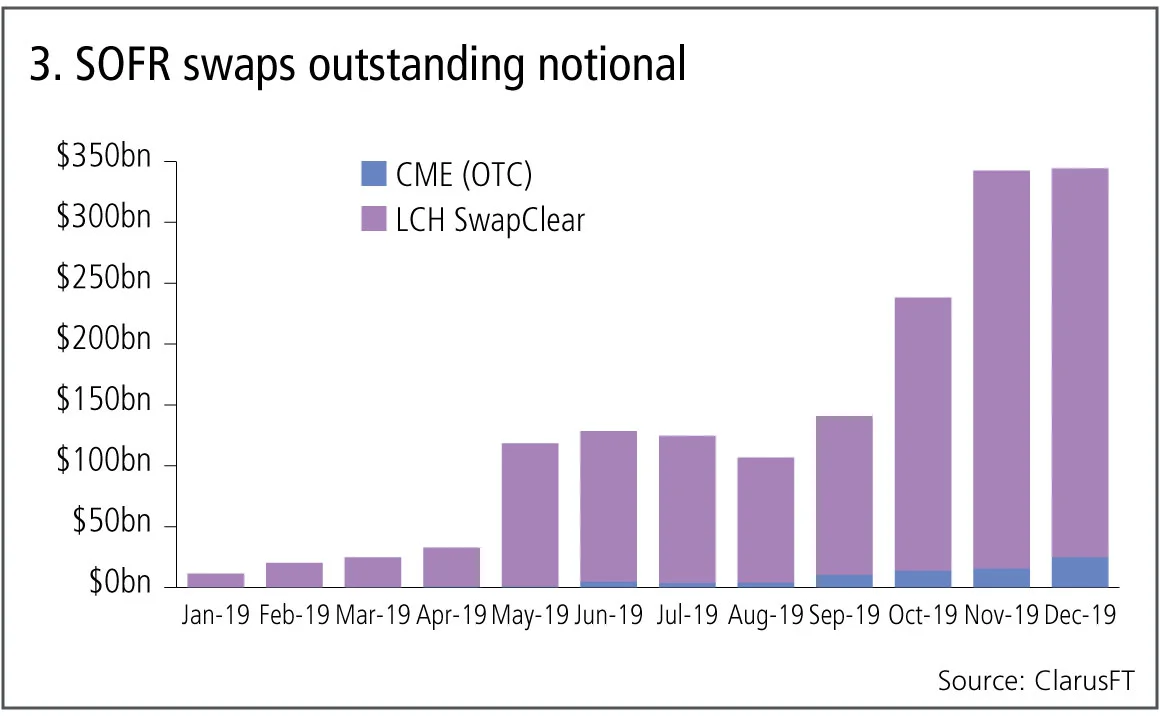

SOFR swaps

Next, let’s look at progress in SOFR swaps trading.

Figure 3 shows:

- Outstanding notional (single-sided) of SOFR swaps at LCH SwapClear and CME over the past year, broken out by month.

- Starting the year at $11 billion and ending at $345 billion, a very respectable increase indeed.

- Large jumps in October and November, meaning that the fourth quarter on 2019 was by far the best quarter in volume growth and it will be interesting to see if the first quarter of 2020 lives up to this rate.

If we follow our futures analogy, we should look to see if the ratio of SOFR swaps outstanding is increasing rapidly compared with Fed funds and Libor swaps.

In this case the jury is still out. As at December 31, 2019, the $345 billion of SOFR swaps notional represents just 3% of Fed fund swaps and 1% of US dollar Libor swaps. The latter ratio of 1% would look even worse if we tenor risk-adjusted the figures as SOFR volume remains dominated by short maturity trades.

It may be that we need to wait until October 2020, the month when CME and LCH change their discounting curve from Fed funds to SOFR, for any real pick-up in volumes.

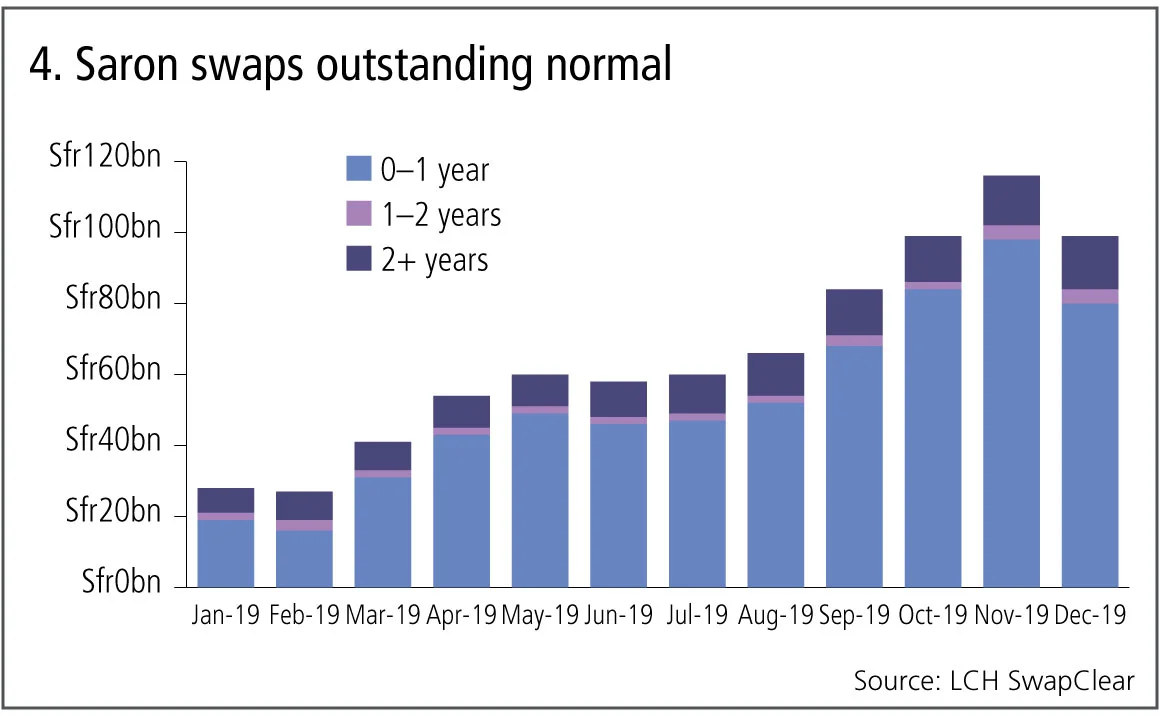

Saron swaps

Next let’s look at swaps in Swiss francs where Saron is the new risk-free rate.

Figure 4 shows:

- Outstanding notional (single-sided) at LCH SwapClear over the past year, split out by the major tenor buckets.

- Total notional increasing from Sfr29 billion ($29.7 billion) on January 31, 2019 to Sfr99 billion on December 2019 – a very decent increase.

- The 0–1 year tenor with the largest increase of 300% from Sfr19 billion to Sfr80 billion, while 2+ year has increased 100% from Sfr7 billion to Sfr15 billion.

And what if we compare Saron OIS swaps to Swiss franc Libor swaps and include volume at CME and Eurex?

On December 31, 2019, that gives us Sfr100 billion Saron to compare with Sfr1 trillion of Libor – a ratio of 10%, and one that has increased from 3.4%, so good progress there, but we need to see more long-term trading in Saron to make a material dent in a risk-adjusted measure.

€STR swaps

€STR is the new risk-free rate in euro markets and while Eonia is now changed to be determined from €STR plus a fixed spread, Eonia swaps continue to trade, but we are now starting to see €STR swaps as well.

I will skip the chart as the data is sparse but LCH SwapClear now has €66 billion ($73.1 billion) of single-sided notional outstanding in €STR swaps from a start in October 2019, while Eonia swaps remain massive with €8 trillion of outstanding notional and Euribor even larger at €25 trillion.

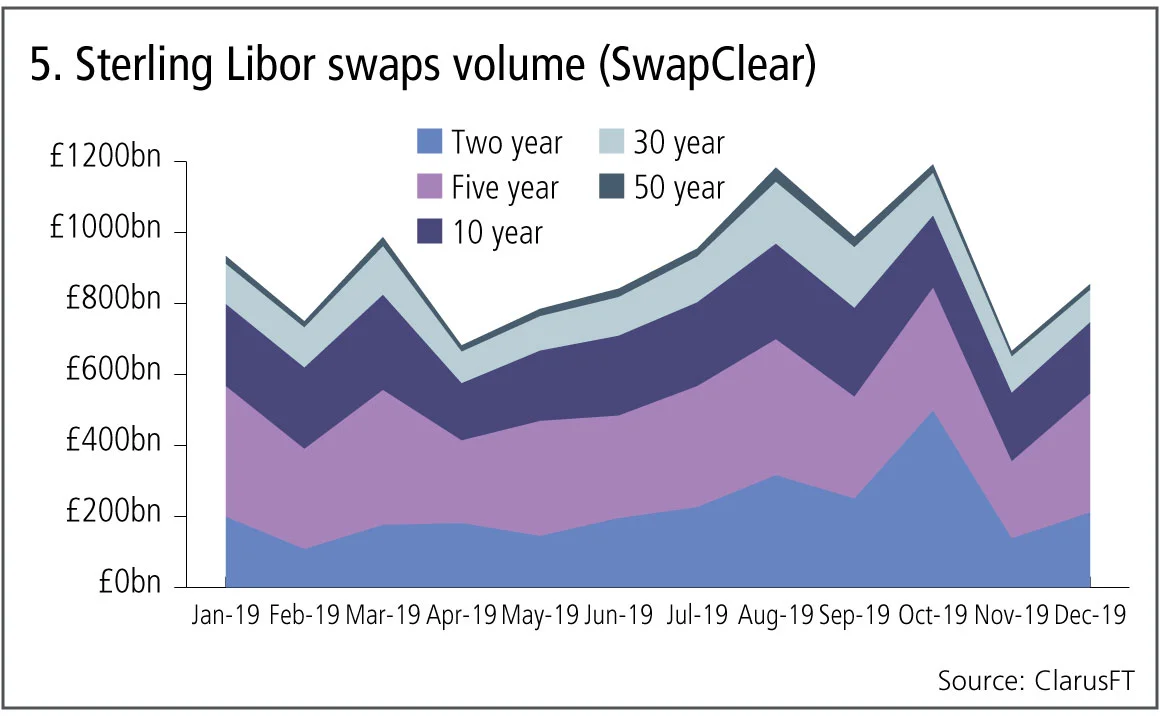

Sterling Libor and Sonia swaps

Finally, let’s turn to sterling, where the existing Sonia rate – after reform – has been selected as the new risk-free rate to replace Libor. The two questions we are most interested in are: first, is swaps volume in Libor decreasing, while Sonia swaps are increasing, and second, are longer tenors trading in Sonia?

Figure 5 shows:

- Monthly gross notional cleared at LCH SwapClear over the past year, split out by the major tenor buckets for Libor swaps.

- Generally the volume trend is up for most of the year and lower volumes in November were to do with market conditions as opposed to any drop in preference for the product.

- The monthly average gross notional in 2019 was £900 billion and December 2019 is close to this figure.

- Open interest ending the year at £5.9 trillion from £5.4 trillion at the start.

So no evidence of a reduction in sterling Libor swaps trading and not even for those with maturity of greater than two years, which would continue past January 2022, the assumed end of Libor.

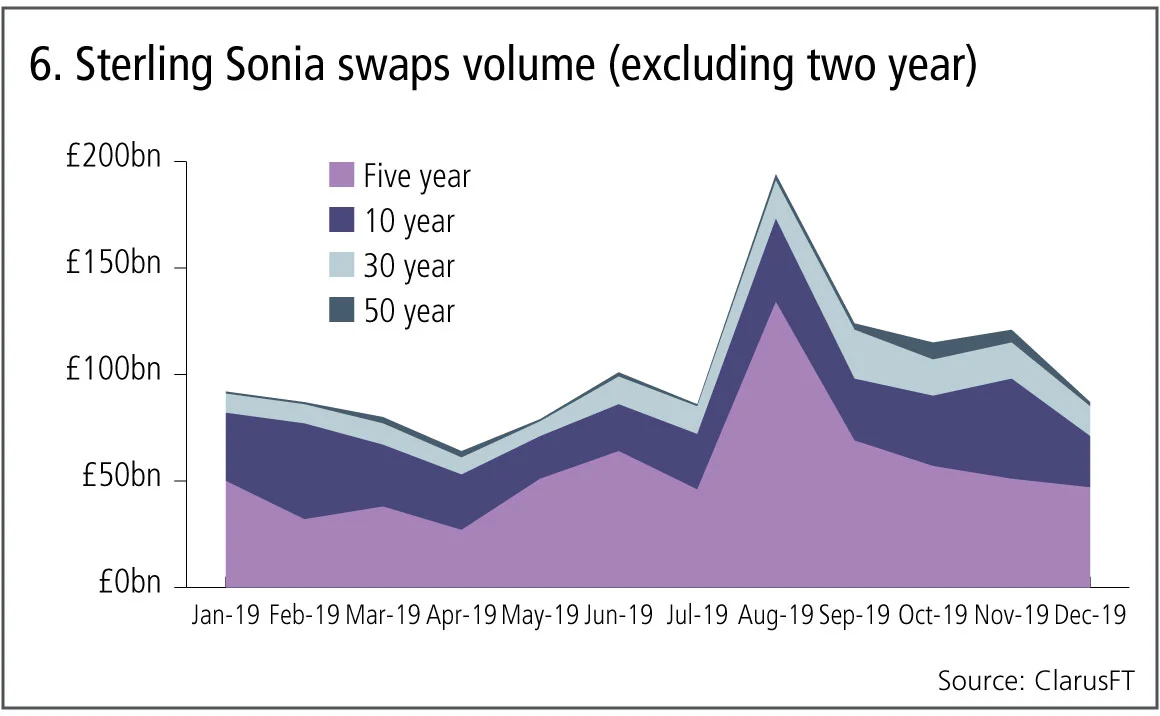

Let’s now chart Sonia swaps volume and, because the below two-years tenor dominates the figures to such an extent, to make the chart useful we will exclude this tenor, otherwise the monthly average of £1.9 trillion in below two years will dominate the total of £100 billion from all other tenors.

Figure 6 shows:

- The significant jump in August 2019 proved to be a false dawn in terms of a ratcheting-up of levels.

- The thin blue line does show a welcome increase in 50 year, but we really need to see five, 10 and 20 year increase greatly.

To summarise, 2019 saw excellent progress in SOFR futures volumes, some progress in SOFR swaps, Sonia futures, Saron and €STR swaps, but little in Sonia swaps. We need to wait and see what 2020 brings.

Amir Khwaja is chief executive of Clarus Financial Technology.

コンテンツを印刷またはコピーできるのは、有料の購読契約を結んでいるユーザー、または法人購読契約の一員であるユーザーのみです。

これらのオプションやその他の購読特典を利用するには、info@risk.net にお問い合わせいただくか、こちらの購読オプションをご覧ください: http://subscriptions.risk.net/subscribe

現在、このコンテンツを印刷することはできません。詳しくはinfo@risk.netまでお問い合わせください。

現在、このコンテンツをコピーすることはできません。詳しくはinfo@risk.netまでお問い合わせください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(ポイント2.4)に記載されているように、印刷は1部のみです。

追加の権利を購入したい場合は、info@risk.netまで電子メールでご連絡ください。

Copyright インフォプロ・デジタル・リミテッド.無断複写・転載を禁じます。

このコンテンツは、当社の記事ツールを使用して共有することができます。当社の利用規約、https://www.infopro-digital.com/terms-and-conditions/subscriptions/(第2.4項)に概説されているように、認定ユーザーは、個人的な使用のために資料のコピーを1部のみ作成することができます。また、2.5項の制限にも従わなければなりません。

追加権利の購入をご希望の場合は、info@risk.netまで電子メールでご連絡ください。

詳細はこちら コメント

市場は未来を非常に歪んだ形で捉えている

ジャン=フィリップ・ブショー氏は、割引のパラダイムはより現実的なものへと適応すべきだと述べています

オペリスクデータ:サイバー攻撃が暗号資産プロトコルを揺るがす

他にも:JPモルガンが投資家の損失をめぐり罰金処分を受けた、Symetraのメソジスト系年金基金をめぐる混乱など。データ提供:ORX News

予測市場は、炭鉱のカナリアのような役割を果たすことがある

リスクの専門家によると、Polymarketなどのプラットフォームにおける契約価格は、リスク管理やヘッジの指標となり得るとのことです

AIエージェントがリスク管理者の課題解決にどう役立つ

シティのリスク専門家は、取引や融資承認に関する構造化データと非構造化データを統合し、リスクに関する単一かつ統一されたビューを構築する自律型AIツールについて概説しました

オペリスク・データ:企業スパイがBBVAに脅威をもたらす

他にも:BofAがエプスタイン氏との関与疑惑で追及されています。また、少数株主がブルックフィールドに異議を唱えています。データ提供:ORX News

AI政治の台頭

MASの顧問であるデビッド・ハードーン氏は、AIを単なる一つの技術として扱うべきではないと述べています

AIリスク管理と能力制御への移行

リスク管理者によると、検証の枠組みを見直すことで、銀行はイノベーションと規制上の要件を両立させ、強固なリスク管理体制を維持することができます

トークン化された商品市場は、経済の円滑な運営に寄与する可能性がある

暗号資産の専門家は、実物資産をブロックチェーンに移行することで、担保に関する摩擦が緩和されると主張しています