Credit data: a tough year for South African financials

Default risk rose steadily for 36 firms during Zuma’s final months of rule, writes Credit Benchmark’s David Carruthers

Cyril Ramaphosa has a lot on his plate. The new South African president succeeded Jacob Zuma on February 15, after allegations of corruption triggered his predecessor’s resignation, and will now have to grapple with the Zuma legacy, severe and spreading water shortages, and entrenched inequality. Unemployment of around 28% is close to a 14-year high.

Accumulating stresses have weighed on the country’s credit rating – it was cut to non-investment grade last year – and are also pushing up probabilities of default (PDs) for South African financials.

The median PD for 36 financial companies remained within a bbb– band throughout 2017, while average PDs were bb+. The gap between the two suggests a small number of very weak names are dragging down the average, but credit quality worsened steadily for both measures. Deterioration was particularly marked during the second and third quarters.

The market’s snap verdict on Ramaphosa’s appointment was positive. The credit outlook depends on whether he can untangle a complex web of problems.

In addition this month, we look at the US equity market and US state pension funds against a backdrop of increasing interest rates, and at the apparent paradox of airline credit data.

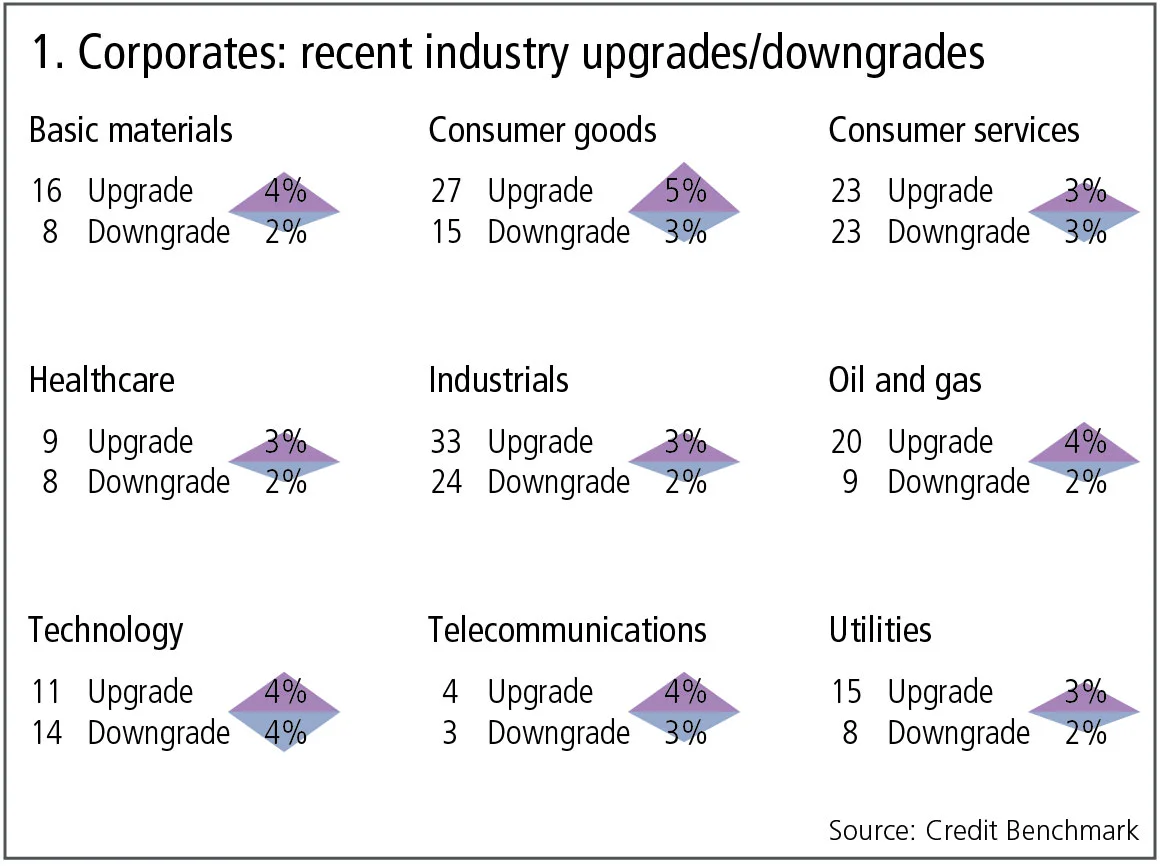

Global credit industry trends

Figure 1 shows industry migration trends for the most recent published data.

Figure 1 shows:

- Global corporates continue to favour upgrades, which dominate downgrades in seven out of nine reported industries.

- Overall, 3% of the global corporates obligors have improved and 2% show a deterioration. Compared with the previous month, the imbalance between upgrades and downgrades has remained stable.

- Basic materials and utilities continue to show a balance in favour of upgrades, continuing the pattern of the past four months.

- Healthcare has moved in favour of upgrades after four consecutive months where downgrades dominated.

- In consumer goods, upgrades now significantly outnumber downgrades for the first time in four months.

- In industrials and oil and gas, upgrades dominate downgrades.

- In telecommunications, upgrades outnumber downgrades for the second month running, after a previous strong bias towards downgrades.

- Technology is the only industry leaning towards downgrades.

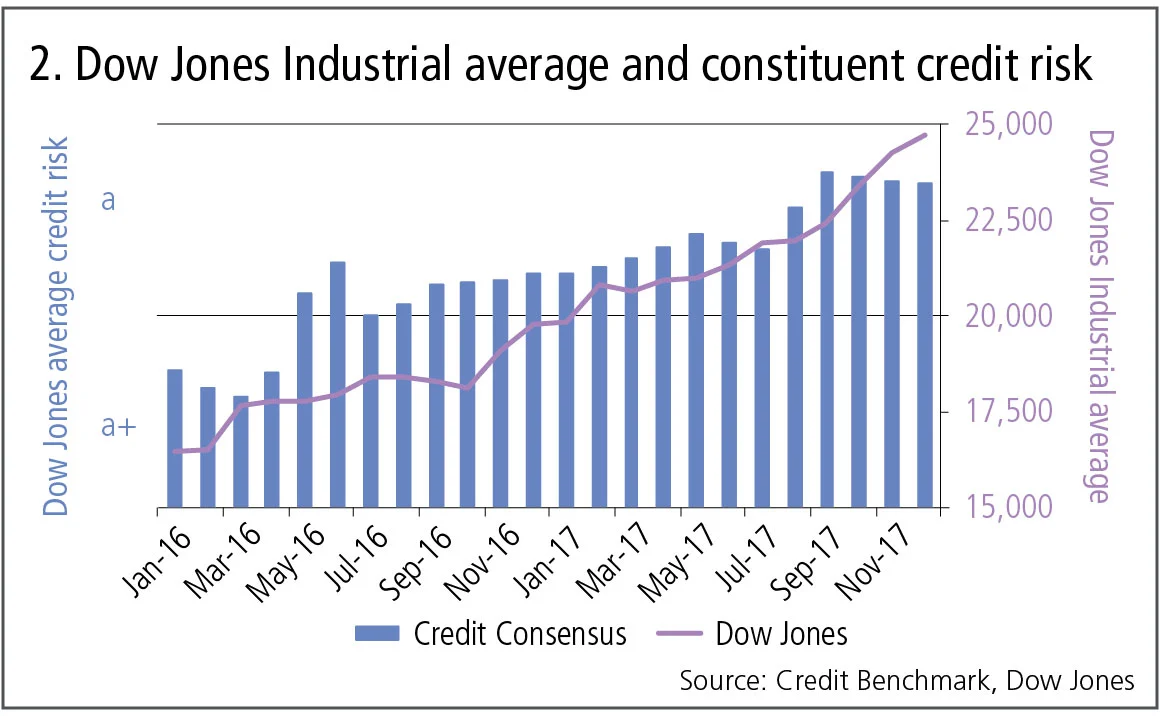

Credit trends for Dow Jones 30 constituents

The bull market in US stocks may have entered a period of heightened volatility and sporadic corrections, but 2017 was a year of almost uninterrupted gains, despite a turning point in interest rates. Trump’s tax cuts are likely to prolong the credit cycle; the impact of this can be seen in figure 2, which compares the Dow Jones Industrials equity index with the credit equivalent based on bank-sourced risk estimates for the Dow Jones constituents.

Figure 2 shows:

- There was a steady increase in the estimated credit risk of US companies until the end of the third quarter of 2017.

- In the fourth quarter – ahead of the Trump tax cuts – the average credit risk showed a modest decline.

- The average credit risk of the Dow Jones Industrial constituents has increased sufficiently that it has been downgraded by a notch.

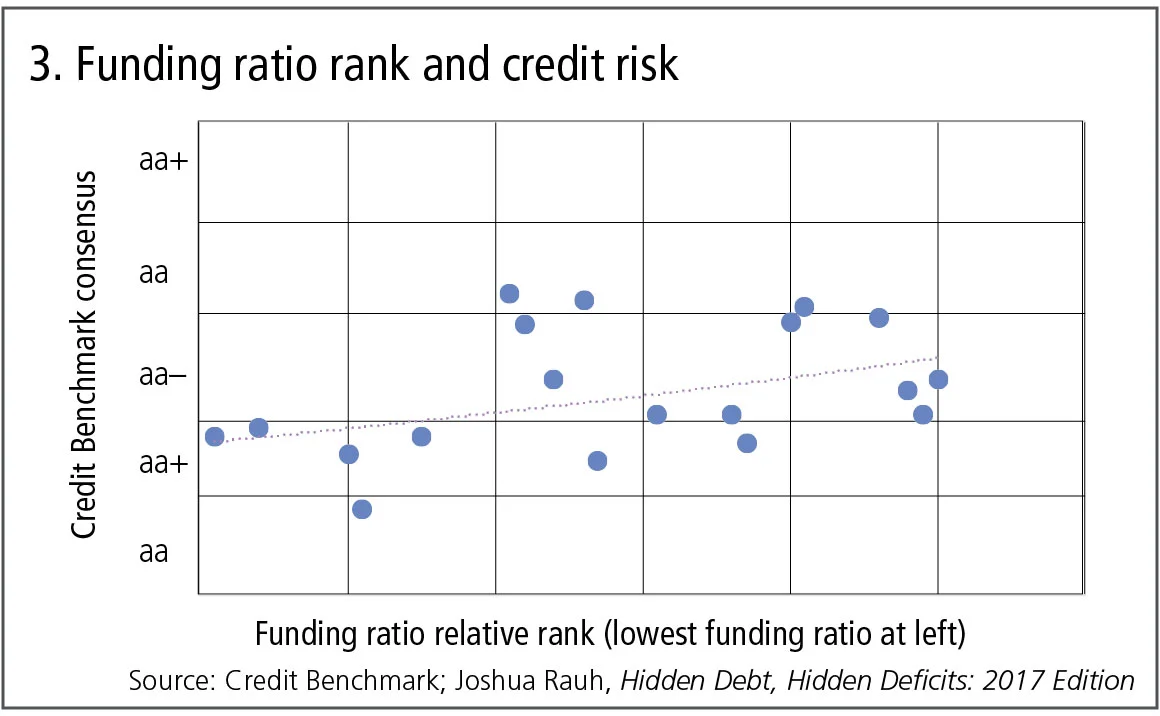

US state pension funds

Pension funds now feature regularly in financial news and have been the catalyst for a number of recent high-profile bankruptcies. Traditional defined benefit pension schemes have suffered from low annuity rates with corresponding record liabilities. Rising long bond yields, underwritten by rising short rates, will ease these problems, but traditional pension funds also face the challenges of increasing life expectancy and lack of new contributions. Corporate pension fund solvency is now a major issue, but there has been less focus on the public sector and the implications of pension deficits for public funding. In 2017, Joshua Rauh of the Hoover Institution published a comprehensive study of US state pension funding. Figure 3 shows the relationship between the ranked funding ratio – total assets divided by total liabilities as measured by market values – and credit risk for 19 of the US state retirement schemes.

Figure 3 shows:

- Credit risks for these 19 schemes show a four-notch range from aa to a.

- The fitted line shows a modestly positive relationship between stronger funding and higher credit consensus, suggesting bank credit analysts are beginning to use funding as an input for credit assessments of US public pension schemes.

- A number of funds show a significant divergence from the fitted line. This may partly reflect the informal implied guarantee that can be attributed to the sponsor state; if a scheme is small relative to the revenue budget of the sponsor state, the effective credit risk may be lower, and vice-versa.

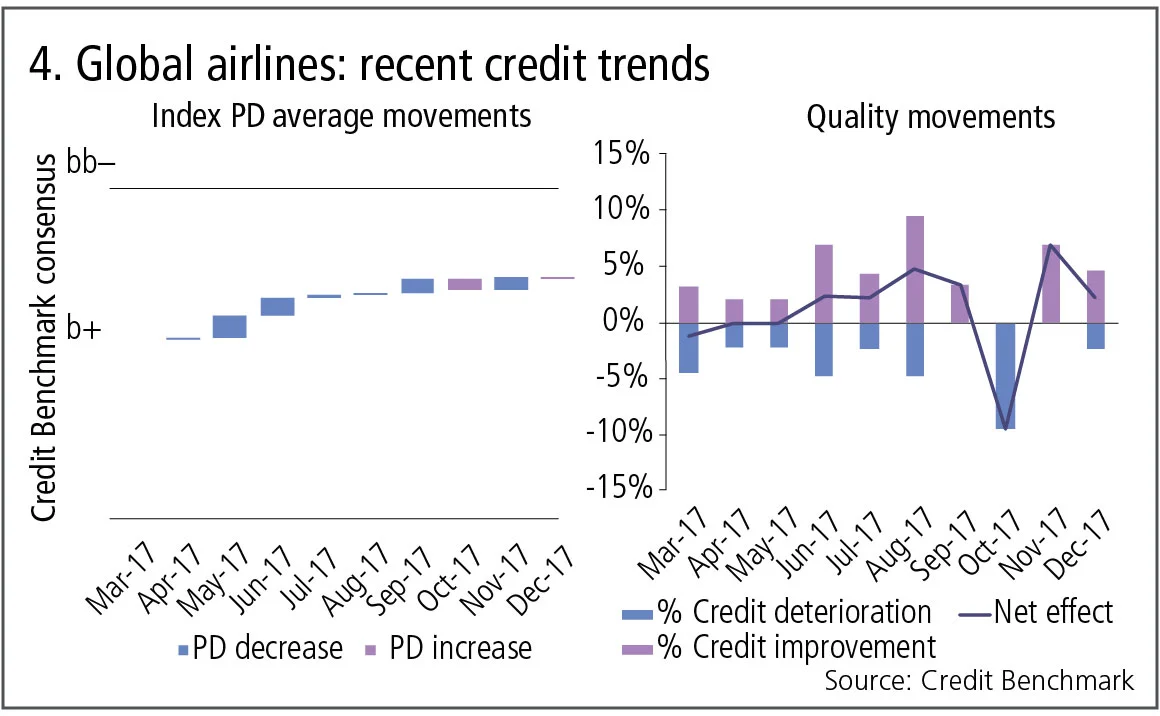

Airlines

The International Air Transport Association reports that 2017 was another good year for airlines and it expects this to continue in 2018. Passenger growth has accelerated and costs have been falling. Some of these positive factors may pause or even reverse – passenger growth is currently outstripping capacity and fuel costs are expected to rise this year. But global secular trends suggest passenger numbers will continue their inexorable rise.

The paradox of the airline industry is that, collectively, it is in good health; but many individual airlines are still typically viewed as high risk due to the typically high default rate of individual airlines.

Figure 4 shows the recent credit trends for global airlines.

Figure 4 shows:

- The left-hand chart shows average credit has improved in most of the past nine months.

- Average credit quality has moved from the b+ range towards bb–, but the rate of improvement has slowed and there have been some slight deteriorations in the past three months.

- The right-hand chart shows this improvement has been broad-based, with material improvements outnumbering material deteriorations in nearly every month, with the noticeable exception of October 2017, which saw a spike in deteriorations.

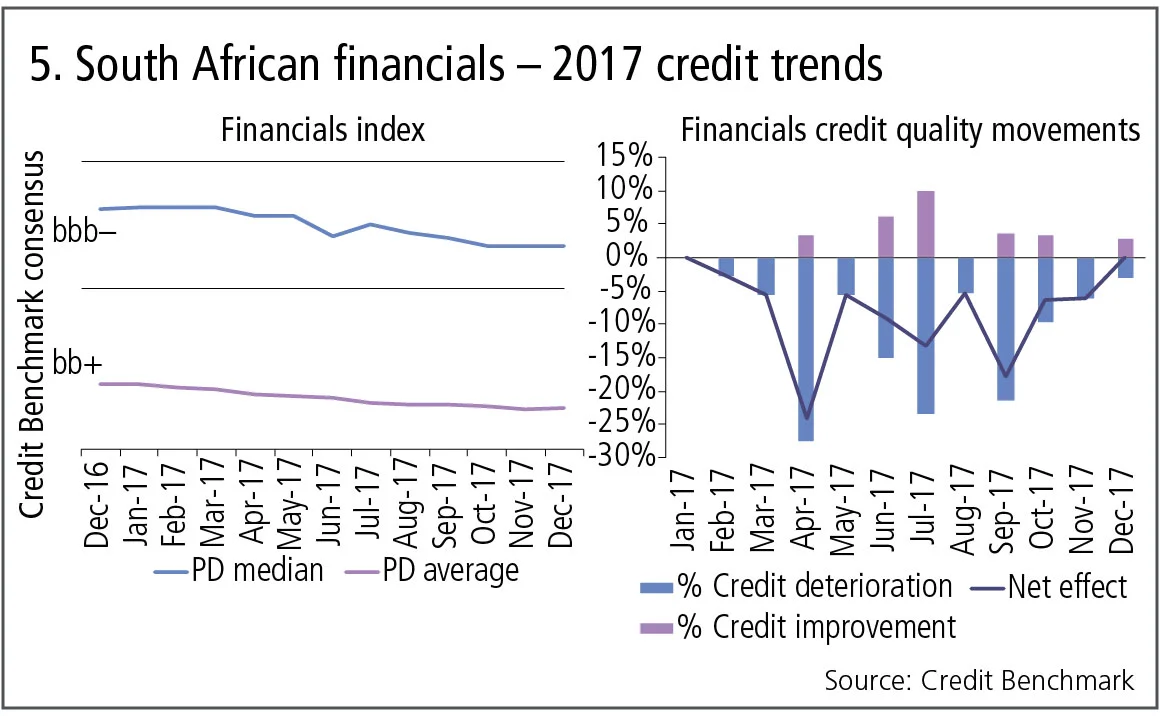

South African financials

South Africa is appearing regularly on the credit radar due to a range of simultaneous challenges. Political tension has led to Zuma’s belated departure, and severe water shortages have highlighted the increasing economic impact of climate change. Standard & Poor’s downgraded South Africa’s local currency sovereign debt to non-investment grade in November 2017; bank-sourced data shows South Africa still hovering just above investment grade, although credit quality deteriorated steadily during the latter half of 2017.

Credit concerns have also affected the financials sector; figure 5 shows the general credit trends for 36 South African financials in 2017.

Figure 5 shows:

- The left-hand chart shows a modest but steady deterioration in the credit quality of South African financials throughout 2017.

- There is a significant difference between the median (in the bbb– zone, ie above investment grade) and the simple average (bb+, and deteriorating) – indicating the distribution of credit risk in the South African financial sector is skewed by a number of higher-risk companies.

- The right-hand chart shows material deteriorations dominated throughout the year, especially in the second and third quarters. This eased in the fourth quarter, suggesting the negative trend may bottom out in 2018.

About this data

The Credit Benchmark dataset is based on internally modelled credit ratings from a pool of contributor banks. These are mapped into a standardised 21-bucket ratings scale, so downgrades and upgrades can be tracked on a monthly basis. Obligors are only included where ratings have been contributed by at least three different banks, yielding a total dataset of roughly 14,500 names, which is growing by 5% per month.

David Carruthers is the head of research at Credit Benchmark, a credit risk data provider.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net

More on Comment

Podcast: Abi-Jaber and Li on a ‘sticky’ volatility problem

The pair discuss their model to jointly capture Vix, SPX and SSR

Markets perceive the future in very distorted ways

Discounting paradigms should adapt to be more realistic, says Jean-Philippe Bouchaud

Op risk data: Cyber hacks shake crypto protocols

Also: JP Morgan fined over investor losses; Symetra’s Methodist pensions mess. Data by ORX News

Prediction markets can be a canary in the coal mine

Prices of contracts on the likes of Polymarket can act as signals for risk management and hedging, says risk expert

How AI agents can join the dots for risk managers

Citi risk expert outlines agentic AI tool that would pull together structured and unstructured data on trading and lending approvals to create single, unified view of risk

Op risk data: Corporate spies spell trouble for BBVA

Also: BofA buttonholed for alleged Epstein links; minority shareholders take a bite of Brookfield. Data by ORX News

The rise of AI politics

AI should not be treated as just another technology, writes MAS adviser David Hardoon

AI risk management and the shift to capability control

By reframing validation, banks can align innovation with regulatory demands and maintain robust risk discipline, argues risk manager