Technical paper/Model risk

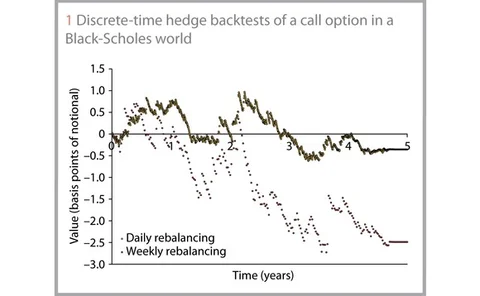

Hedge backtesting for model validation

Hedge backtesting for model validation

Copulas and credit models

Copulas and credit models

Non-linear mixture of asset return models

Non-linear mixture of asset return models

Bayesian lessons for payout structuring

Bayesian lessons for payout structuring

Validating interest rate models under Solvency II

With Solvency II fast approaching, obtaining approval for your internal model is increasingly important. A key part of this process will be to demonstrate the ability of the model’s scenario generation to describe the evolution of interest rates…

Breaking down the model

Brett Humphreys and Andy Dunn outline a method to help energy companies minimise potential model risk and thereby avoid costly errors in valuing deals.