Swaps

Financial institutions move to address funding squeeze in Asia

Funding dilemmas

Despite hurdles, clearers map out forex ambitions

Clearing a way for forex

Energy experts debate merits of speculators and position limits

CFTC and Goldman Sachs executives discuss role of speculators in commodities markets during times of volatility

Despite hurdles, clearers map out forex ambitions

Clearing hurdles

Emir should include exchange-traded derivatives, says Gensler

CFTC chairman says European regulators should expand scope of Emir to include all derivatives, rather than OTC only

Biofuels swaps

Growth industry

Forging an iron ore derivatives market in Asia

Forging a new benchmark

A-share ETF investors to face higher tracking error due to SFC collateral rule change

A new rule from the securities regulator, effective September 12, means some Hong Kong-listed A-share ETFs will have to fully collateralise counterparty risk exposure from their P-note issuers. The move could cause existing investors to rethink their…

US power bodies call for clarity on Dodd-Frank “swap” definition

More guidance is needed from the CFTC on the definition of a swap, according to Ferc and other industry associations concerned about regulatory overlap

Fannie Mae says FHFA's margin rules would drive up hedging costs

US mortgage giant says segregating variation margin will hurt FHFA- and FCA-regulated entities, and create new funding obligations for swap dealers

ECB and World Bank call for exemptions from US derivatives rules

World Bank believes imposition of national regulations on multilateral development institutions is unprecedented intrusion on the internal operations of international organisations

CFTC/SEC swap product definitions 'irrational', say derivatives lawyers

Attorneys criticise the division of regulation and the lack of detail on mixed swaps

Energy experts eye Dodd-Frank tech benefits

Data reporting systems may be far from Dodd-Frank friendly in the energy sector, but experts say users are likely to benefit once they are up and running

Australian regulators suggest clearing exemption for foreign exchange

Reserve Bank of Australia discussion paper commits to harmonising rules with US and Europe

Dodd-Frank extraterritoriality will hurt US banks – Risk.net poll

More than two-thirds of respondents think the long arm of Dodd-Frank will put US banks at a competitive disadvantage

JPM’s Zubrow: US margin rules 'will kill our overseas swaps activities'

US banks will be shut out of the market for uncleared derivatives, says JP Morgan's chief risk officer

General short-rate analytics

Alexandre Antonov and Michael Spector present an analytical approximation of zero-coupon bonds and swaption prices for general short-rate models. The approximation is based on regular and singular expansions with respect to low volatility and contains a…

Challenges ahead for access derivatives in Asian markets

Gateway to Asia

Isda chairman: US banks could be hamstrung by Dodd-Frank

Isda chairman warns House Committee on Agriculture that extraterritorial application of swaps proposals could make US banks less competitive

Energy companies warned on end-user status

Energy Risk USA speakers concerned about reliance on end-user status; urge energy companies to begin Dodd-Frank compliance planning

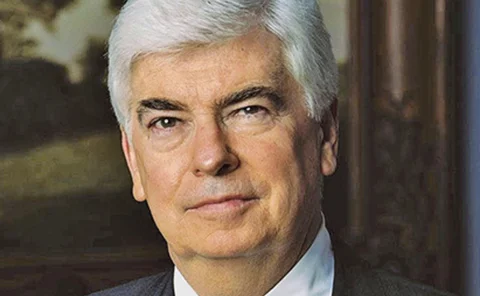

Dodd questions restricting collateral to cash

Co-author of the Dodd-Frank Act shares concerns of energy companies that wish to post non-cash collateral to meet new requirements

European Commission 'unhappy' with Dodd-Frank extraterritoriality

EC official voices concern over the long arm of US derivatives rules