Saddle-point method

Nonparametric estimation of systemic risk via conditional value-at-risk

The authors propose four new nonparametric estimators of static CoVar and compare their performance in simulation studies.

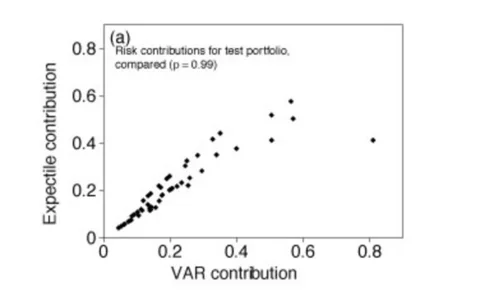

Expectiles behave as expected

Expectiles' results are analogous to those of value-at-risk and expected shortfall

Rational shapes of local volatility

Rational shapes of local volatility

Shortfall: who contributes and how much?

Understanding risk contributions is a key part of successful risk management and portfolio optimisation. Richard Martin extends the discussion from value-at-risk to expected shortfall and shows that saddlepoint approximation preserves the convexity…

The hybrid saddlepoint method for credit portfolios

Anthony Owen, Alistair McLeod and Kevin Thompson derive a practical analytic approach, which they call the hybrid saddlepoint method, to calculate the credit loss distribution for a heterogeneous portfolio of correlated obligors

The saddlepoint method and portfolio optionalities

Richard Martin describes the application of saddlepoint methods to the calculation of tranche payouts and expected shortfall in loss distributions. Aside from computational use in their own right, the resulting formulas motivate a forthcoming discussion…

An indirect view from the saddle

The saddlepoint method has become established as a tool for portfolio analysis. In this article, Richard Martin and Roland Ordovas review the main concepts and show that there are two essentially distinct ways of applying it to conditional independence…

A saddle for complex credit portfolio models

Guido Giese applies the saddle-point approximation to analyse tail losses for very general credit portfolios, including correlated defaults, stochastic recovery rates, and dependency between default probabilities and recovery rates. The numerical…

Bringing credit portfolio modelling to maturity

Michael Barco shows how to perform mark-to-market credit portfolio modelling by extendingthe well-known saddle-point technique, introducing spread and recovery rate volatility. Hethen tests his results on a fictitious portfolio, showing how asset…

Bringing credit portfolio modelling to maturity

Michael Barco shows how to perform mark-to-market credit portfolio modelling by extending the well-known saddle-point technique, introducing spread and recovery rate volatility. He then tests his results on a fictitious portfolio, showing how asset…

Crossing the frontier

Portfolio risk management

Unsystematic credit risk

Although Basel has shifted its treatment of unsystematic credit risk from the first, capital rules pillar (where it was called the 'granularity adjustment') to the second, supervisory pillar of the forthcoming Accord, this issue is of great practical…

Unsystematic credit risk

Although Basel has shifted its treatment of unsystematic credit risk from the first, capital rules pillar (where it was called the ‘granularity adjustment’) to the second, supervisory pillar of the forthcoming Accord, this issue is of great practical…

VAR: who contributes and how much?

Portfolio risk management

Taking to the saddle

Credit portfolio modelling