Derivatives

Brazil’s BM&F in 1999: a central counterparty near-failure case?

The authors argue that, despite some concerns on systemic risk expressed by high-level Banco Central do Brasil officers, the (potential) defaults of Marka and FonteCindam would not have been sufficient to lead BM&F to a failure.

Direct clearing could solve CCP concentration risk

Allowing more clients to self-clear can reduce CCPs’ reliance on a few firms, says ex-Chicago Fed adviser

UK and EU diverge on contractual swap stays

UK scraps pre-resolution stays, while EU regulators could opt for even stricter measures

SA-CCR proves a bitter pill for US banks to swallow

Dealers concerned new regime will punish some business lines with rise in risk-weighted assets

Managing portfolio uncertainty due to the Covid-19 pandemic

For capital market professionals, better understanding the impact of the Covid-19 pandemic on trading and investment portfolios has become even more critical. It’s no easy task to predict market movements and their impact on the profit and loss of a…

Asia edging towards integrated capital markets – SGX’s Loh

Asia Risk 25: full regional co-operation could still be 10 to 15 years away, says Singapore exchange head

CFTC’s Behnam: regulators must be alert to ‘greenwashing’

Risk USA: ESG products that miss sustainability goals may fall foul of customer protection rules

Canada pension fund Hoopp goes cool on bonds

$70bn investor rethinks LDI strategy to take into account paltry yield from fixed income

Mixed response to Esma’s clearing carve-out for optimisation

Long-awaited proposal must be replicated by US and UK to be effective, participants say

Energy Risk Asia Awards 2020: The winners

BNPP wins top derivatives award, with Macquarie scooping environmental products house

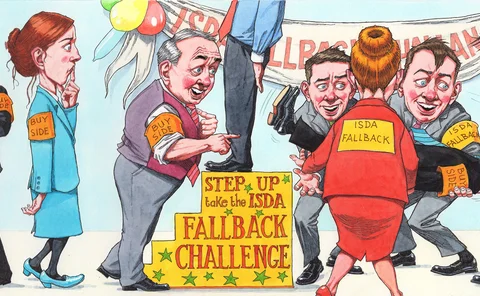

The buy side and Libor: it’s decision time

Investors weigh pros and cons of signing newly released Isda fallback protocol, as Libor demise looms

China structured products could surge after QFII relaxation

Changes to market access scheme allow new hedging methods, but detailed guidelines still pending

Lloyds’ the outlier as UK banks crush CVA charges in Q3

Aggregate CVA RWAs of top five UK banks fell 21%

French rivals BPCE, SocGen see market risks fall in Q3

Market RWAs drop 24% at SocGen quarter on quarter

At UniCredit, XVAs amped trading gains in Q3

Italian bank claimed a €110 million benefit to earnings from valuation adjustments

Jerome Kemp on the skewed economics of clearing

Only Fed intervention prevented “a really big market disaster” during Covid, says derivatives veteran

CFTC’s swap stay plan for clearing houses sparks alarm

Lawyers warn proposal could invalidate close-out netting and expose members to higher risks

Concentration in cleared derivatives: the case for broadening access to direct central counterparty clearing

In this paper, the authors explore the benefits and challenges of encouraging major end-users of derivatives to become direct clearing members of central counterparties (CCPs).

Quants tout alternative carry trades for the ‘new normal’

Low rates and flatlining yield curves leave investors seeking carry in swaps and swaptions

Asic to weigh in on Libor transition conduct risk

Australia’s markets regulator will publish guidance on firms' conduct obligations in move to RFRs

Strengthening supervisory co-operation in derivatives markets

Heath Tarbert and Jon Cunliffe set out a framework for regulating the global derivatives markets

Libor Risk – Quarterly report Q3 2020

The transition away from Libor is littered with ‘chicken and egg’ conundrums. Deep cash markets linked to new risk-free rates (RFRs) require a liquid derivatives market for issuers to hedge exposures, yet RFR derivatives liquidity can only blossom where…

Science friction: some tire of waiting for quantum’s leap

Use cases for new tech are piling up – from CVA to VAR. But so are the obstacles