Infrastructure

Losses and lawsuits

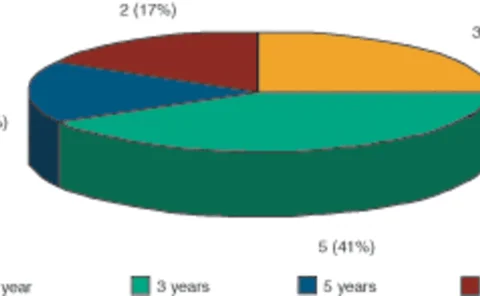

LOSS DATABASE

The Basel II capital accord: op risk proposals in brief

BASEL II UPDATE

UK accepts large banks could use basic op risk approach

BASEL II UPDATE

Letter to the editor: Forbearance measures needed for Basel II

From Tom Wilde, director, risk management, Credit Suisse First Boston

The energy traders’ trader

Danny Masters co-founded a hedge fund to exploit the untapped potential for risk management in the energy market

Volatility dealers’ conundrum

Margins on dollar-denominated swaptions and constant maturity swaps have narrowed sharply. This is great for clients, but dealers are caught in a bind. Gallagher Polyn asks why

Job moves

QUOTE OF THE MONTH: - “An infectious greed seemed to grip much of our business community” Alan Greenspan, on the corporate governance scandals hitting the US Source: Reuters, July 16

Strategic shortcomings

A survey of 13 private banks’ risk management practices reveals some dangerous shortcomings. Lisa Kastigar of Sherwood Alliance, a Switzerland-based financial consulting firm, examines the challenges for risk managers at these institutions

Clearing the obstacles

Credit quality is essential to every energy firm’s success, as recent problems at Aquila and Dynegy attest. Couple this with the post-Enron threat of increased regulation for OTC energy derivatives and it is clear that the energy trading market needs…

From strategy to tactics

Effective tactical use of risk management information has long been an aspiration of many organisations, but technical obstacles have stood in the way. In this third of four articles on integrated credit risk management, David Rowe argues that the…

Running for cover

Energy

The debt dilemma

New angles

Beyond the pail

Basel accord

European banks report decline in equity derivatives volumes

Despite another surge in implied volatility this month, the European equity derivatives business has seen a decline in volumes in 2002, say dealers. Implied volatility on the FTSE reached a high of 39.5% this month, compared with the average daily figure…

Goldman Sachs claims proprietary leap in MBS options pricing

Goldman Sachs claims it has developed a revolutionary new model for pricing mortgage-backed securities (MBS). Alan Brazil, head of mortgage, ABS and rates research at Goldman Sachs in New York, said the new valuation model enables the increasing…

Isda requires CDS reference obligation specification at trade date

The International Swaps and Derivatives Association has decided that confirmations should specify reference obligations as of the trade date for credit default swap (CDS) transactions.

CreditTrade prepares credit volatility pricing tool

Credit derivatives inter-broker dealer and data provider CreditTrade is developing an algorithm to price options on credit default swaps for 20-25 European corporate credits.

Japan Credit Market Update: Spreads track US and Europe wider

Japanese credit default swap spreads were wider this week, tracking the trends in the US and Europe in a generally bear market, traders said.