Technical paper/Model validation

Bayesian analysis in an aggregate loss model: validation of the structure functions

This paper considers the empirical evaluation of a collective risk model with the geometric as the primary distribution and the exponential as the secondary distribution.

The use of the triangular approximation for some complicated risk measurement calculations

The author introduces the triangular approximation to the normal distribution in order to extract closed- and semi-closed-form solutions that are useful in risk measurement calculations.

A practical maturity assessment method for model risk management in banks

This paper proposes a qualitative method to assess the maturity of model risk management practices within banks.

Modeling impacts of stock jumps on real estate investment trust returns with application to value-at-risk

This paper aims to model the impact of extreme stock jumps on REIT returns.

Goodness-of-fit for discrete-choice models of borrower default

This paper demonstrates that the rank-order tests are unreliable for assessing models to be used to predict probabilities.

On modeling zero-inflated insurance data

The authors of this paper use power series distributions to develop a novel and flexible zero-inflated Bayesian methodology.

Testing interest rate models for Solvency II applications

Alexey Botvinnik and Vladimir Ostrovski propose a validation method for interest rate models

Stress testing and model validation: application of the Bayesian approach to a credit risk portfolio

The authors of this paper develop a Bayesian-based credit risk stress-testing methodology.

Comparative analysis of credit risk models for loan portfolios

In this paper, the authors compare credit risk models that are used for loan portfolios, both from a theoretical perspective and via simulation studies.

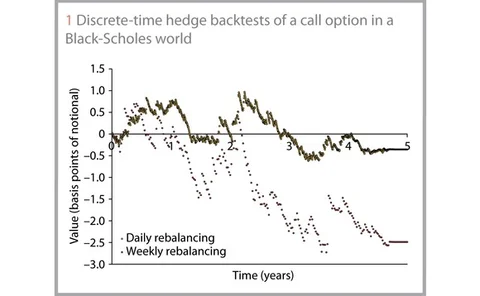

Hedge backtesting for model validation

Hedge backtesting for model validation