Technical paper/Derivatives

Collateral option valuation made easy

Vladimir Sankovich and Qinghua Zhu develop a method to value cheapest-to-deliver option embedded in CSAs

Regulatory and supervisory deference in the context of Australia’s over-the-counter derivative trade reporting and derivative trade repositories regimes

This paper provides an Australian regulatory perspective on the over-the-counter landscape and shows how regulatory deference can play a facilitating role in the cross-border context.

Greeks with continuous adjoints: fast to code, fast to run

Marzio Sala and Vincent Thiery show the derivation of the continuous adjoint problem for PDEs

Multiperiod portfolio selection and Bayesian dynamic models

Kolm and Ritter present a multiperiod, multi-asset selection model with transacion costs, kept computationally tractrable

Short-rate joint-measure models

A joint-measure model combining Q-measure and P-measure

Options for collateral options

Options for collateral options

Local correlation families

Local correlation families

SABR symmetry

SABR symmetry

Differential rates, differential prices

Differential rates, differential prices

Funding strategies, funding costs

Funding strategies, funding costs

Systematic risk factors redefined

Systematic risk factors redefined

Stuck with collateral

Stuck with collateral

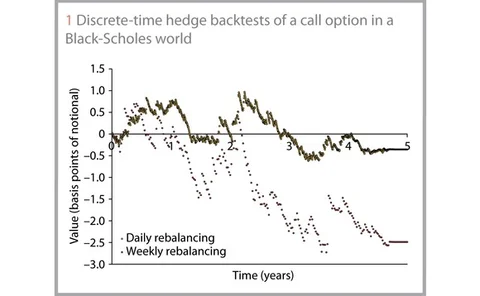

Hedge backtesting for model validation

Hedge backtesting for model validation

Exposure under systemic impact

Exposure under systemic impact

LPI swaps with a smile

LPI swaps with a smile

Bilateral CVA of optional early termination clauses

Bilateral CVA of optional early termination clauses

Breaking break clauses

Breaking break clauses

DVA for assets

DVA for assets

Robust hedging of withdrawal guarantees

Robust hedging of withdrawal guarantees

Wrong-way risk, credit and funding

Wrong-way risk, credit and funding

Rational shapes of local volatility

Rational shapes of local volatility