Risk magazine/Technical paper

Pricing CDSs’ capital relief

Pricing CDSs’ capital relief

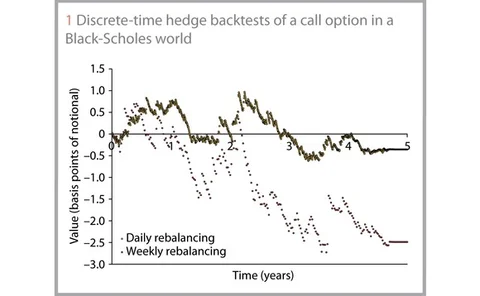

Hedge backtesting for model validation

Hedge backtesting for model validation

Exposure under systemic impact

Exposure under systemic impact

Fast gammas for Bermudan swaptions

Fast gammas for Bermudan swaptions

Cutting Edge introduction: Accuracy or speed?

Accuracy or speed?

Hybrid smiles made fast

Hybrid smiles made fast

SABR spreads its wings

SABR spreads its wings

A quadratic volatility Cheyette model

A quadratic volatility Cheyette model

Smile in the low moments

Smile in the low moments

Cutting Edge introduction: Continuity error

Continuity error

SABR goes normal

SABR goes normal

Lois: credit and liquidity

Lois: credit and liquidity

Cutting Edge introduction: The collateral currency convexity problem

The collateral currency convexity conundrum

Collateral convexity complexity

Collateral convexity complexity

LPI swaps with a smile

LPI swaps with a smile

Cutting Edge introduction: CVA for CDSs

Counterparty risk is generally thought of at a portfolio level, but understanding how a particular payout interacts with credit and debit valuation adjustments could help banks make business decisions. Laurie Carver introduces this month’s technical…

CDSs, CVA and DVA – a structural approach

CDSs, CVA and DVA – a structural approach

Breaking break clauses

Breaking break clauses

Cutting Edge introduction: Wrong-way risk and the limits of correlation

Traditional models for wrong-way risk focus on the correlation between default and exposure – a blunt tool for a tail risk. Alternatives are thin on the ground, but a scenario-based approach may provide some fresh insight. Laurie Carver introduces this…

Robust hedging of withdrawal guarantees

Robust hedging of withdrawal guarantees

Wrong-way risk, credit and funding

Wrong-way risk, credit and funding

Cutting Edge introduction: Goodwill for DVA

Goodwill blunting

Rational shapes of local volatility

Rational shapes of local volatility