Energy Risk/Technical paper

Counterparty risk

Energy Risk Annual Awards

Real option valuation

Emissions trading

The sum of its parts

Germany

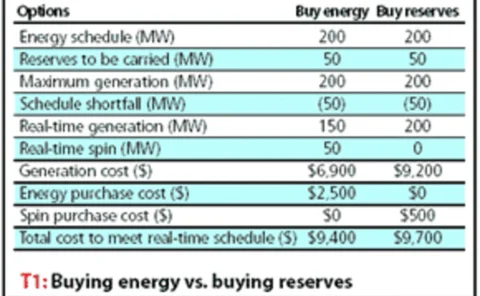

Real-time trading

Rankings 2005

Caring competition

What are the theoretical consequences of restructuring electricity markets on emissions? Here, Benoît Sévi shows that changes in supply and consumption and restructuring for competition has environmental effects, and argues that strong public policies…

Ex-citations

Oil

Earnings at risk

The structure of a typical energy portfolio often contains a different assetand contract mix from the simple derivatives instruments in a more standard portfolio.This requires a different approach to risk. Here, Les Clewlow and ChrisStrickland make the…

A decent exposure

Weather risk

Getting physical

Technology

Covering all the bases

Natural Gas

A history lesson

Abstract: The size of bid/ask spreads in electricity options has both valuationand credit implications. Here, Ted Kury of The Energy Authority shows how toderive theoretical spreads using historical option price data so they can beused as liquidity…

The matrix

Abstract: Portfolio-wide risk management requires a model that accounts correctlyfor the volatility of, and the correlations between electricity forward products.In this paper Kjersti Aas and KjetilK°aresen discuss a joint model for electricityforward…

String theory

Awards 2004

Trading techniques

Rankings 2004

Storage strategies

Rankings 2004

’Tis the season...

Abstract: Aurelian Tröndle presents a general framework for modelling prices of storable and non-storableenergy assets, which sheds light on different market fundamentals, and showshow energy market volatility is seasonal and anything but stable. The…

Dissecting risk

New frontiers

Operational and market risks of a regulated power utility

Victor Dvortsov and Ken Dragoon present an analytical method for including market and operational risks when estimating utility portfolio value-at-risk

Both sides of the fence: a statistical and regulatory view of electricity risk

Ernst Eberlein and Gerhard Stahl analyse price series of 25 energy spot rates simultaneously using Lévy models. This model class allows the capture of stochastic behaviour of these financial instruments. The implications of this analysis will form the…

Valuing exploration and production projects

Lukens Energy Group’s Hugh Li sets out an option method for valuing exploration and production projects, using a practical example

Backwardation and contango change indicators for seasonal commodities

In the first part of this two-part article, Svetlana Borovkova introduced two indicators for detecting changes between backwardation and contango market states. Here, in the second part, she applies the indicators to seasonal commodities and introduces a…

Detecting market transitions: from backwardation to contango and back

Svetlana Borovkova looks at detecting market transitions between backwardation and contango states using the forward curve. In this first part of a two-part article, she introduces two change indicators, which she applies to oil futures prices. Next…