Credit risk

Protecting your own

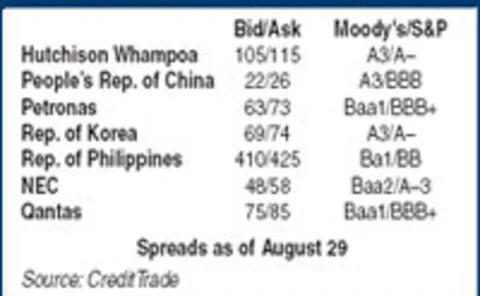

Alstom

News in brief

New angles

Credit Crunch!

clive horwood

Credit due

commentary

A Nordic niche for CLS

Liquidity risk

Early days for indexes

Credit indexes

Unexpected recovery risk

For credit portfolio managers, the priority is to properly incorporate recovery rates into existingmodels. Here, Michael Pykhtin improves upon earlier approaches, allowing recovery rates todepend on the idiosyncratic part of a borrower's asset return, in…

Ultimate recoveries

Measuring recovery using the ultimate rate observed at emergence from bankruptcy may be conceptually desirable, but modelling it is difficult.

Ready and waiting

The Australian Prudential Regulation Authority is confident that the country's financial institutions are well placed for the implementation of Basel II, and expects the four largest banks to implement the advanced IRB approach.

A false sense of security

Credit portfolio models often assume that recovery rates are independent of default probabilities. Here, Jon Frye presents empirical evidence showing that such assumptions are wrong. Using US historical default data, he shows that not only are recovery…

Sponsor's article > The operational risk pyramid

The extremely heterogeneous character of operational risk often makes discussion of it appear fragmented and unstructured. David Rowe proposes one possible paradigm for organising our thinking on various aspects of this increasingly important topic.

Does CP3 get it right?

The Basel Committee on Banking Supervision's third consultative paper raises several complex issues, not least of which is: will it work in practice?

JP Morgan and Morgan Stanley launch Tracx emerging markets

JP Morgan Chase and Morgan Stanley have launched the Tracx Emerging Markets (Tracx EM) index, the latest addition to the Tacx global suite of credit default swap (CDS) indexes created by the two US financial services firms.

Ultimate recoveries

Measuring recovery using the ultimate rate observed at emergence from bankruptcy may be conceptually desirable, but modelling it is difficult. Craig Friedman and Sven Sandow tackle the problem by maximising the creditor’s utility function, constructed…

A false sense of security

Credit portfolio models often assume that recovery rates are independent of defaultprobabilities. Here, Jon Frye presents empirical evidence showing that such assumptions arewrong. Using US historical default data, he shows that not only are recovery…

Unexpected recovery risk

For credit portfolio managers, the priority is to properly incorporate recovery rates into existing models. Here, Michael Pykhtin improves upon earlier approaches, allowing recovery rates to depend on the idiosyncratic part of a borrower’s asset return,…

Retail credit innovations

Credit derivatives

Ready and waiting

Basel Accord

Isda and BMA propose 35% charge for restructuring risk

The International Swaps and Derivatives Association (Isda) and the Bond Market Association (BMA) submitted a comment letter today to the Basel Committee on Banking Supervision in which they argued that, for the sake of capital calculations, loans hedged…

The cutting hedge

Loan hedging

Does CP3 get it right?

Basel II

US credit default swaps and CLN markets recovering, says S&P

The US credit default swaps (CDS) and credit-linked notes (CLN) markets are recovering from a lull in activity, according to rating agency Standard & Poor’s (S&P).

A false sense of security

Recovery rates - Cutting edge

Ultimate recoveries

Recovery rates - Cutting edge