Risk magazine - Volume20/No10

Articles in this issue

No silver bullet

The emergence of contingent credit default swaps has presented banks with a new way to manage their counterparty credit exposures. However, they have important limitations, argues David Rowe

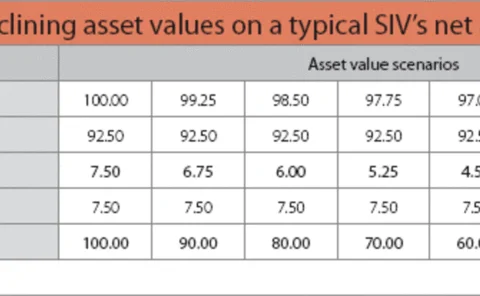

Leaking like a SIV

Structured Finance

Single measures are not enough

Ashish Dev considers the contemporary relevance of three Risk articles from 2002-03

Carry on trading

Structured products

Italian unease

Italy

Algorithmic investment strategies

Sponsored Statement

Building through selling

Real estate

The OTC ambassador

Isda's deputy chief executive, George Handjinicolaou, talks to Alexander Campbell

The risk of one

Fund Derivatives

Capitol mortgage ideas

Government-sponsored Entities

Quants' tail of woe

Liquidations of large quantitative equity portfolios prompted widespread misfiring of hitherto robust quant models. Historically unusual returns volatility and multi-billion-dollar mark-to-market losses ensued. Leading hedge fund managers talk to Jayne…

Economic capital ideas

This month sees the start of Charles Smithson's fourth series of Class Notes, which will run in alternate issues of Risk through the remainder of this year and into 2008. Class Notes is an educational series, designed to pull together the threads of…

Gamma process dynamic modelling of credit

The existing generation of credit derivatives models is unsatisfactory because they generally contain arbitrage, cannot describe the dynamics of the process, and are hard to extend beyond vanilla products. Martin Baxter has created a new tractable family…

Not stressed enough

Stress Testing

Uncertain dividends

Dividend Swaps

Investment solution duo

Sponsored Statement

The benefits of 130/30 vision

Equity funds

Credit's worthy start

Credit Portfolio Management

More than a retail tale

Profile

Riding the M&A wave

Corporates

Equity derivatives – a 'new' old volatility regime?

Sponsored Statement

Investing in company directors' insight

Sponsored Statement

Parisian barrier option applied to convertible bonds

Sponsored Statement

A risk unspoken

Structured products

The ups and downs

Exotic products

Modelling South African swap spreads

Sponsored Statement

An unusual existence

Exchanges