Credit markets

Introducing CCOs

product launch

Sunil Hirani

q&a

Innovation and integration

Profile

Balancing currency and credit risk

Contingency swaps

German banks get to grips with a new lending reality

Removal of state guarantees and pressure from shareholders for better returns means German banks can no longer churn out uneconomically priced loans to clients. Now they are starting to introduce sophisticated loan pricing systems, writes Duncan Wood

Markit signs up 50th Red customer

Markit has signed its fiftieth customer to its reference entity database (Red) for credit instruments. The move means the St Albans-based company has signed up 35 additional clients to Red from its base of 15 institutions in January 2004.

From Basel II to Basel III

Financial institutions face major challenges in modelling credit portfolio risk, particularly in the field of CDOs. Walter Schulte-Herbrüggen and Gernot Becker argue that the main challenge will be in model testing, due to the increasingly customised…

DDQ re-issues commodity-linked structured product

Dawnay Day Quantum (DDQ), a division of London-based financial services and property investment company Dawnay Day, has re-issued its commodity-linked structured product aimed at both the institutional and retail markets.

The importance of ALM

The crossfire between the International Accounting Standards Board and the European Commission seems to have left corporates bewildered about the implications of IAS 39. Risk talks to leading advisory groups and corporates about the challenges ahead, and…

Front Capital wins $5 billion hedge fund client

KBC Alternative Investment Management (KBC AIM), a hedge fund subsidiary of Belgium's KBC Bank and Insurance Group that manages more than $5 billion in assets, plans to implement Front Capital's Arena trading, risk management and distribution system.

Structured finance ratings given BIS OK

The structured finance ratings business was given a clean bill of health today by the Bank for International Settlements (BIS), with a few caveats.

Barclays Capital wins derivatives house of the year in 2005 Risk Awards

Barclays Capital, the UK-based investment bank, scooped the prestigious Derivatives House of the Year Award in Risk magazine’s sixth awards for achievement in risk management.

HSH takes a long-term view

Company profile

Market models for CDS

In August 2004, Risk published an article on the pricing of credit default swap (CDS) options entitled A measure of survival by Phillip Schönbucher. Here, Damiano Brigo provides an alternative derivation of the CDS option pricing formula based on Cox

From Basel II to Basel III

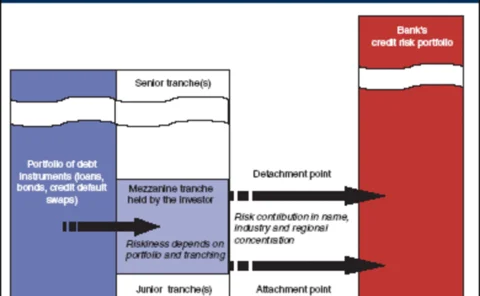

Portfolio risk

Credit risk

Introduction

Forex appeal

Foreign exchange

Bridging the gas gap

Emission trading

A new breed of bond

Emissions trading

High-yield CDS Building liquidity

credit default swap market

ABB’s asbestos risk

news