This article was paid for by a contributing third party.More Information.

Macroeconomic exposures of style indexes: what you don’t know could hurt you

Melissa Brown, managing director of applied research at Qontigo, reveals how changes in the macroeconomic environment can influence portfolio risk across a range of investing styles

About Eurex

Eurex offers futures covering cash equity factors in the US and European equity markets. The offering is based on Qontigo’s Stoxx Industry Neutral Ax Factor Indexes suite and comprises futures based on the five standard factors: value, momentum, low-risk, quality and size. An additional multifactor future, which combines the five exposures in one product, is also included.

Product specifications for the futures follow the well-known standards already in place for Eurex’s benchmark derivatives such as the Stoxx Europe 600 Index Futures.

The benefits of a strict rules-based approach to the construction of style-based portfolios are well known. Portfolios are constructed to tilt on factors with proven track records of driving outperformance, and often-wrong emotions that can drive stock selection decisions are absent. The approach remains the same throughout market and economic cycles, and this consistency is an advantage in producing strong risk-adjusted returns.

While style-based managers may not incorporate a top-down economic outlook into the portfolio construction, the macro environment will drive portfolio risk and therefore impact return. The degree of economic risk seen varies widely per chosen style and may be mitigated to a small or large extent, depending on the factor, by restricting industry exposures.

A multifactor approach is a time-honoured method of diversifying across compensated factors, improving a portfolio’s risk-return trade-off. It has less macro risk than some single-factor styles, but more macro risk than others and, on its own, is not a reliable way to reduce macroeconomic exposure. However, a side benefit of a multifactor approach that also restricts industry exposures is that the resulting portfolio tends to have little exposure to economic forces.

Even if a manager does not consider the economic environment when constructing a portfolio or index from the bottom up, it can be helpful to know about the inherent risks – especially in times of economic upheaval.

With this in mind, Eurex used Axioma’s macroeconomic projection model to evaluate several Stoxx single- and multifactor style indexes – factor-based, industry-neutral and equity factor – to illustrate the degree of economic exposure a manager might experience. This model projects 14 daily traded economic factors, such as term spreads, credit spreads and break-even inflation in several major economies (the US, the European Union, the UK and Japan), along with oil, non-oil commodities, gold and carbon emissions futures onto a standard fundamental factor risk model, separating return into that from the economic factors and the residual of the standard style, industry, country and market factors. The total and active risk expectations produced by this model are the same as those from the fundamental model, only the distribution of that risk varies.

Macro variables can be correlated with industry, country and style factors, some more significant than others

Some of the relationships between economic variables and model factors are to be expected: energy stocks and some country returns (such as Norway) are highly related to oil prices, financial stocks are related to changes in term spreads, and so on. Some style factors are closely tied to economic factors as well. For example, Axioma’s market sensitivity factor is highly correlated with term spreads.

This means what a manager may view as risk and return coming from market sensitivity is actually a result of portfolio exposures to interest rate variables, with some left over (or residual) coming from the style factor.

Some style indexes have more economic exposure than others

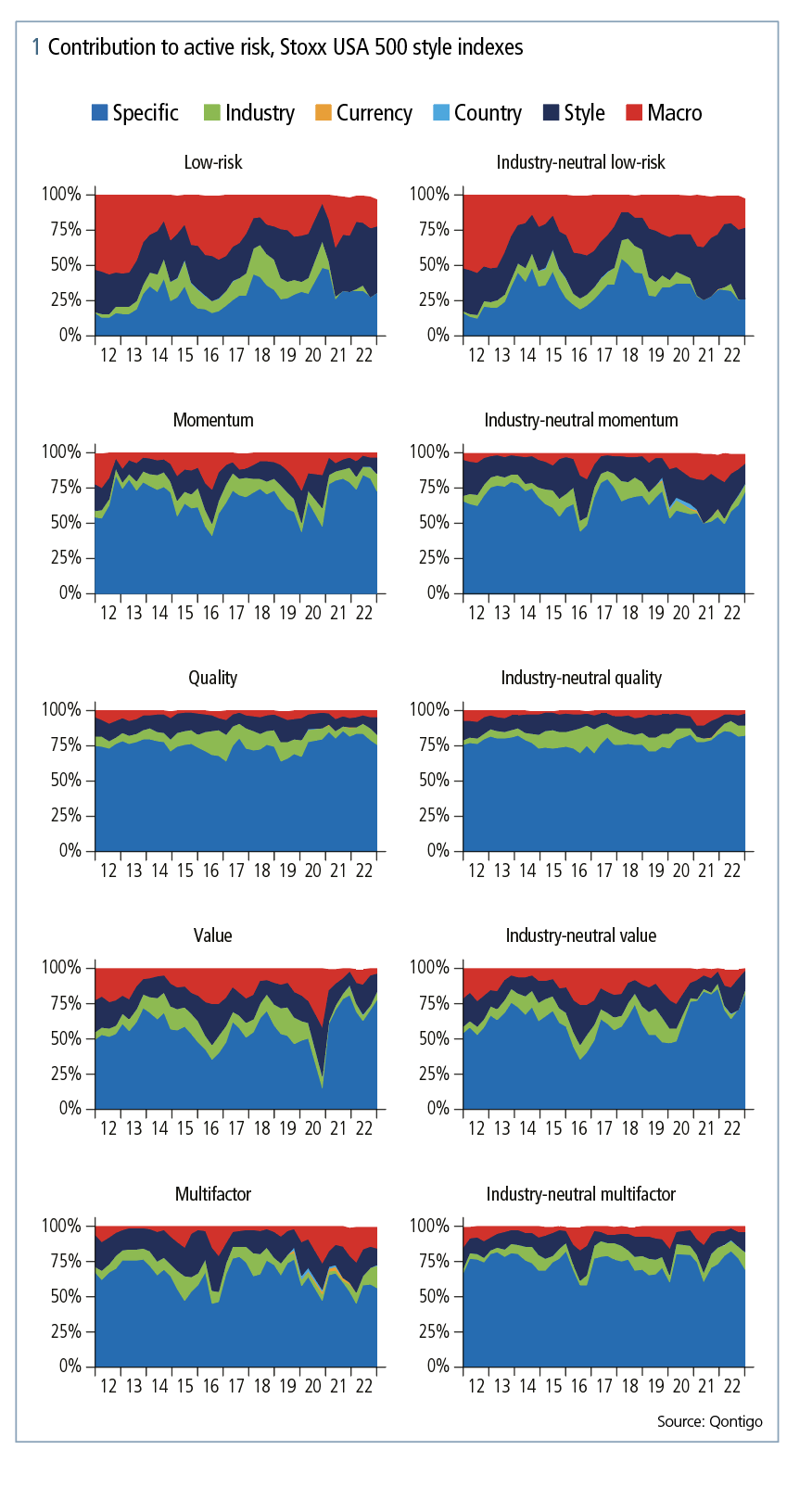

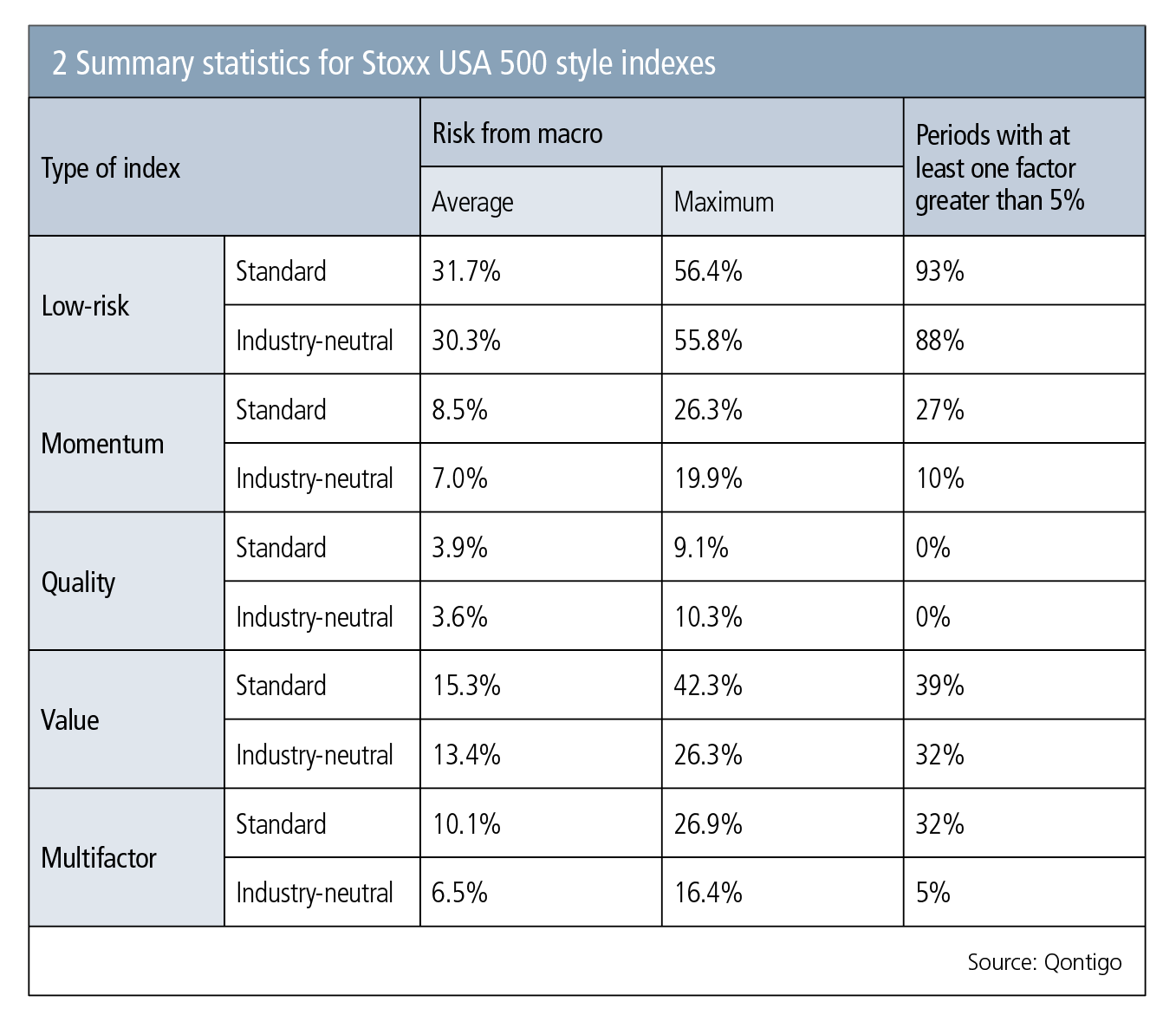

There are two versions of Stoxx style indexes: one that tightly constrains exposures to industry classification benchmark designations, and one that has less strict industry controls. Figure 1 presents the breakdown of risk over the past 10 years for selected style indexes built from the Stoxx USA 500 parent index according to the macroeconomic model, and compares the ‘standard’ version with one that has stricter industry-neutrality rules.1 Risk is calculated at each quarterly rebalance over the past 10 years. Figure 2 details some summary statistics.

Both versions of the low-risk index, which tilts on lower beta and lower volatility stocks, clearly have the most macroeconomic exposure among this set of indexes, with an average of more than 30% of the risk coming from these exposures for both standard and industry-neutral, and a maximum of about 56% (see the red shaded portions of figure 1).

High exposure to macro factors was consistent as well: we calculated the percentage of periods in which at least one individual macro factor accounted for 5% or more of the overall risk, and this was the case in 93% of the periods for the standard index and 88% for the industry-neutral index. In most periods, more than one factor contributed more than 5% of the risk, but this was not the case for the other style indexes.

Quality – which tilts on high-profitability and low-leverage names – fell at the opposite end of the macro risk spectrum, with an average contribution from macro factors of 3.6–3.9% and a maximum of approximately 10%. There were no periods for either version in which any factor contributed more than 5%. This suggests these indexes were much less vulnerable to changes in the economic environment compared with others.

Momentum fell between those two extremes, with 7–8.5% of risk, on average, coming from macro factors. The contribution reached as high as 26.3% for the standard version, although was only about 20% with industry constraints.

Value had at least one macro factor contributing significantly to its risk more often than the other indexes (except low-risk). While the average macro contribution was only 13.4–15.3%, it reached as high as 42% in the standard index, but only 26.3% when industry exposures were constrained.

Finally, the standard multifactor index averaged about 10% of its risk coming from macroeconomic factors, although it reached as high as about 27%. At least one individual factor accounted for 5% or more of the risk in about one-third of the periods. The impact of industry neutrality was bigger for multifactor indexes than any of the single-factor indexes, dropping the average risk contribution to 6.5%, the maximum to 16.4% and the number of periods in which the 5% threshold was exceeded by one factor to just 5%.

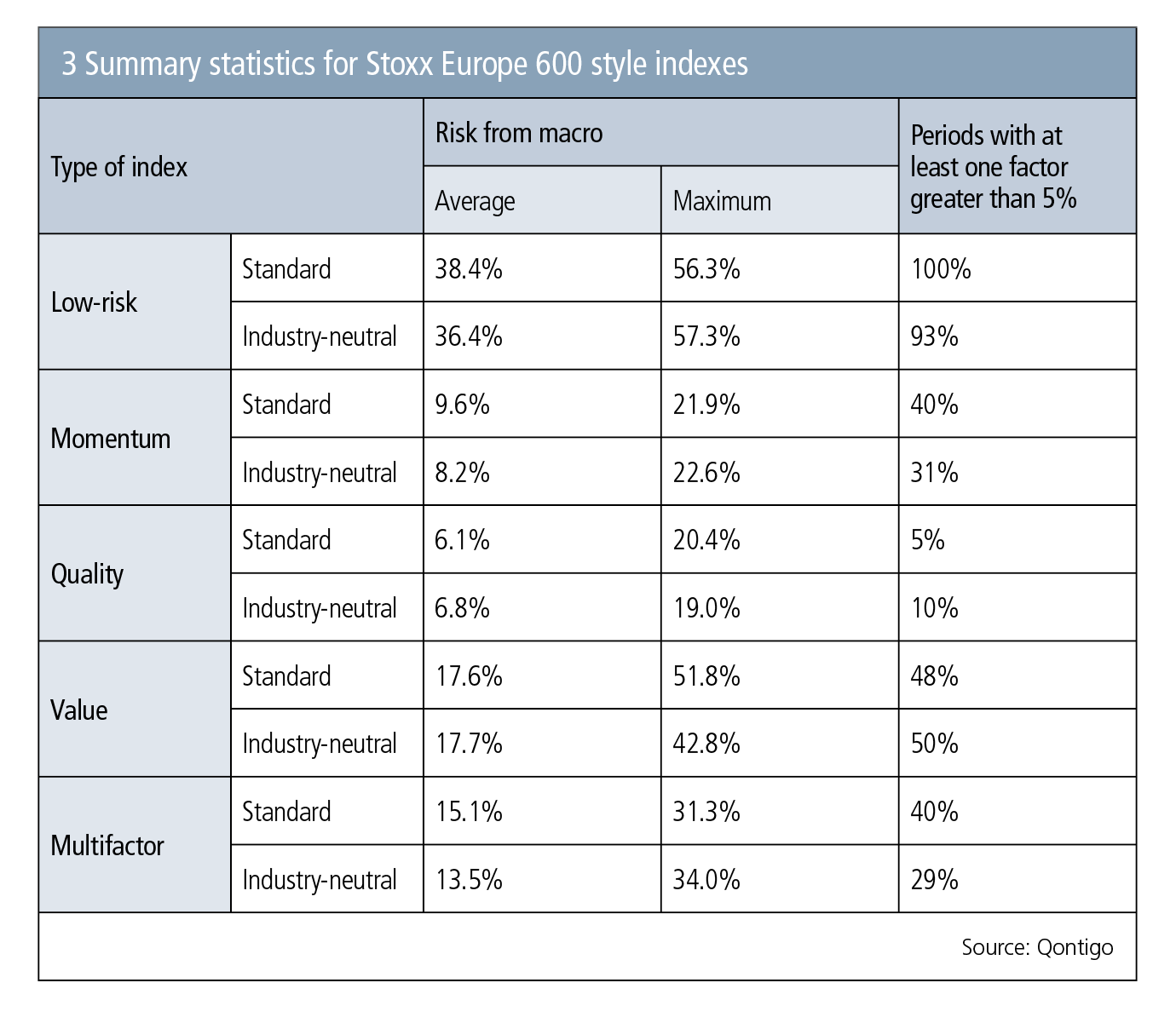

We also calculated the same set of statistics for factor indexes built on the Stoxx Europe 600 index (see figure 3). Almost all the statistics present a higher sensitivity to the macroeconomy in Europe compared with the US, and emphasise that imposing industry constraints reduces sensitivity.

Conclusion

Style indexes and portfolios may engender more macroeconomic risk than investors realise, but that can change over time and based on the specifics of the index. In addition, limiting industry exposures can reduce the macroeconomic risk exposures of a style portfolio.2 When industry exposures were constrained:

- The average contribution from macro factors was lower

- The maximum exposure was lower (except quality)

- The number of periods in which one or more factors contributed at least 5% of the risk was lower.

The impact of industry constraints was biggest for value and multifactor, followed by momentum. Our quality indexes had relatively little macro risk exposure, but it was occasionally high enough that investors may want to at least be aware.

Notes

1. The charts still show active risk from industry exposures – even for the industry-neutral indexes – as the risk model uses finer industry designations than the portfolio construction process, so there may be active weights in sub-industries, even if there is no exposure to the parent industry.

2. Although this analysis was restricted to US indexes, we saw similar results from our European factor index suite.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net