Technical paper/Risk management/Commodities

Identification and capitalisation of non-modellable risk factors

Adolfo Montoro, Tim Becker and Lars Popken propose techniques for systematically capturing and categorising non-modellable risk factors and risk-adequate aggregation

Cutting edge technical: Carbon derivatives pricing

Carbon derivatives pricing: an arbitrageable market

Cutting edge: Modelling the correlation function in the crude-oil futures market

Energy market participants often require the computation of coefficients of correlation in a multi-asset portfolio. Addressing crude oil futures contracts, Ehud Ronn proposes and implements a simple procedure to reduce the cross-maturity correlations in…

Masterclass: Valuing generation assets using Monte Carlo simulation

In this Masterclass, Les Clewlow, James Lujun Liu, Doug Meador, Ron Sobey and Chris Strickland describe the use of Monte Carlo methods for valuing generation assets in more detail. In particular, they discuss the appropriate price models to use and how…

Improving annuity pricing with address data

Technical papers

Taking stock of Pillar II

Technical papers

The true cost of no-cost mortgages

Banks offering no-cost mortgages have been accused of hiding the real cost of the loan from borrowers. But as Andrew Kalotay and Jinghua Qian explain, lenders can also run into problems if they fail to calculate correctly the prepayment behaviour of…

Purchase timing

Managing purchase timing risk is a constant issue for wholesale power buyers. Pavel Diko reviews products that reduce this risk, proposes a lookback option that can eliminate it completely and outlines a hedging strategy for the option writer

Hedging weather exposure

Volumetric weather risk is usually levered by the commodity price, resulting in cross-commodity exposure known as a quanto. Hedging such exposure with quanto instruments is costly. Victor Dvortsov suggests a simple strategy that allows efficient hedging…

Nuclear fusion R&D

In 50 years, nuclear fusion may be a major source of energy, but until then extensive research and development is needed. To justify the current and future R&D expenditure, a cost-benefit analysis designed specially for this sector is required. David…

A matter of principal

Developing term structure models can be tricky, as unknown factors and non-observable variables can affect futures prices. But principal components analysis is useful in tackling these problems. Here, Delphine Lautier uses PCA to pin down price movements…

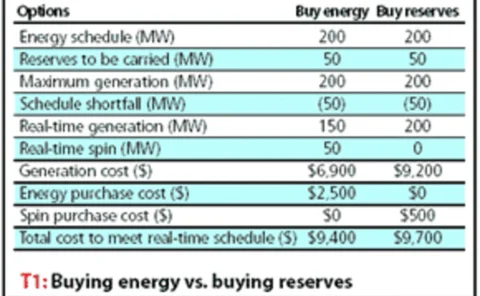

Real-time trading

Rankings 2005

Caring competition

What are the theoretical consequences of restructuring electricity markets on emissions? Here, Benoît Sévi shows that changes in supply and consumption and restructuring for competition has environmental effects, and argues that strong public policies…

Correlated defaults: let's go back to the data

Estimates of asset value correlation are a key element of Merton-style credit portfoliomodels. Many practitioners have access to asset value data for a large universe of listedfirms, so estimation is within reach. Alan Pitts describes a statistical…