Risk-based capital

Solvency II to cause regulatory arbitrage in Asia

A two-tier regulatory market could develop across Asian insurance sectors as Solvency II capital requirements for European insurers will cause them to lose out to domestic competition

Aussie insurers face new risk-based capital requirements

New explicit requirement for operational risk capital proposed for life and general insurance firms in Australia.

The liquidity gap

Regulators are increasing their focus on liquidity risk in response to the financial crisis, but there are questions about whether capital is an effective mitigant for liquidity risks and the nature of the relationship between liquidity risk and bank…

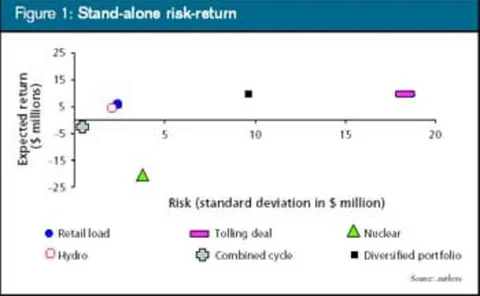

Breaking down the model

Brett Humphreys and Andy Dunn outline a method to help energy companies minimise potential model risk and thereby avoid costly errors in valuing deals.

Optimise this

One of the reactions to recent energy trading difficulties has been a shift away from speculative activities towards portfolio optimisation, but what does the term really mean, ask Tim Essaye and Brett Humphreys

Stress tests and risk capital

For many financial institutions, "stress tests" are an important input into processes that set risk capital allocations. In the current regulatory environment, two distinct model-based approaches for setting regulatory capital requirements include stress…