Technical paper

Cutting edge: Electricity contract risk with portfolio effects

The incremental risk of including electricity contracts in a portfolio is computed by George Levy using a Monte Carlo regime-switching approach. The volume and price processes are modelled using empirical distributions and correlation is captured via a…

Pricing CDSs’ capital relief

Pricing CDSs’ capital relief

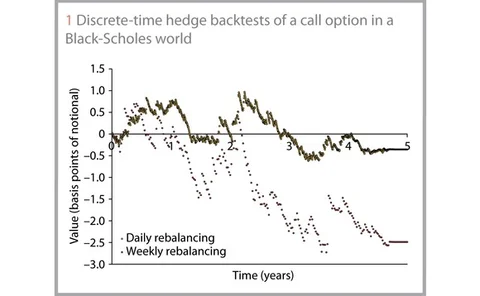

Hedge backtesting for model validation

Hedge backtesting for model validation

Exposure under systemic impact

Wrong-way risk (WWR) behaves differently for exposures to systemically important counterparties because their default has the potential to move financial markets before the close-out. Michael Pykhtin and Alexander Sokol show how the traditional exposure…

Cutting edge: Impact of execution behaviour on valuation of optional financial contracts

Expected payoff maximisation is a commonly assumed strategy in valuation. S Hossein Hosseini, Qiaoyan Bian, Jay Chen and John Jiang suggest that execution strategies may vary due to complex option structures and their resulting uncertainties. Using a…