Technical paper

Banco Urquijo

Quant analysis by StructuredRetailProducts.com

The sum of its parts

Germany

Replication of flexi-swaps

Ingmar Evers and Farshid Jamshidian describe a relatively new product known as a flexi-swap and discuss its application in securitisation. A flexi-swap gives a counterparty an option to amortise the interest rate swap at an accelerated pace. They show…

Rating properties and their implications for Basel II capital

Internal ratings

Common interests

Interest rates

La Caixa

Quant analysis by StructuredRetailProducts.com

Sanpaolo IMI Group

Quant analysis by StructuredRetailProducts.com

Quant analysis by StructuredRetailProducts.com

Quant analysis

Barclays

Quant analysis by StructuredRetailProducts.com

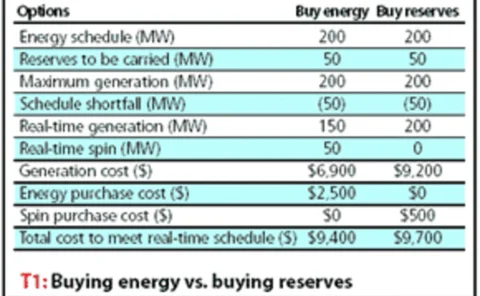

Real-time trading

Rankings 2005

Understanding variations in the risk of multi-strategy portfolios

Investors spend a great deal of time and effort setting a thoughtful risk budget for their portfolio,only to see all too frequently that the targeted risk will be missed by a wide margin when theinvestment process gets started. In this article, Gang…

Jumps as components in the pricing of credit and equity products

The equity and credit markets have become increasingly integrated over recent years. This has increased the need for models and tools that allow traders to hedge their risk simultaneously in the two markets. Here, Daniel Bloch presents an approach that…

Quant analysis by StructuredRetailProducts.com

Quant analysis

AGF

Quant analysis by StructuredRetailProducts.com

West LB

Quant analysis by StructuredRetailProducts.com