This article was paid for by a contributing third party.More Information.

Stress‑testing under Covid‑19

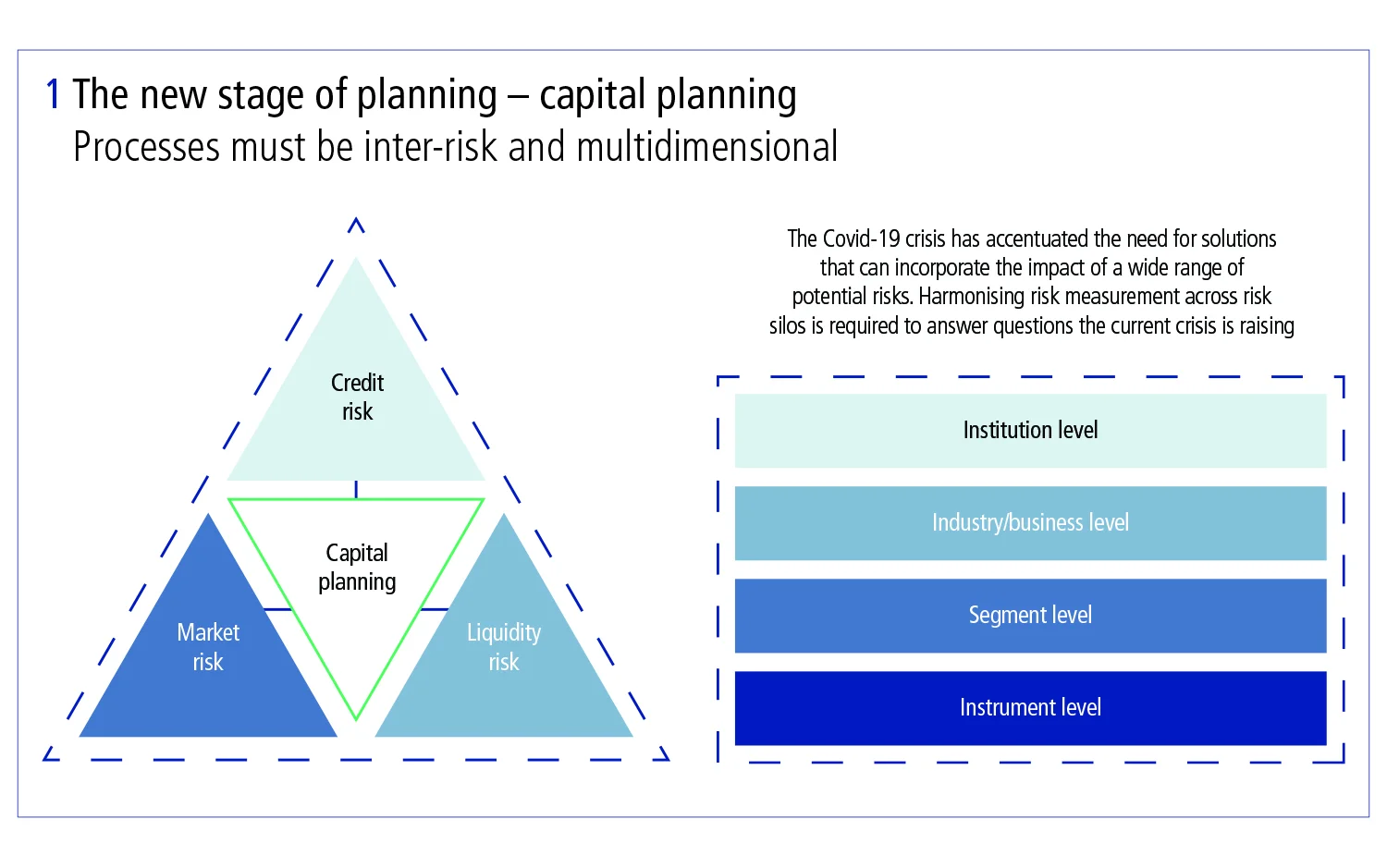

Banks need to build numerous models and try to separate bank-specific decisions from macroeconomic effects. Projecting the balance sheet and income statement under the most likely scenarios is no easy task – and banks cannot rely solely on internal performance data.

When stress‑testing needs arise from ad hoc situations such as the Covid‑19 pandemic, the challenge is even more complex as the process lies outside of ‘business as usual’. Timelines are compressed and validated models might not be adapted for the specific stress.

The Moody’s Analytics paper Stress testing under Covid‑19 explores an approach that addresses these issues, proposing an alternative simple, coherent methodology that allows Moody’s Analytics to forecast and stress‑test the entire balance sheet and profit-and-loss statement consistently for all of the approximately 6,000 banks in the US. This methodology can be used as a primary approach for banks without the means to produce such stress‑testing exercises, or as a challenger or benchmark to validate the results of a set of primary models.

The Moody’s Analytics approach is also useful for strategic planning as it allows banks to compare their balance sheet and income statements with those of their peers and the industry, and to explore potential mergers and acquisitions.

Moody’s Analytics has always been on the front line of quantitative analysis to support loss forecasting and forecasting the other line items of the balance sheet and income statement. A few years ago, at the peak of the Comprehensive Capital Analysis and Review exercise, Moody’s Analytics helped customers develop models and execute simulations to produce regulatory reports, such as the US Federal Reserve’s FR-Y14. We have harnessed this experience in Capital Risk Analyzer, a capital planning and stress‑testing solution that offers a cloud-based platform to execute champion and challenger forecasting models, and off-the-shelf models to automate stress‑testing.

Stress testing under Covid‑19 discusses one of the approaches in this solution based on a top-down model, the Call Report Forecast. This model uses publicly available historical data through the Federal Deposit Insurance Corporation report to derive forecasts for industry-level aggregates based on asset sizes and geographies. The paper describes how this approach can be useful for producing stress‑testing results with unexpected scenarios, such as the Covid‑19 pandemic: first, by examining the methodology used to produce industry-level forecasts, then looking at Covid‑19-based scenarios before finally combining them to quickly produce bank-level forecasts under these scenarios.

To learn more

Stress-testing – Special report 2020

Read more

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net