Interdealer brokers consolidate to survive

Four of top five firms in this year's rankings are involved in deals

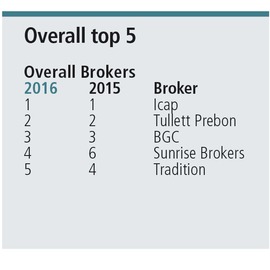

Since last year’s Risk ranking of interdealer brokers, the sector has embarked on a series of long-awaited consolidating deals. Four of the top five firms in this year’s survey are involved, underlining the scale of the change.

In January, BGC Partners completed its merger with GFI Group – an integrated back office now supporting the still-separate front-office brands. BGC followed in July with an agreement to buy equity specialist, Sunrise Brokers. Icap and Tullett Prebon, meanwhile, are edging closer to regulatory approval for a deal that will bring together their respective voice brokers as TP Icap.

When the dust settles, the market will contain two giants – BGC and TP Icap – alongside a third firm of substance, Tradition. Below this global bulge bracket, there will be a big gap to the remaining crowd of small and mid-sized brokers that focus on specific products or geographies.

The consolidation has a simple strategic imperative – with dealers in retreat from many products, and other market participants being nudged towards standardised products that trade on exchange or wholly electronically, the brokers need scale to survive. They may also need new customers, and bigger brokers should have more freedom to chase them.

The consolidation has a simple strategic imperative – with dealers in retreat from many products, and other market participants being nudged towards standardised products that trade on exchange or wholly electronically, the brokers need scale to survive. They may also need new customers, and bigger brokers should have more freedom to chase them.

This is a market in which Risk’s rankings will no longer work as well as they have – voter numbers are already dwindling, as is the number of firms competing for the honours.

The various individual products still work as a snapshot of the banks’ preferred brokers, but it is increasingly difficult to do this comprehensively, or to aggregate votes in the various products and obtain a useful picture.

This year, it was necessary to add up votes across the various forex products – swaps, options, forwards and exotics – to produce credible results. The votes are grouped by currency pair instead. For the second year in a row, there is no ranking of brokers in credit derivatives. The rankings have become patchy as a result. The relatively high number of remaining rates and equities categories magnifies the size and importance of the firms that perform well in these spaces – as does the fierce competition between Sunrise and its upstart rival, Square Global Markets, which between them attracted a big chunk of the overall vote.

Risk has grown up with many of these firms over its 29-year existence, and for much of that period, the rankings have been a good way of keeping tabs. Next year’s version must evolve alongside the industry it tracks – and it will. But that’s all we’re saying for now.

HOW THE POLL WAS CONDUCTED

In total, Risk received 588 valid responses for this year’s rankings, primarily divided between Europe (67.5%), North America (19.9%), and Asia-Pacific (12.1%).

The broker rankings cover 56 instruments across interest rates, foreign exchange and equity derivatives. Participants were asked to vote for their top broker in each instrument, based on the criteria most important to them.

As always, the poll is not designed to reflect volumes traded in any particular market and is therefore not a direct reflection of market share – voters are able to base their decisions on a variety of criteria, including cost, liquidity provision, technology support and reliability. In that sense, this poll should be considered a reflection of how banks view brokers in terms of overall quality of service.

When aggregating the results, we strip out what we consider to be invalid votes. These include people voting for their own firm, multiple votes from the same person or IP address, votes by people who clearly do not trade the product, votes that select the same firm indiscriminately throughout the survey, and block votes from groups of people on the same desk at the same institution. The editor’s decision on the validity of the votes is final.

The survey also includes asset class leaderboards – showing the top brokers in rates, foreign exchange and equities – which are calculated by aggregating the total number of votes across individual categories. These overall results are naturally weighted, as there are more votes in the large categories (for example, US dollar and euro swaps) than the smaller, less-liquid categories.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net

More on Rankings

Risk management is key in this unpredictable environment

With energy markets upended by crisis after crisis, the best strategy is always to be hedged against extremes

A consistent view of risk across the organisation

Beacon by CWAN is a unified platform that spans the full investment lifecycle – from trading and modelling to accounting and regulatory reporting

TP ICAP: leveraging a unique vantage point

Market intelligence is key as energy traders focus on short-term trading amid uncertainty

GEN-I: a journey of ongoing growth

GEN-I has been expanding across Europe since 2005 and is preparing to expand its presence globally

Bridging the risk appetite gap

Axpo bridges time and risk appetite gaps between producers and consumers

Axpo outperforms in the Commodity Rankings 2024

Energy market participants give recognition to the Swiss utility as it brings competitive pricing and liquidity to embattled gas and power markets

Hitachi Energy supports clients with broad offering

Hitachi Energy’s wide portfolio spans support for planning, building and operating assets. Energy Risk speaks to the vendor about how this has contributed to its strong Software Rankings performance in 2024

Market disruptions cause energy firms to seek advanced analytics, modelling and risk management capabilities

Geopolitical unrest and global economic uncertainty have caused multiple disruptions to energy markets in recent years, creating havoc for traders and other companies sourcing, supplying and moving commodities around the world