This article was paid for by a contributing third party.More Information.

Automating regulatory compliance and reporting

Flaws in the regulation of the banking sector have been addressed initially by Basel III, implemented last year. Financial institutions can comply with capital and liquidity requirements in a natively integrated yet modular environment by utilising technology developed by providers such as Profile Software

Basel III reforms implementation in Europe: the third Capital Requirements Regulation (CRR III)

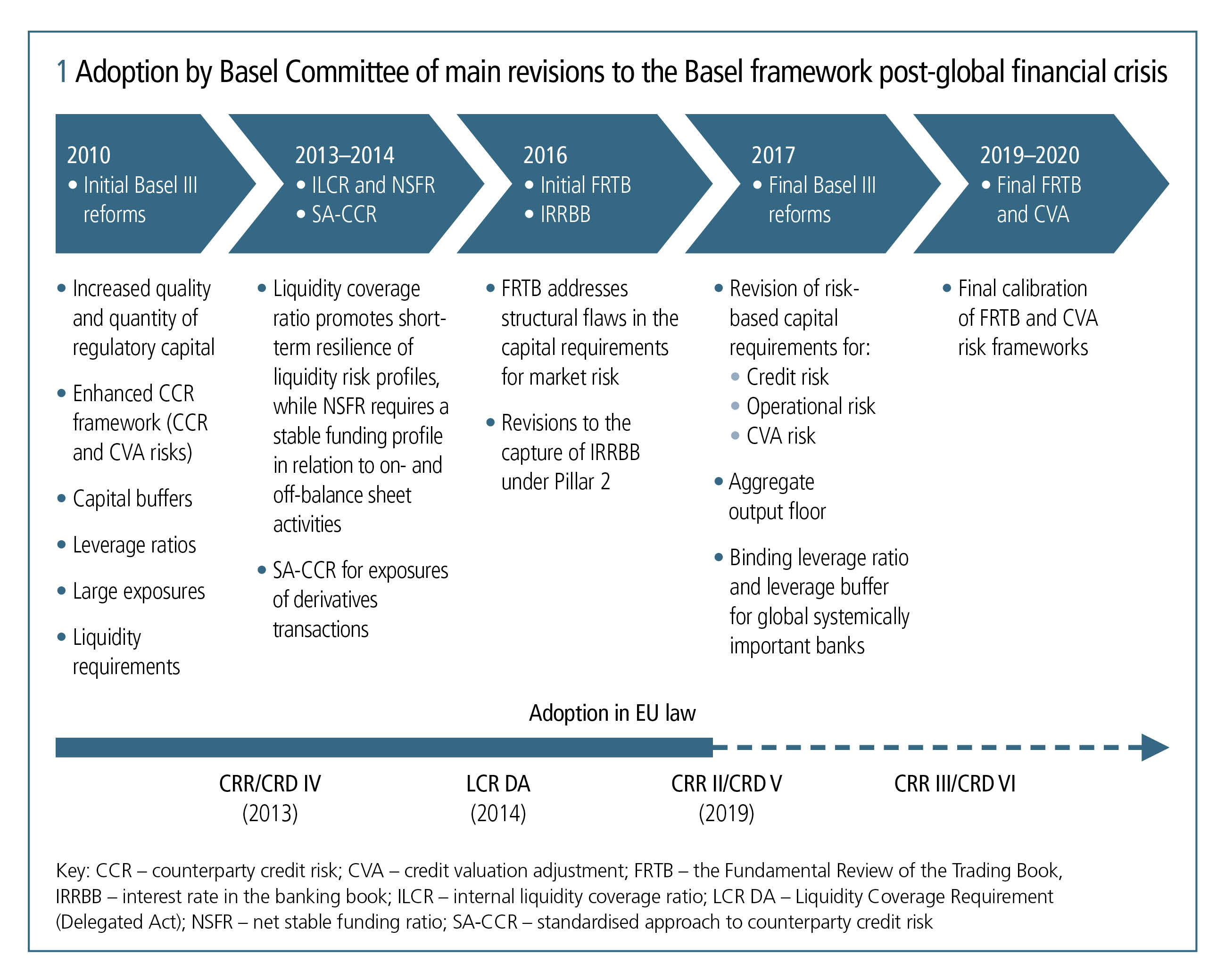

The global financial crisis that began in 2007–08 exposed flaws in the regulation of the banking sector. To address this, the Basel Committee on Banking Supervision published the Basel III reforms (Basel IV), with the initial implementation in January 2022.

The European Union implemented substantial reforms to the prudential framework that applies to banks to enhance resilience to financial sector turbulence and prevent the recurrence of a similar financial crisis. Those reforms were largely based on the Basel Committee’s standards.

Figure 1 provides an overview of the first and final set of Basel III reforms, as well as the timelines of their adoption in the EU:

In October 2021, the European Commission (EC) adopted a review of EU banking to ensure a more resilient and robust banking regulatory framework. In preparation for implementation, different options for implementing the package – with EU-specific adjustments and a transition period to cater for the specifics of the EU economy – have been put forward.

After the publication of the general approach proposal of the EU Council in October 2022, a trialogue with the European Parliament began in March 2023, which ended with the provisional agreement of June 2023.

The forthcoming amendment of CRR is expected to come into force in January 2025.

Major reforms in EU banking frameworks

Some major amendments to the general approach proposed in October 2022 – which were published in the EU procedure to amend Regulation 575/2013 – are listed below:

Credit risk

- Output floor – The output floor represents one of the key elements of the Basel III reforms. It aims to set a lower limit of 72.5% for the standardised approach to risk-weighted assets (SA-RWA) compared with the internal ratings-based approach to RWA (IRB-RWA) – which applies to institutions using the internal ratings-based approach to counterparty credit risk (IRB-CCR). The general approach concluded with an application at all levels of consolidation, with an option to differentiate at the request of EU member states. A transitional arrangement period has been introduced to implement the revisions of the output floor within the EU smoothly.

- The standardised approach to counterparty credit risk (SA-CCR) – The current SA-CCR has been revised to be more risk-sensitive in a number of areas. Moreover, the necessity of the output floor requires the recalibration of SA-CCR to increase consistency with the IRB-CCR.

- IRB-CCR – The global financial crisis revealed important deficiencies in the IRB-CCR. The legislative proposal aims to recalibrate the guidance for IRB-CCR to enhance the robustness of the results and thus the financial system.

- Credit risk mitigation

- Specific provisions have been inserted to reflect prudential guidance for a substitution approach, when guaranteed exposure and comparable direct exposures are treated by different supervisory approaches (SA, advanced-IRB and foundation-IRB approaches).

- Rules and methods for the financial collateral’s comprehensive method approach are amended, pursuant to Basel III rules.

- Treatment – under the comprehensive approach of securities financing transactions covered by master netting agreements – is recalibrated in line with Basel Committee standards.

Operational risk

The Basel Committee concluded that the current framework on operational risk lacks risk sensitivity to SAs and comparability resulting from internal modelling under the advanced measurement approach. To address this, all existing approaches for calculating operational risk capital requirements were replaced by a single SA.

The revised SA is based on a Business Indicator Component that relies on the size of an institution.

Environmental, social and governance (ESG)

The EU promotes a long-term green transition, which, if realised, would see it become a sustainable and climate-neutral continent by 2050 through the European Green Deal road map, in response to the ongoing climate crisis.

To that end, CRR III and the sixth iteration of the Capital Requirements Directive (CRD VI) aim to set new regulatory requirements and definitions on how financial institutions across the EU will identify, disclose and manage ESG risks for exposures.

Crypto assets

In December 2022, the Basel Committee published rules – which must be implemented by January 2025 – covering the treatment of the inherent risk in crypto asset exposures. International standards classify crypto assets on an ongoing basis into two groups: those that meet in full and those that fail to meet a set of classification conditions.

Although not widely used in banking operations, the rapid increase in financial market activity connected to crypto assets may lead to turbulence in the EU banking industry. Therefore, the European Parliament, in a legislative resolution proposal in February 2023, suggested following up the Basel Committee’s developments and publishing a proposal by December 2024.

The proposal requires institutions to disclose exposures to crypto assets and related activities, and to apply an interim risk weight of 1,250% to exposures to crypto assets until December 2024.

Provisional agreement

Following the publication of the general approach proposal, the negotiators from the European Parliament, the European Council and the EC ended with the provisionally agreed date of June 2023, which had been reached ad referendum, having to be approved before coming into force. Negotiators have struck a provisional deal on:

- Capital requirements

- Environmental and crypto risks

- Amendments to CRD

Utilising technology to fully comply with CRR III

Banks strive to meet regulatory requirements, while continuously monitoring the evolving regulatory framework and aligning their strategies and business models with risk management expectations.

It is a challenge to automate and streamline the process for regulatory risk calculations and reporting to free up resources to direct to primary risk management objectives and analysis, so banks should consider investing in more flexible, robust and fully integrated regulatory technology platforms.

By adopting technology providers such as Profile Software, financial institutions can achieve regulatory compliance for capital and liquidity requirements in a natively integrated and modular environment.

The RiskAvert platform ensures data consistency and integrity while ensuring the delivery of personalised reporting for institutions based on their unique needs.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net