This article was paid for by a contributing third party.More Information.

From fragmented signals to confident credit decisions

At Risk Live 2025, Credit Benchmark and Oliver Wyman explored how aggregated bank data and advanced analytics are helping risk teams make more confident, forward-looking credit decisions

Credit risk professionals are being asked to do more with less clarity than ever before. Volatile macroeconomic conditions, growing private credit exposure and increased regulatory scrutiny are combining to stretch internal risk models and expose the limits of traditional credit data sources. For banks, asset managers and insurers, the challenge is not just about monitoring risk – it’s about finding signals buried in fragmented, often incomplete, data.

That is the issue Credit Benchmark and Oliver Wyman tackled at Risk Live in their session Signals in the noise: extracting credit risk clarity from a fragmented world. The presentation provided insight into how the two firms are working together to help institutions gain forward-looking, aggregated credit views – especially for the growing portion of the market that lies beyond the reach of public ratings.

The data gap

The structure of credit markets is evolving rapidly. Increasingly, institutions are exposed to counterparties in private markets – such as mid-market corporates, private equity-backed firms, hedge funds and funds of funds – that lack public ratings. At the same time, global banks face heightened requirements under internal ratings-based (IRB) approaches and International Financial Reporting Standard 9 (IFRS 9), which call for defensible, well-calibrated models – even in low-default portfolios where internal data is thin.

“In many cases, a single institution’s dataset just isn’t enough to build or validate a robust credit model,” said Cem Dedeaga, partner and head of risk modelling, UK & Ireland, at Oliver Wyman. “This is especially true for hard-to-model segments where you don’t have observed defaults – but collectively, the market may have seen enough events to make a case.”

It’s not just a modelling issue. As portfolios diversify across asset classes and geographies, siloed internal views create blind spots in credit monitoring and capital planning. This is where Credit Benchmark’s model comes in.

Aggregated views

Credit Benchmark’s solution is to pool internal credit risk assessments – probabilities of default (PDs) and loss given defaults – from 40 of the world’s largest banks to generate Credit Consensus Ratings (CCRs) for entities that traditional sources often overlook.

“These are real credit assessments used by banks managing actual exposure,” said Joe Proctor, head of banking, Apac and Emea at Credit Benchmark. “What we do is anonymise and aggregate that data to create a single consensus view – updated weekly – that reflects how risk professionals are viewing these entities in real time.”

Today, Credit Benchmark has consensus ratings on more than 115,000 entities, around 90% of which are unrated by public credit rating agencies. The dataset covers such areas as fund finance, private corporates, structured credit exposures and mid-market lending – segments that are expanding in importance but remain difficult to analyse through traditional lenses.

“This isn’t just filling in the blanks – it’s creating a new category of forward-looking credit insight,” said Proctor. “And, because these are sourced from banks using IRB models, including global systemically important banks, the data is already aligned with regulatory standards.”

Capital relief

One of the most immediate applications of Credit Benchmark’s data is in model development and validation for regulatory compliance – an area in which Oliver Wyman has been helping clients use consensus insights to unlock capital efficiency.

“Under the latest regulatory guidance (particularly covering the UK and Europe), banks are required to demonstrate the effectiveness of their models, even in low-default portfolios with more robust evidence,” said Dedeaga. “But if your internal data can’t show that, you may be forced to apply heavy conservatism, tying up capital unnecessarily.”

Through a joint initiative known as IRB Nexus, Oliver Wyman and Credit Benchmark have worked with institutions to use consensus data as a supplement in IRB model development, monitoring and validation. Dedeaga said: “By using Credit Benchmark’s data, we were able to develop a broader market view of defaults and PD parameters that provided further important evidence to internal validation teams and regulators in their reviews.”

The approach is already bearing fruit. “Banks have had supervisory inspections using this methodology already,” he added. “Specifically, it has helped banks justify their levels of conservatism and made the internal model frameworks more defensible.”

Better early warning systems

Beyond regulatory modelling, consensus data is increasingly being used as part of integrated early warning indicators, where the goal is to spot signs of credit deterioration before losses emerge.

“After events like Archegos, there seems to be increased pressure on banks to show they can detect stress early, even in entities without public ratings,” said Proctor. “Consensus data provides another signal – one based on the actual behaviour of bank risk teams updating internal views.”

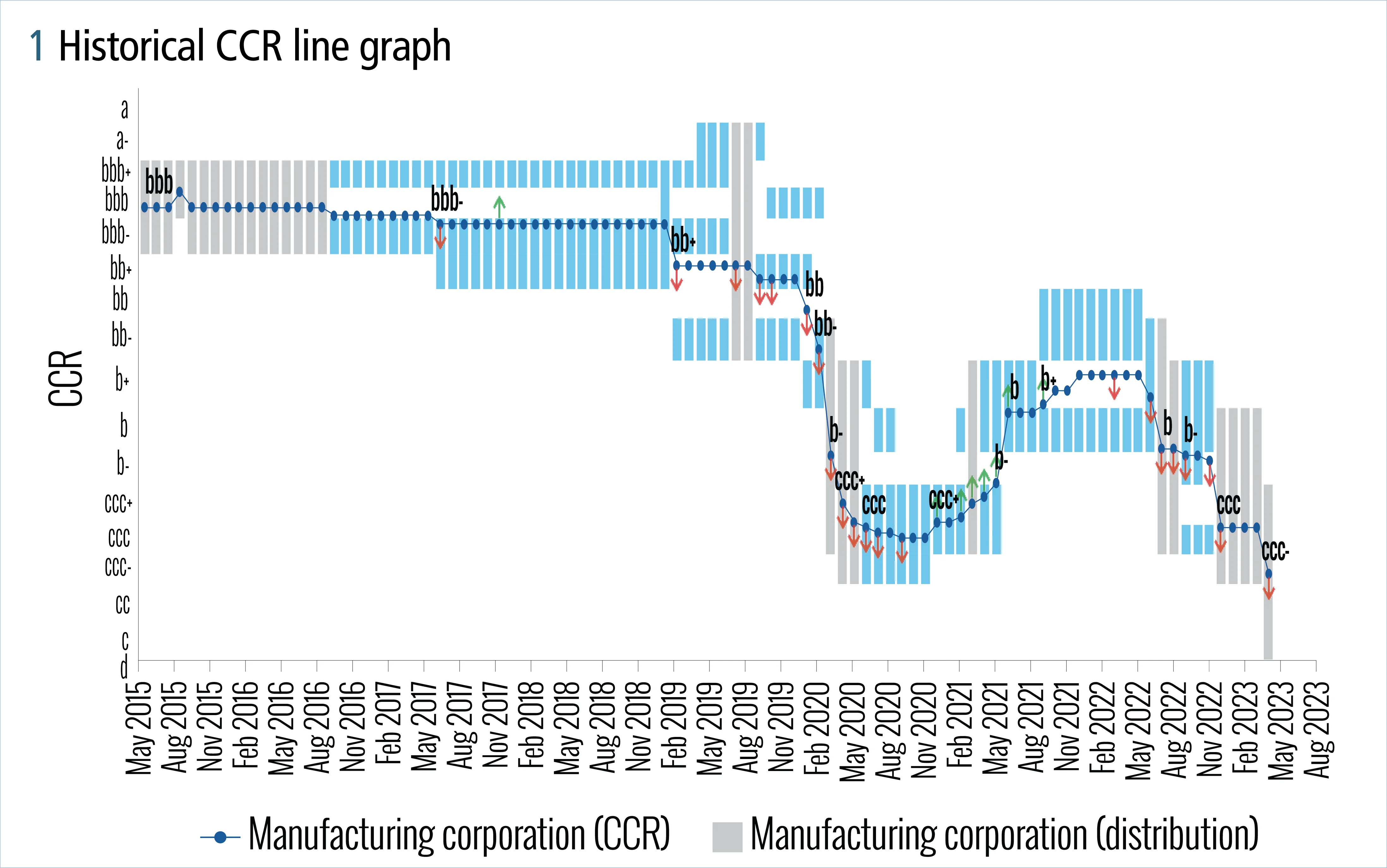

Credit Benchmark tracks opinion change indicators (see figure 1) – subtle shifts in the PDs that banks assign to an entity, even if the overall rating band hasn’t changed.

“If the consensus stays flat but the underlying PDs are trending lower, then that is valuable metadata,” Proctor added. “It tells you where to take a closer look.”

Oliver Wyman integrates sentiment signals from Dow Jones Factiva data using machine learning. This adds further depth by helping to evaluate news flow around specific entities.

“We apply a large language model to score articles for positive or negative credit sentiment,” said Dedeaga. “That’s then aggregated and linked to entities as a monitoring signal. It’s not a rating; it’s a spotlight that tells analysts where to focus their time. It is making risk management multiple times more efficient.”

By combining these tools, clients gain layered insights: baseline credit signals from consensus data, directional shifts from opinion changes and timely red flags from news sentiment.

Expanding use cases

The consensus model isn’t limited to modelling or monitoring – it’s also being adopted for credit portfolio management, pricing and second order (or look-through) risk analysis.

In fund finance, for instance, where the underlying counterparties are often unrated, limited partners or funds-of-funds, Credit Benchmark has become a core data provider.

“Banks will send us their full obligor lists – often tens of thousands of entities – and we’ll return a coverage map showing where we have consensus ratings,” said Proctor. “This has proven especially useful in areas like private equity, where traditional data just doesn’t exist.”

For credit valuation desks, consensus PDs can help construct more reliable credit curves when public benchmarks are unavailable. And, in risk transfer markets, such as synthetic securitisations, the data helps assess the underlying credit distribution at the point of structuring.

“We’ve seen increasing interest from financial institutions managing exposures to non-rated corporates,” Proctor added. “Consensus data offers valuable use cases, including IFRS 9 benchmarking, credit risk management and portfolio analysis, providing insights that traditional sources may not deliver.”

The future of credit decisioning

Ultimately, what distinguishes the Credit Benchmark and Oliver Wyman collaboration is its focus on making hard-to-see risk visible, without trying to replace internal models or external ratings.

“We’re not trying to be a rating agency,” Proctor pointed out. “We’re trying to provide a complementary signal – one that reflects how banks, in aggregate, are seeing credit risk shift across the market.”

That view is resonating with institutions under pressure to justify their models, monitor sprawling portfolios and respond more quickly to emerging risks.

“In today’s environment, it’s not enough to have a single lens on credit,” said Dedeaga. “You need different types of signals – like sentiment and internal ratings – to get a more complete view of credit risk.”

As credit markets become broader, more opaque and interconnected, clarity won’t come from one model, dataset or signal. It will come from the ability to integrate them – turning fragmented insights into confident decisions.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net