This article was paid for by a contributing third party.More Information.

Breaking the collateral silos – Navigating regulation with a strategic alternative

Emmanuel Denis, head of tri‑party services at BNP Paribas Securities Services, discusses why financial institutions must rethink old practices of collateral management and instead adopt a tri-party approach, with which equities can be managed as collateral

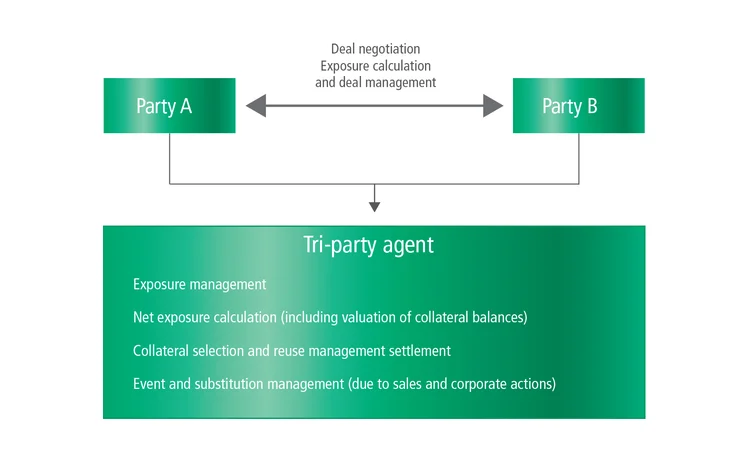

New regulations mean that market participants are seeking more sophisticated and comprehensive collateral solutions that will enable them to use a wide range of securities to back their trades and mobilise their assets when and where they are needed. Increasingly, they are turning to the tri-party model. Acting as a neutral party, the tri-party agent manages the collateralisation of exposures that result from trading activities between two counterparties.

However, how can a service designed historically for interdealer transactions fully meet new collateral management requirements? What are the conditions necessary for an efficient tri-party collateral management? BNP Paribas examines three different collateral requirements:

- Variation margin (VM) on uncleared over-the-counter (OTC) derivatives

- Initial margin (IM) on cleared OTC

- Securities financing transactions.

Using equities as collateral

The main characteristic of bilateral management on uncleared OTC derivatives is the almost exclusive use of cash and government bonds. There is an inherent risk in using equities as collateral due to the frequency of corporate actions. When these occur, there may be a tax risk when failing to detect such events or substitute on time. Therefore, some asset managers have had to change their investment profiles to hold cash or bonds, which has had an impact on their returns – especially for Ucits funds that cannot ‘transform’ their equities because of regulatory guidelines.

The tri-party model is perfectly suited to manage equities as collateral. However, this solution is only viable for the buy side if various criteria are met:

- Both buy-side and sell-side participants must adapt their operational processes for OTC derivatives to create a new operational path for tri-party collateral management

- The tri-party agent must comply with asset segregation rules such as Ucits and the Alternative Investment Fund Managers Directive imposed on some institutional investors. These are not entirely uniform, with some local rules needing to be considered1

- Tri-party management must be connected directly to the client’s main account to avoid the burden of constantly managing collateral inventory realignments.

Initial margin on cleared OTC derivatives

In addition to the VM obligation, more of the buy side will soon be required to post the IM on OTC derivatives cleared by central counterparties (CCPs) as the clearing mandate progressively enters into effect. Some participants are anticipating this, as their banking counterparties have already passed on to them the capital costs associated with uncleared transactions. This is particularly true for large and directional portfolios with long-dated trades, such as those held by pension funds. Given the size of the IM, it is most likely that many will decide to post securities.

A tri-party service can be a considerable benefit because of the following:

- The amount of the IM varying – even more with new OTC derivatives trades

- No minimum transfer amount – unlike uncleared OTC derivatives – meaning the client will be called for the first penny

- The requirement that transfers between the customer and the CCP are complete on the same day

- Different places of deposit between the buy side and the CCP, resulting in early market cut‑offs to transfer the collateral.2

Tri-party securities financing

Today, the hundreds of billions of euros of collateral linked to securities financing transactions mainly comes from interdealer transactions, with few buy-side participants. Institutional investors are eyeing new opportunities for securities financing transactions. With quantitative easing, historically low or negative interest rates and the requirements of Basel III, banking counterparties are seeking high‑quality liquid assets over the long term. Buy-side participants will be able to generate additional income, which is particularly welcomed in the current environment.3

Several initiatives have emerged in trading with new securities financing execution platforms. On post-trade, it is essential to optimise the full operation chain – confirmation with the counterparty, fees calculation, portfolio accounting, monitoring funds’ ratios, collateral management, and so on.

As with OTC derivatives, tri-party platforms are well positioned:

- Basket repos can be easily managed as the cash-leg settlement is synchronised with several lines of securities defined by an eligibility matrix – also known as the ‘basket’

- They provide more velocity to the collateral giver, notably when refinancing small lines of securities

- The type of collateral can be broader – equities or corporate bonds – enabling the buy side to obtain more attractive execution spreads.

At a turning point

It is time for financial institutions to rethink the old practices of collateral management and break existing silos. Although the tri-party service was initially created for the interdealer business, it can be used more widely across financial institutions’ derivatives activities. To make it a success, market players should adopt a strategic approach, with the involvement of many teams, to ensure that processes along the value chain – from front office to middle and back office – are adapted to tri-party services.

1 The same segregation rules apply to Italian pension funds, for example.

2 The buy side uses a global custodian. Article 47.3 of the European Market Infrastructure Regulation requires CCPs’ initial margins to be held by a securities settlement system.

3 Excluding Ucits funds that cannot participate in term securities financing transactions because of regulatory restrictions.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net